Web3 Digital Funds Topic:Comparison of Tax Risk Analysis Easily Ignored

As a world famous offshore financial center, Cayman Islands is also the world's largest offshore fund establishment, more than 85% of offshore funds are registered in Cayman Islands. At the same time, Cayman p…

As a world famous offshore financial center, Cayman Islands is also the world's largest offshore fund establishment, more than 85% of offshore funds are registered in Cayman Islands. At the same time, Cayman provides very favorable tax policies, funds in the Cayman Islands do not need to pay income tax, capital gains tax, dividend tax, etc.; it has also signed tax information exchange agreements with the United Kingdom, the United States, Australia and other countries. According to the Cayman Islands Monetary Authority (CIMA), as of year-end 2020, there were 2,6351 regulated open-ended funds and 9,857 regulated closed-ended funds in the Cayman Islands, with total assets of these funds exceeding US$2 trillion. The number of exempted funds established in Cayman is even greater.

Registering a fund in Cayman has become an important way of cross-border investment, and setting up a private equity fund to invest in digital assets is also gradually favored by Web3 investors. This article focuses on three structures for setting up offshore funds for investment in Cayman and analyzes the tax risks designed under the LP (limited partnership) structure.

1 Three typical forms of organization of Cayman funds

Cayman exempted funds mainly exist in the following organizational forms: Exempted Company (EC), and Exempted Limited Partnership (ELP). This article first selects the more typical three fund structures for analysis.

