Ethiopia has become a mining hotspot Tax-related analysis of mining enterprises

Ethiopia became the first African country to start bitcoin mining, and although Ethiopia still bans cryptocurrency trading, it approved laws in favor of mining in 2022, allowing "high-performance computing" an…

Ethiopia became the first African country to start bitcoin mining, and although Ethiopia still bans cryptocurrency trading, it approved laws in favor of mining in 2022, allowing "high-performance computing" and "data mining", and in 2023, Ethiopia ranked fourth among the top destinations for bitcoin mining equipment, behind the United States, Hong Kong, and Asia, according to bitcoin mining services company Luxor Technologies. And according to its estimates, Ethiopia has become one of the world's largest recipients of bitcoin mining machines. This article analyzes Ethiopia's crypto tax system, with a particular focus on the types of taxes and tax rates that mining companies may be involved in.

1 Taxation issues related to mining

1.1 The Concept of Mining

Mining is the act of acquiring digital currency. It is a way to solve complex mathematical problems in the network through computer operations in order to earn rewards. In the field of cryptocurrencies such as Bitcoin, mining is widely used. To put it simply, mining is a computational act carried out in order to obtain a certain digital currency.

1.2 Mining Income

Mining revenue refers to the rewards earned by using computer equipment to participate in the consensus mechanism of the cryptoasset network, validate transactions, or create new units of cryptoassets. There are two sources of mining revenue: a fixed block reward, where a miner receives a certain amount of crypto assets every time a new block is added to the blockchain, and a variable transaction fee, where a percentage or amount of each transaction is paid to the miner who verifies the transaction. The method of calculating mining revenue depends on the consensus mechanism used, and there are two main types: Proof of Work and Proof of Stake.

1.3 Tax issues in mining

The tax treatment of cryptocurrency mining business mainly depends on the definition, asset classification, and recognition and measurement of mining income and expenses in the country or region where it is located. The taxes involved in mining income vary from country to country, and the main taxes involved are as follows:

Firstly, direct tax, i.e., income tax and capital gains tax on mining income. In most countries where mining business is involved, mining income is treated as business income of enterprises or individuals and subject to corporate income tax or personal income tax. The tax rate is determined by the identity of the miner (individual or enterprise), income level, and place of residence, among other factors.

Secondly, indirect tax, i.e., value-added tax (VAT) or goods and services tax (GST) on mining income. Currently, there is no unified opinion among countries or regions on whether to levy value-added tax (VAT) or goods and services tax (GST) on mining income. In the European Union, most countries believe that mining activities are not subject to VAT. In Israel, however, according to the taxation regulations issued in 2017 on virtual currency activities, mining activities are considered to be providing services and subject to 17% VAT. In New Zealand, mining activities are also considered to be providing services and subject to 15% GST.

Some countries impose consumption tax on mining companies for reasons such as industry resource adjustment. For example, the US, according to the "Supplemental Budget Information" issued by the US Treasury Department in March 2023, one of the clauses suggests levying consumption tax in stages based on the cost of electricity used in cryptocurrency mining. These companies will be required to report their electricity consumption and the type of electricity used.

2. Advantages of Mining in Ethiopia

Hit by political and economic setbacks, bitcoin miners are usually attracted by governments that offer cheap electricity costs and are friendly to the cryptocurrency industry. Ethiopia, although it still bans cryptocurrency transactions, has allowed bitcoin mining since 2022. For all companies engaged in cryptocurrency mining, Ethiopia has become an unprecedented opportunity, so a brief analysis of the advantages of mining in Ethiopia will be presented below. 2.1 Strong opposition from other countries to cryptocurrency mining

Due to reasons such as climate change and power shortages, there is strong opposition from other countries to cryptocurrency mining. For example, Kazakhstan and Iran, among a series of developing countries, initially accepted Bitcoin mining, but when its energy use sparked domestic dissatisfaction, the policy shifted to non-support and opposition. In 2021, the Chinese government also banned Bitcoin mining. Most countries ban cryptocurrency mining. Because countries may run out of available power, thereby leaving miners with no room for expansion. Secondly, miners may suddenly be viewed as unwelcome by the government and forced to leave.

