1 Introduction

In September 2025, the Turkish government put forward a new bill to give its Financial Crimes Investigation Board (MASAK) the power to directly freeze cryptocurrency accounts as part of fighting money laundering and terrorist financing. If it gets voted through and takes effect, this step would be another big tightening in Turkey's anti-money laundering (AML) and counter-terrorist financing (CFT) efforts, and it means their oversight of the crypto asset market is officially moving from just watching to actually enforcing rules. This proposal for MASAK to get account freezing rights shows a change in what regulators are focusing on—from just banning payments to setting up a system that's easy to monitor and track. Unlike the active and stricter crypto rules, Turkey's crypto market is actually thriving: Even though Turkey clearly bans cryptocurrencies for payments, it doesn't stop people or organizations from using them for investing and trading; in real life, Turkey's crypto usage rate is among the top globally, with way more users and trading buzz than in other emerging markets. With ongoing local currency drops and inflation, crypto assets have slowly become a key way for Turkish folks to protect their wealth and invest.

In this setting, getting a grip on Turkey's crypto asset tax system and the legal logic behind it is key for investors and businesses to check out local crypto market risks. Crypto assets are defined in Turkish law as non-monetary intangible assets, and their use and trading are watched over by multiple groups like the central bank, the Capital Markets Board (CMB), and MASAK. The current setup doesn't have a separate crypto tax law, but various taxes—like income tax, corporate tax, value-added tax, and stamp tax—are already partly applied to crypto activities by treating them as assets.

So, this article will lay out Turkey's crypto tax basics and how regulations have evolved, covering legal status, oversight systems, main tax angles, and collection logic, plus look at potential impacts on businesses and individual investors. With global regulations getting tougher, studying Turkey's crypto taxes not only helps understand their approach but also gives practical tips for risk management and compliance to folks active in emerging markets.

2 Turkey's Taxation and Regulation Basics

Turkey's tax setup is handled by the Ministry of Treasury and Finance, with its Revenue Administration (Gelir İdaresi Başkanlığı, GİB) taking care of tax collection, filing reviews, and taxpayer services. The Ministry sets annual budgets, tax rates, and spending plans, while the Revenue Administration handles collecting and info management. The tax year matches the accounting year, running from January 1 to December 31, with a self-filing system. Taxpayers have to file income and taxes through GİB's online system by set deadlines.

2.1 Turkey's Basic Tax Setup

Tax Structure: Turkey's overall tax system includes direct and indirect taxes—direct ones are corporate income tax and personal income tax; indirect ones include value-added tax, special consumption tax, stamp tax, banking and insurance transaction tax, and more. Tax revenues are managed under the Public Financial Management Law (Law No. 5018) by the Ministry of Treasury and Finance, and distributed to local governments and social security bodies.

Basic Tax Rates: Based on GİB's 2025 tax guide and revisions in Official Gazette No. 32590 (July 2, 2024), Turkey uses a mixed tax system—direct taxes have progressive rates, indirect ones are flat rates. Anyone with a home in Turkey or living there over 6 months in a tax year is a tax resident, paying on worldwide income; others are non-residents, only taxed on Turkey-sourced income.

International Cooperation: On the global side, Turkey has signed double taxation avoidance agreements (DTA) with over 80 countries, following OECD standards to prevent double taxing and profit shifting. All taxpayers need to register for a tax ID in the GİB system. Individuals can register and file annually via the e-Devlet Portal; businesses must submit VAT, withholding tax, and income tax reports regularly through GİB's e-filing system. Starting in 2023, the Ministry rolled out full electronic invoicing, e-ledgers, and e-stamp tax, so all registered businesses have to create and keep tax docs electronically.

Digital Taxes: Turkey is also pushing digital tax projects hard—since 2023, the Ministry has been reforming for full digital tax data submission by businesses by 2026. The Ministry joins OECD's Automatic Exchange of Information (AEOI) system (see reference [6]), sharing financial accounts and cross-border transaction info with international tax authorities to stop tax evasion and profit shifting.

Overall, Turkey's tax system balances direct and indirect taxes, with centralized collection and digital filing. The highly centralized setup of the Ministry and GİB ensures steady fiscal income and sets up institutional safeguards for future cross-agency oversight and financial compliance.

2.2 Turkey's Tax Supervision System

For collection mechanisms, Turkey uses quarterly prepayments combined with year-end settlements. Corporate income taxpayers prepay quarterly, then settle at year-end; personal income tax is levied progressively on excess amounts. Tax audits are done by GİB and local tax offices, covering books, bank statements, contracts, and cross-border payments. If underreporting, short payments, or bad filings are found, authorities can collect back taxes plus late fees and fines. Tax disputes can go through admin reviews or to tax courts.

The 2024 Law No. 7524 (Law No. 7524, Official Gazette No. 32550, 2024-07-12) added "domestic minimum corporate tax" and "global minimum tax" rules, requiring businesses to pay at least 10% of profits no matter what perks they get, aligning with OECD's Pillar 2 global minimum tax framework. Plus, free zone tax exemptions got tightened, only applying to export income now.