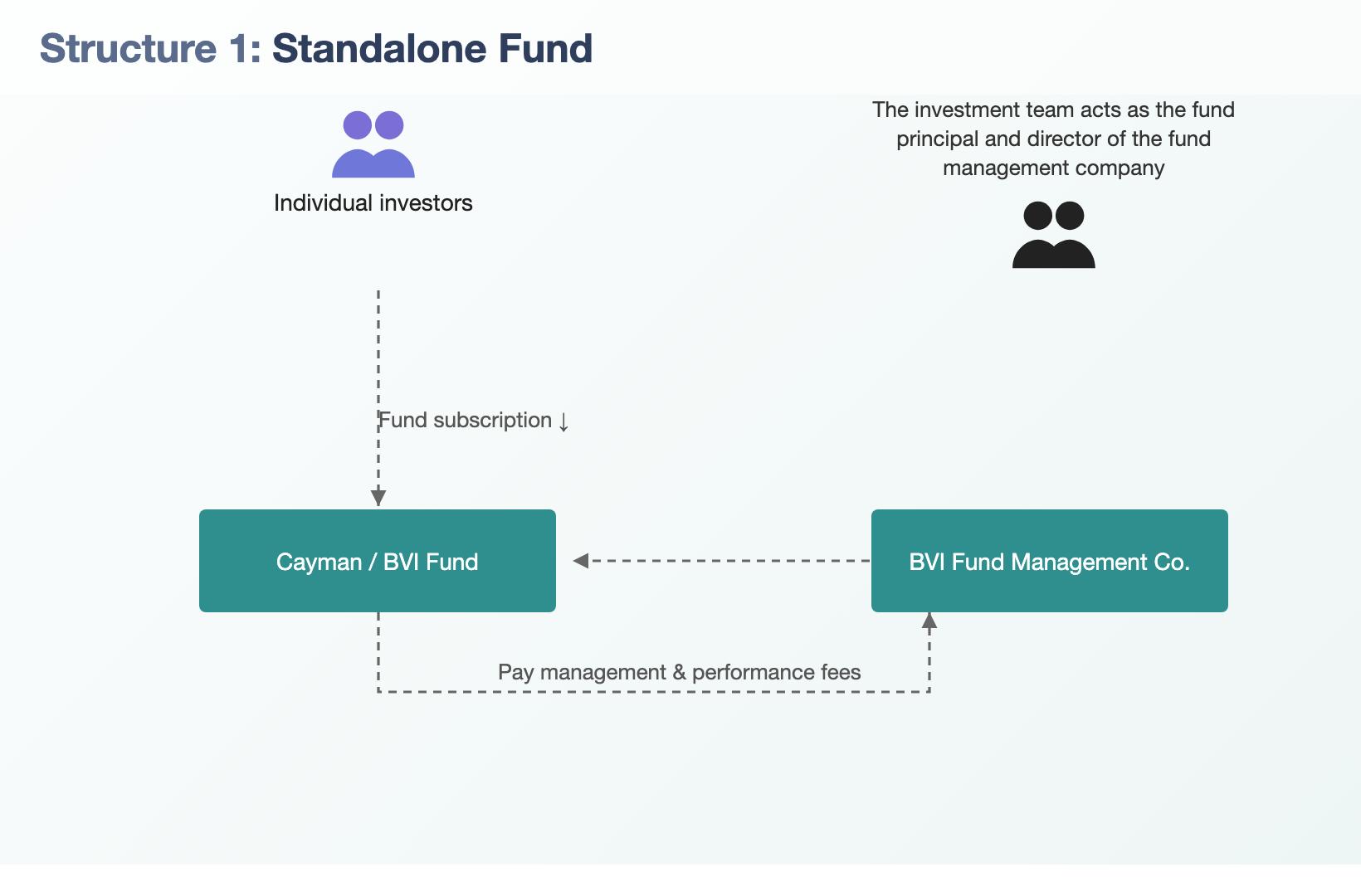

1.1 Stand-Alone Fund Structure

There are two entities in a single fund, where the fund entity is usually set up as an exempted limited partnership, with the investment team subscribing to participatory shares in the fund (with the right to dividends, but without the right to vote). At the same time, the investment team establishes a fund management company in the British Virgin Islands (BVI), which acts as the fund's managing shareholder (with no right to participate in dividends, but with the right to vote at general meetings), while the day-to-day decision-making and operation of the fund is vested in the fund's board of trustees, which is chaired by the investment team.

