1 Bitcoin's Price Soars

In recent years, Bitcoin's price has gone through multiple rounds of strong appreciation. At the start of 2023, Bitcoin's price was only about $20,000. Now, it has long surpassed the $100,000 mark and remains high, with the price increasing almost five-fold. Bitcoin's continuous rise over more than two years reflects the global liquidity environment, institutional allocation demand, and the trend of digital assets entering the mainstream financial system.

Data source: yahoo finance, Chart by FinTax

2 High Returns Come with High Taxes

However, the other side of the soaring price is the real problem Bitcoin investors face when cashing out—as tax regulations tighten in various countries, the tax burden from cashing out BTC has intensified .

Take the United States as an example. The IRS treats cryptocurrency as property. Therefore, when selling, trading, or otherwise disposing of crypto assets, the income is considered capital gains or ordinary income and taxed at the relevant rates. Specifically:

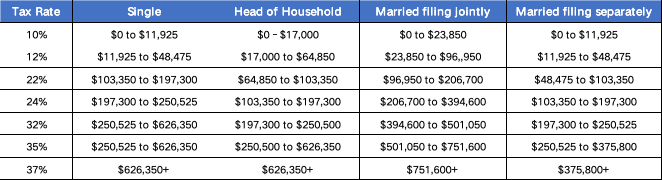

Ø If you hold cryptocurrency for less than one year, you must pay short-term capital gains tax. The rate is calculated according to ordinary income tax rates, which vary based on an individual's annual income, ranging from 10% to 37%.

The 2025 tax year federal income tax rates are:

Ø If you hold cryptocurrency for more than one year, you must pay long-term capital gains tax. Favorable rates apply to long-term capital gains. Most taxpayers will pay a rate of 0%, 15%, or 20%.

The 2025 long-term cryptocurrency gains tax rates are:

3 A New Tax Planning Idea Based on Accelerated Depreciation Policy

But significant tax pressure doesn't mean taxpayers have completely lost all room for planning. By reasonably using the provisions of the U.S. tax code, it's still possible to reduce the effective tax burden while remaining compliant. For example, the "accelerated depreciation" policy stipulated in §168(k) of the U.S. tax code allows taxpayers to deduct the entire cost of fixed assets like mining rigs or servers in the year of purchase, thereby significantly reducing taxable income. The specific provision is as follows:

(k)Special allowance for certain property

(1) Additional allowance In the case of any qualified property—

(A) the depreciation deduction provided by section 167(a) for the taxable year in which such property is placed in service shall include an allowance equal to 100 percent of the adjusted basis of the qualified property, and

(B) the adjusted basis of the qualified property shall be reduced by the amount of such deduction before computing the amount otherwise allowable as a depreciation deduction under this chapter for such taxable year and any subsequent taxable year.

The following example illustrates the effect of this tax planning approach: An American mining company earns $1 million in revenue in 2024 and invests $500,000 in mining rigs that same year. Assume the corporate income tax rate is 21%.

If applying the §168(k) accelerated depreciation policy: The company can deduct the entire $500,000 cost in that year. The income tax would be approximately:

(100−50) × 21% = $105,000

If using conventional five-year straight-line depreciation: Only $100,000 can be deducted each year. The income tax would be approximately:

(100−10) × 21% = $189,000

It should be noted that using the accelerated depreciation method requires considering the cost situation for the year to avoid losing profits and carrying over losses. Here is another simple example: An American mining company still invests $500,000 in mining rigs in 2024, but it only earns $400,000 in revenue that year.

If still using the §168(k) accelerated depreciation policy:

The company can deduct the entire $500,000 cost in that year, but due to low revenue, this will result in a book loss of $100,000 (NOL, Net Operating Loss) after the deduction. Although the current period's profit is negative and no income tax is due, this also means the company cannot extract or distribute profits, even if there is still cash flow on the books. Furthermore, in terms of tax treatment, under current regulations, an NOL carried forward to the next year can only offset 80% of that year's taxable income. Therefore, blindly using accelerated depreciation in a low-profit year is not a wise move.

Individual Bitcoin holders can also achieve tax reductions by investing in Bitcoin miners, while also receiving monthly mining rewards. For example, the crypto lending company Arch is launching TaxShield. Its co-founders, Himanshu Sahay and Dhruv Patel, said in an interview with CoinDesk that this financial product, developed in collaboration with renowned Bitcoin educator Mark Moss and Blockware, is specifically designed for high-income Bitcoin investors seeking to reduce federal tax liabilities through equipment-based deductions. By their estimates, a client with $1 million in annual taxable income could reduce their federal taxes by about $400,000, all while maintaining their Bitcoin holdings and earning mining rewards.

Conclusion

Overall, while the continuous rise in Bitcoin's price has brought considerable investment returns, it has also made tax issues more prominent. Faced with the dual pressures of tightening regulation and rising tax burdens, blind risk avoidance may exacerbate exposure, whereas leveraging compliant tax incentives provides a more sustainable solution. A more rational choice is to understand and make good use of the compliant policy provisions within the current tax law for tax planning. Take the §168(k) "accelerated depreciation" policy as an example: it provides a realistic path for the capital-intensive crypto industry to legally reduce taxes and optimize cash flow. This case also demonstrates once again that systematic planning within a compliance framework, using the space available in institutional design to resolve tax burdens, is the key idea for cryptocurrency investors to achieve sustainable development.

The FinTax Consulting Team has extensive practical experience in handling complex cross-border tax and compliance matters. Our clients include numerous U.S.-listed crypto companies and multinational enterprises. From equity structure planning to the implementation of tax incentive programs, we are committed to providing one-stop financial and tax solutions for crypto businesses—transforming complex tax compliance processes into a source of business certainty and empowering enterprises to achieve sustainable and steady growth.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.