Overall, Turkey's tax oversight features centralized unity, electronic collection, and international teamwork. As the central tax body, GİB boosts compliance through tech platforms and system integration; the Ministry pushes policy for broader tax bases and cross-border tax coordination, showing Turkey's tax governance is deeply blending digital and global elements.

3 Turkey's Crypto Tax System and Regulations

3.1 Crypto Usage in Turkey

Right now, crypto use in Turkey is still super active. According to Chainalysis's 2025 Global Crypto Adoption Index, Turkey ranks 14th in crypto adoption. [7] This shows that even with stricter rules, Turkish people and organizations are heavily into crypto assets; per AInvest's market report, Turkey's crypto penetration rate is expected to hit 28.17% by the end of 2025, with nearly 24.82 million users. And crypto-related revenue is projected at $2.2 billion that year. [8]

These numbers highlight how big and deep Turkey's crypto use is. With such a huge market share, it's a spot crypto investors and pros can't ignore, and it gives the government reason to amp up regulations.

3.2 Legal Definition of Crypto

Turkey's legal take on crypto assets has evolved from no rules to formal laws step by step.

On the system level, the first clear rule came from the Central Bank of the Republic of Turkey (TCMB) on April 16, 2021—the Regulation on Not Using Crypto Assets in Payments. It was published in Official Gazette No. 31456 and took effect on April 30, 2021. The reg spells out two main points: No direct or indirect use of crypto assets in any payment deals; and payment and e-money outfits can't offer services based on crypto for payments or settlements. Under this law, crypto assets are defined by Turkish officials as "non-material assets created virtually based on distributed ledger or similar tech, distributed via digital networks, but not recognized as fiat money, accounting money, electronic money, payment tools, securities, or other capital market instruments." This definition sets crypto's non-monetary, non-payment tool status in Turkey's legal system, giving a base for later enforcement by regulators.

But this definition only applies to payments and financial deals, not automatically to tax laws. Turkey's Revenue Administration hasn't issued any specific notices or details on taxing crypto assets yet, nor clarified them in the current Income Tax Law or VAT Law. So, TCMB's "non-monetary" definition doesn't directly bind tax applications, and GİB might still classify them as "intangible assets" or "capital gains income" in interpretive notices or collection guides based on economic substance.

In other words, in the current legal setup, crypto assets aren't fiat money and aren't seen as separate tax items yet; how they're handled in tax law will depend on future interpretive notices from GİB and the Ministry. If Turkey follows EU-like frameworks in future tax reforms for crypto normalization, it'll likely go with an "economic substance first" approach, keeping the central bank's definition while GİB taxes based on gain types as capital gains or business income.

3.3 Crypto Regulatory System

On July 2, 2024, Turkey's parliament passed amendments to the Capital Markets Law (Law No. 6362)—Law No. 7518, published in Official Gazette No. 32590. The changes add Article 35/B and more, bringing in a full regulatory framework for "Crypto Asset Service Providers (CASPs)": All CASPs need Capital Markets Board licenses; they must meet minimum capital, set up internal controls and info security systems; custody and client assets must be separated under independent custody rules; unlicensed foreign platforms can't serve Turkish residents, or they'll have to stop operations soon.

Based on OECD's 2024 Crypto-Asset Reporting Framework (CARF) international notice, Turkey has said it'll join CARF and CRS for cross-border tax info swaps, to connect crypto account data internationally. This shows Turkey's regulatory path is moving from domestic compliance to global data teamwork, and future crypto taxes will rely on cross-border info transparency as key support.

The Capital Markets Board issued a press release on the amendment day, explaining that crypto asset service providers have until March 31, 2025, to apply for licenses and file compliance. Plus, follow-up rules published on March 13, 2025, in Official Gazette No. 32509 detail info disclosure, risk warnings, data retention, and cross-border fund transfers. That means from April 2025, unlicensed platforms can't serve Turkish residents anymore.

By now, Turkey's crypto oversight structure is basically set: The central bank (TCMB) handles payment boundaries, the Capital Markets Board (CMB) deals with trading and service provider licenses, and the Financial Crimes Investigation Board (MASAK) covers anti-money laundering and account monitoring.

The legal evolution since 2021 shows Turkey has shifted from banning payments to allowing operations with licenses. The current framework centers on CMB's licensing and MASAK's compliance oversight, backed by the central bank's payment limits and legal definitions, forming a full-chain system covering trading, services, compliance, and reporting. This model gives a legal base for extending tax collection and sets Turkey's role in global crypto governance.