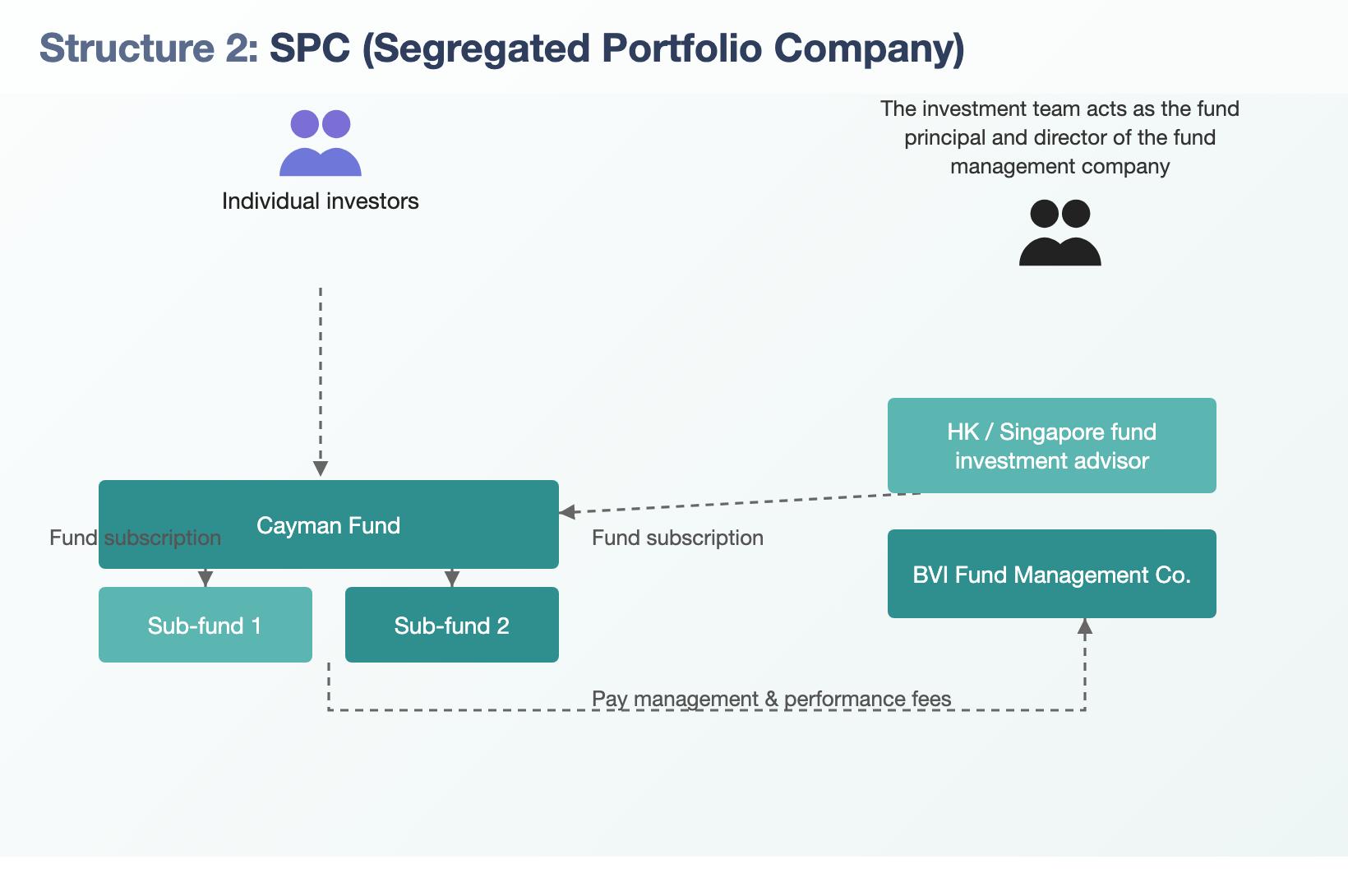

1.2 Standalone Portfolio Company (SPC) Structure

The Segregated Portfolio Company (SPC) is a special case within the EC structure and a unique form of Cayman law. In the SPC structure, as an exempted entity, the SPC can set up as many as 25 Segregated Portfolio (SP), and at the same time, these portfolios are completely independent of each other in terms of assets and liabilities. The practical effect of operating a number of different funds under an SPC is similar to setting up a number of single funds, making the SPC more cost-effective. The specific SPC structure is shown below.