2.2 Cheap electricity

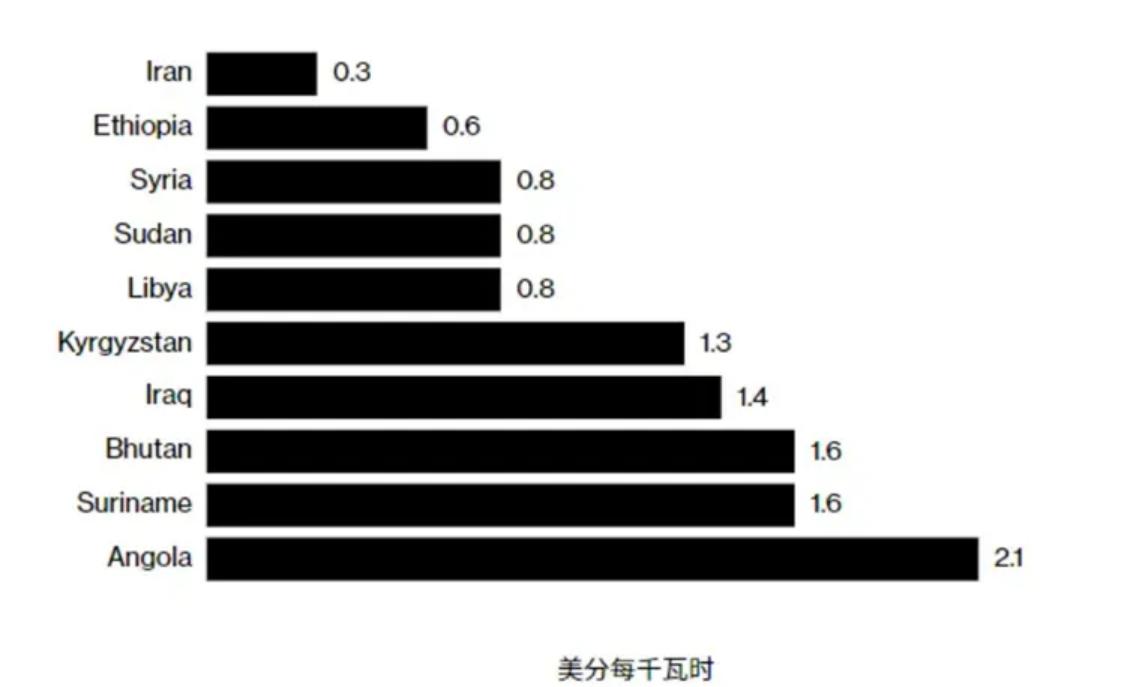

Bitcoin mining will use a lot of electricity, and electricity accounts for up to 80% of miners' operating costs, so obtaining cheap electricity is a key competitive advantage for mining. In 2023, Bitcoin mining consumed 1.21 trillion kWh of electricity, and the dependence on abundant electricity is its main weakness, because the dependence on electricity may squeeze power use for factories and households, thereby putting mining enterprises under political opposition. Ethiopia has cheap electricity, as shown in the figure (source: Statista Research Department). The Ethiopian National Electric Power Corporation stated that it has signed power supply agreements with 21 Bitcoin miners, of which 19 are from China.

2.3 Ideal resources and climate conditions

In the context of global warming, although miners claim that they are increasingly using clean energy, bitcoin mining is increasingly being seen as a factor in global warming. A study published by the United Nations shows that two-thirds of the electricity used for bitcoin mining in 2020 and 2021 was generated from fossil fuels.

Ethiopia can take advantage of its abundant surplus green energy and renewable energy to provide electricity to its citizens through bitcoin mining. Ethiopia's ability to provide power for bitcoin mining could be on par with Texas within a few years. The completion of the GERD project will increase Ethiopia's generating capacity to 5.3 gigawatts, doubling its generating capacity. Ethiopia's advantage is not just in cheap renewable energy. Its climate conditions are also ideal, with the ideal mining temperature being between 5 and 25 degrees Celsius, which coincides with Ethiopia's average temperature.

2.4 Ethiopian government's attitude

The Ethiopian government allows bitcoin mining mainly because these mining companies pay for the electricity they consume in foreign currency, and the electricity company charges bitcoin miners a fixed rate of $3.14 per kilowatt-hour, which is a profitable source of foreign exchange income. Expanding foreign exchange inflows to alleviate economic challenges, and viewing the mining industry as an attractive investment opportunity. According to Project Mano, integrating bitcoin mining into the Ethiopian economy could contribute $2 billion to $4 billion to its GDP. Accepting bitcoin mining can largely block the path of mining breaking through foreign exchange controls. It can also create employment, increase tax revenue, and reduce the amount of water released during the flood season at hydroelectric power stations.

3. Taxation study of mining enterprises in Ethiopia

3.1 Tax system in Ethiopia

3.1.1 Tax structure

Ethiopia has a system of federal and state government sharing tax revenue. Each state is required to pay a certain percentage of its tax revenue to the federal government. The federal government distributes funds to the states based on population, economic conditions, and the amount of taxes paid.