4 Taxes and Rates That Might Apply to Crypto Assets in Turkey

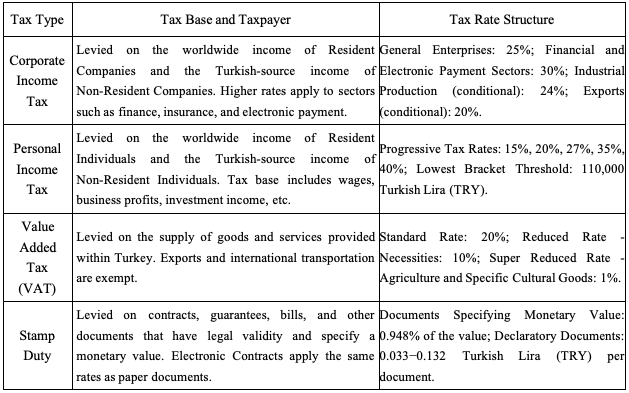

Even though Turkey doesn't have a specific crypto asset tax law yet, existing taxes like corporate income, personal income, value-added, and stamp taxes can extend logically and under certain conditions. In short, these current taxes could be the government's go-to for taxing crypto in the transition period. Specifically: Corporate and personal income taxes could cover investment gains and trading profits from crypto; VAT might apply to platform fees, custody charges, and matching services; stamp tax could link to signed contracts, custody agreements, and guarantee docs in crypto scenarios.

The table below is based on original files from Turkey's Revenue Administration (GİB) and Official Gazette (Resmî Gazete), showing basic scopes, rates, and official sources for each tax.

4.1 Corporate Income Tax (Kurumlar Vergisi)

If businesses do crypto trading matching, custody, payment infrastructure, or market-making, their operating income could count as taxable profits, calculated at the corporate rate. If Turkey formally brings virtual asset platforms under CMB licensing, this tax would be key for crypto businesses to comply and pay.

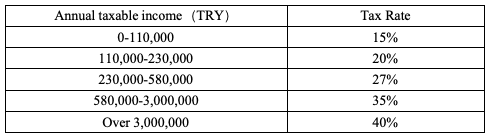

4.2 Personal Income Tax (Gelir Vergisi)

Individual investors getting price difference gains from trading crypto could, without specific rules, be taxed as capital gains under personal income tax.

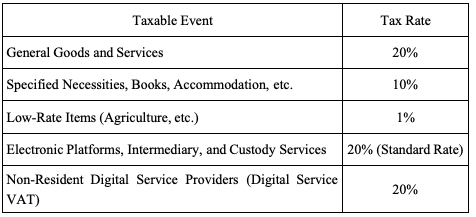

4.3 Value-Added Tax (Katma Değer Vergisi, KDV)

For outfits providing matching, custody, advisory, or platform ops services, fees like service charges or handling fees might be seen as taxable services, filed at 20% rate. If detailed rules come out, KDV would be a big factor in trading costs.

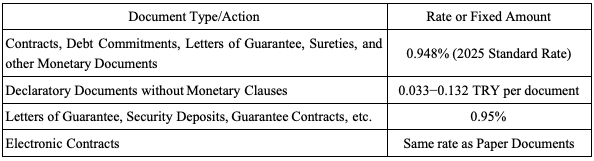

4.4 Stamp Tax (Damga Vergisi)

In scenarios like OTC trades, custody partnerships, or proxy investment agreements, if docs have legal force and state amounts, they theoretically need stamp tax under the law.

5 Summary

Looking back, Turkey's crypto asset scene has a clear two-sided vibe: On one hand, the market's buzzing with high activity from retail and institutional investors; on the other, regulations are getting stricter, with the government pushing for compliance and transparency through systems. From Turkey's move to gradually give MASAK more powers, it's clear they've transitioned from banning payments to basic oversight in the global crypto regulatory landscape. Tighter rules don't mean a closed market—instead, they lay the groundwork for a transparent, safe, and long-term crypto investment space. What investors need to do isn't dodge rules, but use records, proofs, and clear fund logic to stay compliant. That's the steadiest way to play in Turkey's crypto market for the next few years.

[1] GİB: Law No. 5520 on Corporate Tax

[2] GİB: Law No. 193 on Income Tax

[3] GİB: Law No. 3065 on Value-Added Tax

https://mevzuat.gov.tr/mevzuatmetin/1.5.3065.pdf

[4] GİB: Law No. 488 on Stamp Tax

https://mevzuat.gov.tr/mevzuatmetin/1.5.488.pdf

[5] DTA Implementation Reference

https://www.gib.gov.tr/yurtdisi-ile-cifte-verginin-onlenmesi-anlasmalari

[6] OECD AEOI Status of Commitments – Turkey Page

[7] https://www.chainalysis.com/blog/2025-global-crypto-adoption-index/

[8] https://www.ainvest.com/news/turkey-imposes-crypto-transfer-limits-licensing-rules-2506/

[9] https://www.oecd.org/tax/exchange-of-tax-information/crypto-asset-reporting-framework.htm

[10] https://aksan.av.tr/blockchaincryptocurreny-regulation-2024-turkiye-turkey

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.