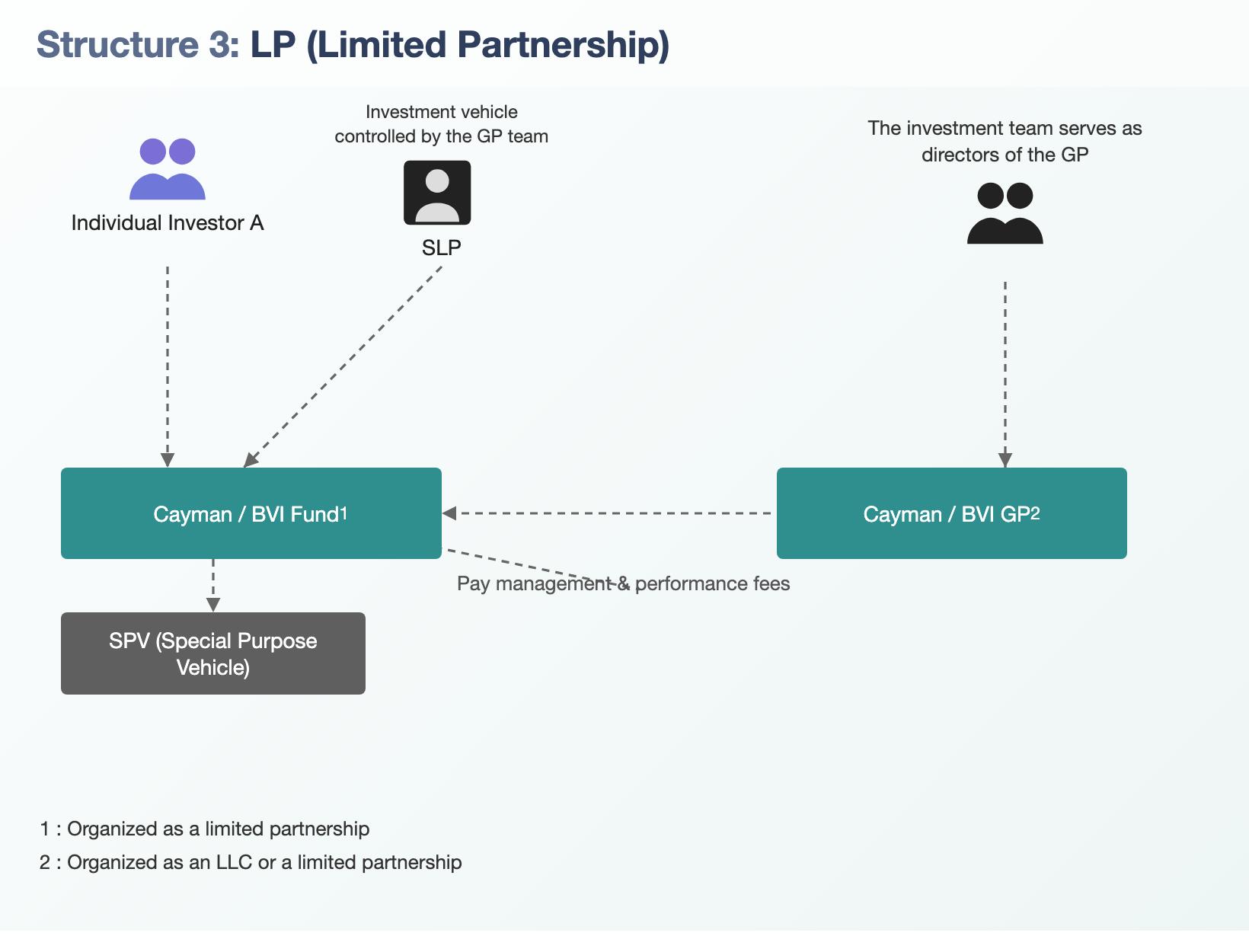

1.3 Exempt Limited Partnership (ELP) Structure

The ELP structure is divided into three main steps, one of which is that the investor first establishes a GP (General Partner) company in Cayman/BVI as the general partner of the ELP. Secondly, the ELP fund entity is formed by individual investors, the GP company established in the first step and the SLP (limited partner), which is an investment entity controlled by the GP team. The ELP then establishes an SPV (Special Purpose Vehicle) to carry out the investment business. Among other things, the GP has management and control over the ELP fund affairs and is responsible for the operation, management, control and conduct of fund business of the ELP fund.

An SPV under a fund entity is a subsidiary or sub-partnership set up by a fund entity to invest in a project, usually also in the form of an ELP, with the fund entity as the general or limited partner and the project parties as the limited or general partners.The ELP structure can offer the following benefits:

Avoid double taxation and exchange controls by utilizing the favorable tax policies of the Cayman Islands.

According to the characteristics and needs of different projects, we flexibly design the SPV's investment strategy, income distribution, exit mechanism, etc., and protect the interests of investors and project parties.

Like SPCs, ELPs can account for the risks and benefits of different projects separately, avoiding interactions and improving transparency and efficiency.

2 Selection of SPV locations under the ELP architecture

Under the ELP structure, the fund entity reaches its investment in the downstream enterprise through an SPV, which is able to liquidate independently, protect shareholders' rights and interests, and realize risk isolation. In practice, the choice of SPV location is generally landed in Hong Kong or Singapore, which is convenient to carry out financial activities, and also can obtain the low tax rate concessions of the two places. This paper analyzes the impact of four factors, namely, interest, dividend, property gain and stamp duty, on the choice of SPV location, as shown in the table below.

Key considerations

a concrete analysis

Are there tax advantages

HK

Singaporean

interest (on a loan)

In Hong Kong and Singapore, the tax implications of interest income/payments are broadly similar.

be

be

dividend

Dividends distributed by the project company to an offshore SPV may be eligible to claim a DTA, reduced withholding tax of 5%, if the SPV qualifies as a beneficial owner of the dividend under the expanded safe harbor rules and is able to obtain a Certificate of Tax Residence (CoR) from the Hong Kong/Singapore tax authorities.