Central taxes include customs duties and other taxes on goods imported and exported; personal income tax for employees employed by the central government or international employers; corporate income tax, personal income tax, and value-added tax on profits of enterprises owned by the central government; taxes on national lottery income and other winnings; taxes on airplane, train, and sea transportation activities; taxes on rental income from houses and properties owned by the central government; taxes on licenses and services issued or granted by the central government. The central government and local governments share taxes, including corporate profit tax, personal income tax, value-added tax, royalties, and land rent taxes for large-scale oil, gas, and forest resource extraction.

3.1.2 Taxes that Ethiopian mining enterprises may be subject to:

(1) Enterprise Income Tax

Any enterprise that obtains income within Ethiopia is required to pay enterprise income tax. Taxpayers are divided into three categories: A-class taxpayers, B-class taxpayers, and C-class taxpayers. Of which, enterprise income taxpayers are classified as A-class taxpayers. Based on the nature of the income, the Income Tax Law has divided it into five categories: A-category income, B-category income, C-category income, D-category income, and E-category income. Of which, the enterprise income taxpayers are involved in the following types of income: B-category income (30%), C-category income (30%), D-category income (10% or 5%), and E-category income (exempt).

(2) Value Added Tax (VAT)

The scope of value-added tax (VAT) in Ethiopia is the provision of goods and services, importation of taxable goods, and certain imported services. VAT taxpayers are divided into obligatory registrants and voluntary registrants based on the total value of taxable transactions. Value-added tax is calculated on a net basis, and when input tax exceeds output tax, the taxpayer may choose to carry forward the excess, claim a refund of VAT, or offset it against other taxes. The tax rate is divided into two tiers, a basic rate of 15% and a zero rate. Value-added tax is reported monthly. Mining companies that involve the transmission or provision of power, including electricity, in the production of heat, power, gas or water, will be subject to value-added tax.

(3) Capital Gains Tax

Capital gains are the profits realized from the transfer of business assets. In Ethiopia, capital gains are classified as D-type income under the income tax law and are subject to income tax (i.e. capital gains tax). The tax rate for buildings used for commercial, factory, or office purposes is 15%; the tax rate for company shares is 30%.

(4) Royalty Tax

In Ethiopia, royalty refers to any payment made as compensation for the use or right to use any literary, artistic or scientific works, including film films, the use of film film in radio or television broadcasting, any patent, trademark, design or model, drawing, secret formula or secret procedure, or any industrial, commercial, scientific equipment, or any payment made as compensation for industrial, commercial, scientific experience information. Royalty tax is levied at a flat rate of 5%. Companies that do not comply with the registration requirements for encryption will be subject to legal action. Meanwhile, INSA has the power to regulate encryption products and related transactions. In addition, INSA will also be responsible for developing operational procedures and building cryptographic infrastructure.

Ethiopia implements a principle of territoriality and residency combined for taxation, any enterprise that obtains income in Ethiopia must pay corporate income tax, and Ethiopian resident enterprises should report and pay corporate income tax on their global income. The mining enterprises that enter Ethiopia are likely to be classified as C-type income or D-type income, with a tax rate of 30%, the type of income to be subject to corporate income tax or profit tax is not yet clearly stipulated in the relevant government documents of Ethiopia. The supply of electricity, heat, etc. in Ethiopia requires the payment of value-added tax, and mining enterprises are extremely dependent on electricity, in fact, they are the actual burden bearers of electricity value-added tax. In essence, the tax on electricity will affect the taxes of mining enterprises. As well as the fact that Ethiopia has not yet clarified how to define the mining behavior of enterprises, if it is defined as providing services or labor, it will also involve the direct payment of value-added tax. Regarding the point of recognizing mining revenue, many opinions hold that cryptocurrency mining represents the intangible assets developed within the mining enterprise, where the miners' investment in computers, electricity, and various employee costs are used to construct and mine, thus the revenue or gain should be recognized upon the subsequent sale of the cryptocurrency. There is no clear regulation indicating that Ethiopia currently has tax incentives for mining enterprises, but mining enterprises may be eligible for some existing tax incentives, such as tax incentives for creating employment. Additionally, if a mining enterprise involves import activities involving mining machines, it will also involve the payment of customs duties, and specific regulations and related tax rates need to be clarified.

Reference:

[1] State Taxation Administration. (2023). China Resident Investment Tax Guide in Ethiopia

[2] TaxDAO. (2023). Which is More Suitable for Cryptocurrency Mining Companies: Hong Kong or Singapore

[3]Techub News.(2023).Chinese Bitcoin Miners Find a New Crypto Haven in Ethiopia

[4]Zheng Mengya, Wang Keko, Wang Zhenni, Yan Huqin. (2021). Research on the Taxation Issues of Cryptocurrencies in the Context of Digital Economy - Taking the Mining Mechanism of Bitcoin as an Example. World Economic Exploration. 2

Send this FinTax note to your team.