Based on the observation of past cases, it is currently easier for Singapore resident companies to obtain CoRs than Hong Kong resident companies.

clogged

be

Proceeds of property

Qualifying investment disposals are not subject to capital gains tax in Hong Kong and Singapore.

be

be

non-residential property

(1) Hong Kong stamp duty will be levied on the sale of shareholdings in Hong Kong listed companies in the capital exit segment, except for the adoption of Option 2 structure (described later), and the sale of shares in a BVI or Cayman Islands company.

(2) No stamp duty is levied on paperless shares traded on the Singapore Exchange.

clogged

be

It can be seen that in terms of dividend and stamp duty, Singapore as the SPV landing point has more cost advantages than Hong Kong: the dividend tax relief for SPVs in Singapore is more lenient; and its stamp duty provisions are more concise and low-cost. However, transaction cost is only one of the considerations of SPV landing point, and the specific landing choice should be judged according to different industries, structures and corresponding policies of the two places.

3 Three segments of ELP structure investment and tax risk analysis

3.1 Taxation of the investment chain

The investment segment is divided into three main steps: setting up an offshore structure, setting up a domestic asset management company and a Wholly Owned Foreign Enterprise (WOFE), and acquiring a project company. There are fewer tax issues involved in this segment.

Setting up an offshore structure can be broadly categorized into the following two options: Option 1 is the simplified Cayman structure, i.e., setting up a holding company in the Cayman Islands and then investing in offshore or onshore project companies or special purpose entities through the company; Option 2 is the BVI/Cayman - Cayman structure, i.e., setting up a holding company in the Cayman Islands and setting up a sub-holding company in the British Virgin Islands (BVI) or Cayman, and then invest in offshore or onshore project companies or special purpose entities through the sub-holding company.

The advantages of Option 1 are simple structure, low cost and easy management. Only one holding company needs to be registered and maintained in Cayman, there is no need to register and maintain another holding company in BVI, as well as enjoying Cayman's tax benefits. However, its disadvantages are higher risk, less confidentiality and less flexibility. If the Cayman holding company invests directly in projects in other countries, it may be restricted or regulated by the laws of other countries. If the Cayman holding company is listed, it may expose information about its investors and investment projects. If the Cayman Holding Company needs to change its investment strategy or exit the project, there will be additional costs.

The advantages of Option 2 are lower risk, better confidentiality and higher flexibility. By setting up a sub-holding company in BVI or Cayman, it can isolate the risk between the Cayman holding company and the investment project; this structure also provides a higher level of confidentiality and does not require the disclosure of information about its directors, shareholders and beneficial owners. By setting up a sub-holding company in BVI, it can flexibly design the SPV's investment strategy, income distribution, exit mechanism, etc. according to the characteristics and needs of different projects, and protect the interests of investors and project parties. The disadvantages are complicated structure, high cost and troublesome management. It is necessary to register and maintain two holding companies in two regions, which increases compliance risks and management difficulties.

Enterprise Life Cycle

move

Cayman

Offshore Special Purpose Entity (offshore SPV)

HK

Singaporean

Phase I.

Investment links

Building an Overseas Structure

No tax treatment

No tax treatment

No tax treatment

Establishment of Domestic Asset Management Companies and Wholly Owned Foreign Enterprises (WOFE)

Acquisition of project companies

3.2 Taxation of production and business operations

Production and operation is the direct source of profit and the main channel for controlling tax risks. In general, Hong Kong has a more streamlined tax policy and imposes a lower tax burden on enterprises. Singapore has higher tax rates on certain tax-related items, such as bank interest income and cross-border interest payments. The tax provisions in Hong Kong and Singapore for different tax-related items are shown in the table below.

Enterprise Life Cycle

Tax-Related Items

Cayman/BVI

HK

Singaporean

①Offshore special purpose entities

Phase II

Production and Business Segment

Operating income (assuming that the offshore SPV has only passive bank interest income)

No tax treatment

(1) Hong Kong bank interest income is tax-deductible if the conditions are met

(2) Non-Hong Kong bank interest income not taxable

1) Corporate income tax at 17% on interest income from Singapore banks

(2) Non-Singapore bank interest income is not taxable unless the recipient of the income is in Singapore or is deemed to be in Singapore

Interest payments

1) No withholding tax

2) Not deductible if the loan is used for investments

1) Cross-border interest payments are subject to a withholding tax of 15% (except where a tax treaty applies)

2) Deductible for income tax purposes

dividend distribution

no withholding tax

no withholding tax

dividend income

untaxable

not liable taxation (of monastery, imperial family etc)

② Shareholders of offshore asset management companies

untaxable

Corporate income tax at 17%

3.3 Taxation of the capital exit chain

In the capital exit segment, Option 1 and Option 2 face different tax issues. Overall, there is not much difference between the two exit scenarios in terms of taxation, except that Scenario 2 has an additional layer of BVI sub-holding company, which does not have much impact on taxation.

As shown in the table below, no tax is payable in the Cayman Islands on the disposal of either the holding company or the SPV. When exiting an investment in Hong Kong, only the disposal of a listed Cayman holding company with an SPV is subject to stamp duty, and at a low rate of 0.1% for each party, the buyer and the seller. All other types of disposals are not subject to tax. When exiting an investment in Singapore, only the disposal of the SPV is subject to stamp duty, at a rate of 0.2% for the buyer. All other types of disposals are not subject to tax.

Enterprise Life Cycle

situations

Cayman

HK

Singaporean

Phase III

Capital exit links

Option 1: Simplified Caymanian structure

1a) Disposal of Cayman holding company (pre-listing)

No tax treatment

No tax treatment

No tax treatment

1b) Disposal of Cayman holding company (post-listing)

Stamp duty at 0.2% (i.e. 0.1% to be borne by the parties to the contract) on the sale of shares

No tax treatment

2) Disposal of offshore special purpose entities

Stamp duty at 0.2% of the higher of the value of the shares or the purchase consideration (i.e. borne by the buyer)

3a) Disposal of project company - equity transaction

Income in the nature of property gains is not taxed

3b) Disposal of the project company - asset trading

No tax treatment

4) Disposal of domestic asset management companies

Option 2: BVI/Cayman - Cayman structure

1a) Disposal of Cayman/BVI holding company (before listing of Cayman holding company)

No tax treatment

No tax treatment

No tax treatment

1b) Disposal of BVI holding company (after listing of Cayman holding company)

No stamp duty impact

No tax treatment

4 Extension and discussion

4.1 Risk of separation of the place of physical management from the place of incorporation

The actual management organization of offshore funds is often set up in Hong Kong or Singapore, which gives rise to tax risks due to the inconsistency between the location of the management organization and the place of incorporation. Considering that the Cayman Islands does not have a DTA with Hong Kong or Singapore, the actual tax situation will be even more complicated.

The main tax risk of a Cayman offshore fund is that it may be deemed to be tax resident or to have taxable income in the place where it is physically managed, and thus be subject to income or other taxes in that place. The treatment of this risk depends primarily on the tax laws of the location of the entity, and different jurisdictions may apply different criteria and tax principles. Therefore, when choosing the location of the actual management institution, the offshore fund should fully understand and compare the tax regulations of these regions, so as to choose the most favorable region, or take corresponding measures to avoid or reduce the tax risk.

Singapore's tax laws provide that whether a company is tax resident in Singapore depends primarily on whether the company is controlled and managed in Singapore. Control and management in this context refers to the location of the company's highest level of decision-making, which is usually where the company's board of directors meets. Therefore, if the actual management of a Cayman offshore fund is located in Singapore, then it may be considered to be controlled and managed in Singapore and thus become a tax resident of Singapore. Tax residents of Singapore are subject to global income tax (at a rate of 17%) in Singapore.

Under Hong Kong's tax law, whether a company is liable to profits tax in Hong Kong depends primarily on whether the company's profits are derived from a trade, business or undertaking in Hong Kong, i.e. whether the company's profits have a substantial connection with Hong Kong. Therefore, if the de facto manager of an offshore fund is located in Hong Kong, its investment income may also be deemed to be "sourced in Hong Kong" and thus subject to Hong Kong profits tax (at a rate of 16.5 per cent).

In addition to tax risks, regulatory and legal risks are also issues of concern during the investment process. Firstly, if the financial regulator in Hong Kong or Singapore determines that the offshore fund is engaged in financial service activities locally, the fund entity may be required to comply with the regional financial regulatory regulations, including but not limited to obtaining the appropriate licenses, disclosing the relevant information, and being subject to inspections by the regulator. Secondly, the actual management organization will need to comply with the relevant legal requirements locally and may also have to deal with litigation or arbitration under the local legal framework, which will require dealing with jurisdictional and applicable law issues.

4.2 Risks to the Fund's investments arising from the Cayman Economic Substance Bill

The Cayman Economic Substance Bill is a law enacted by the Cayman government in December 2018 and coming into effect in January 2019 in order to comply with the OECD's requirements for tax transparency and fair competition, and in particular to respond to international standards put forward by the OECD to combat the erosion of tax bases and the shifting of profits from geographically mobile activities. The Act requires Relevant Entities incorporated in Cayman to pass the appropriate Economic Substance test in respect of the Relevant Activities they undertake or risk fines and even write-offs, and the local tax authorities may exchange information on such Relevant Entities to the ultimate beneficiaries. The local tax authorities may exchange information on such Relevant Entities to the tax authorities in the place where the ultimate beneficial owner is located.

This article organizes the relevant requirements of the Economic Substance Act for different subjects and the risk points in actual operation as shown in the table below. Among the four types of investment entities, offshore asset management companies, general partner funds and funds are not subject to the economic substance requirement, but there are corresponding risky operations that may be subject to the economic substance requirement. A Cayman holding company is subject to the (reduced) economic substance requirement and is only required to have sufficient personnel and office space in Cayman to hold and manage the other entities and can satisfy the economic substance requirement through its registered agent. The "Economic Substance Risk Point" in the table refers to the point at which, as a result of the execution of certain operations, the subject changes from not being subject to the Economic Substance Requirement to being subject to the Economic Substance Requirement; or is not allowed to benefit from the Reduced Economic Substance Test. Investors should therefore pay close attention to such risk points in the course of their investments and consult a professional if necessary.

Cayman Economic Substance Bill

Cayman subject

Whether subject to the economic substance requirement

Economic material risk points

Offshore Asset Management Company

(tax resident outside the Cayman Islands)

×

1) Executing investment decisions at will

2) Providing services to entities within the group

3) Issuing interest-bearing loans and deriving income from financing activities

Investment funds

×

Operating activities and assets extend beyond passive investment activities related to the Fund

ELP Fund

×

Change in status of exempt limited partnership

Cayman Holding Company

(non-domestic companies)

√

(may apply "reduced economic substance test" with attention to economic substance risk)

1) Holding shares solely for the purpose of receiving dividends or property gains

2) Engaging in other activities or other types of business, or holding shares or other assets other than similar participations

4.2 Discussion and outlook

The Cayman Economic Substance Act is a legal risk that cannot be ignored by investors and managers of funds established in Cayman. Failure to comply with the Economic Substance Requirement may affect the tax status of the fund, add additional disclosure obligations and even lead to the write-off of the fund. Therefore, investors and managers need to choose and design the structure and operation of the fund in a reasonable manner according to their specific circumstances. At the same time, they also need to pay close attention to the further interpretation and implementation of the Economic Substance Act by the Cayman government and tax authorities to adjust and optimize their fund strategies in a timely manner.

Setting up a fund in Cayman to invest in digital assets has corresponding potential and prospects while also facing many challenges and risks. Therefore, investors and managers need to fully understand the characteristics and laws of digital assets, and reasonably allocate and manage their digital asset portfolios in order to achieve long-term stable investment returns.

This article analyzes and compares three structures for setting up a fund in Cayman to invest in digital assets from a tax perspective only. In practice, investors and managers also need to consider various factors according to their specific objectives and needs, and choose the fund structure that best suits them.

Send this FinTax note to your team.