Beyond the CBDC: How the New Zealand Government Taxes Cryptocurrencies

1.New Zealand Cryptocurrency Status New Zealand has a relatively open attitude towards cryptocurrencies, with the government recognizing the legitimacy of cryptocurrencies and viewing them as a form of asset a…

1.New Zealand Cryptocurrency Status

New Zealand has a relatively open attitude towards cryptocurrencies, with the government recognizing the legitimacy of cryptocurrencies and viewing them as a form of asset and investment. New Zealand has implemented a strategy to embrace cryptocurrencies, with its Minister of Business and Consumer Affairs Andrew Bayly suggesting that New Zealand needs to develop security and safeguard mechanisms for blockchain citizen data, while he advocates for the government to provide policies and supportive measures to accelerate the development of the crypto industry and address some of the potentially associated risks.

1.1 The current state of cryptocurrency investment

Nearly 50% of New Zealanders own, have owned, or are considering investing in cryptocurrencies in the future, according to research by consumer insights firm Protocol Theory and crypto exchange Easy Crypto. Meanwhile, according to The Fintech Times, nearly half of New Zealanders are still interested in crypto investments as an alternative to property investments, despite the fact that there are still major barriers to understanding and trust.

In addition, the number of holders of cryptocurrency investment products in New Zealand is also on the rise. between March 2023 and April 2024, the number of holders of cryptocurrency investment products in New Zealand rose from 3% to 9.5%. More and more investment institutions have started to provide cryptocurrency investment services, which has contributed to the increase in the number of cryptocurrency users in New Zealand.

1.2 Current state of cryptocurrency regulation

Cryptocurrencies are not considered legal tender in New Zealand, but are considered a form of property. Its regulation of cryptocurrencies is handled by several agencies, with the Reserve Bank of New Zealand (RBNZ) monitoring cryptocurrency development and its impact on the financial system. The Financial Markets Authority (FMA) oversees the trading and issuance of crypto assets and their legal compliance.The FMA plays a crucial role in setting guidelines and regulatory norms for the cryptocurrency industry, which includes approving licenses for the operation of exchanges and ongoing monitoring.

Significant progress has also been made in the regulation of New Zealand's cryptocurrency sector in recent years. The government has recognized the need to adapt existing frameworks to address the unique challenges posed by digital currencies and has developed guidelines for Initial Token Offerings (ICOs) as well as the classification of certain types of crypto assets as financial products. These developments reflect New Zealand's commitment to creating a safe and robust environment for the development of the cryptocurrency industry, while working to safeguard the interests of investors and the integrity of the financial system.

2 Overview of New Zealand's Tax System

2.1 Overview of the Tax System

New Zealand takes income tax as the main tax, supplemented by other taxes to constitute the tax system. The main taxes include: corporate income tax, personal income tax, goods and services tax, fringe benefits tax, employer's social security surtax, accident compensation insurance premiums, customs duty, consumption tax, and withholding tax on contracted works for non-residents. There is no capital gains tax in New Zealand, but the sale of certain assets is taxable under certain circumstances. Cash and personal assets brought into New Zealand from offshore are not taxable.

2.2 Major taxes

2.2.1 Corporate income tax

Taxpayer Type | Scope of Taxation | Definitions

Resident Enterprise | Worldwide Income | A business that meets any of the following conditions. (1) The business is incorporated in New Zealand. (2) the head office of the business is located in New Zealand; and (3) the principal management body of the business is located in New Zealand; and (4) the place where the directors, etc. of the enterprise exercise control within the scope of their authority is in New Zealand (even if the directors sometimes make decisions outside New Zealand)

Non-resident Enterprise | New Zealand-sourced income | Enterprises other than New Zealand resident enterprises

Resident taxpayers are required to file a New Zealand tax return on worldwide-sourced income at a corporate income tax rate of 28%. Non-resident businesses (including branches) are taxed only on their New Zealand-sourced income. Non-resident withholding tax on dividends may apply at 0%, 15% or 30%, depending on the proportion of shares held, whether the dividend is a cash dividend, and other factors.

2.2.2 Personal income tax

Type of Taxpayer | Scope of Taxation | Definitions

Resident Taxpayer | Worldwide source income | An individual who meets any of the following conditions: (1) is a resident of New Zealand for more than 183 days in any consecutive 12-month period; (2) has a continuing relationship with New Zealand; (3) performs services for the New Zealand Government overseas; and (4) has a permanent residence in New Zealand.

Non-resident taxpayer | New Zealand-sourced or deemed New Zealand-sourced income | Individuals who are not New Zealand resident taxpayers

New Zealand's personal income tax is a comprehensive income tax system, with resident taxpayers paying personal income tax on worldwide income and non-resident taxpayers paying on New Zealand-sourced or deemed New Zealand-sourced income. Tax rates are progressive.

2.2.3 Goods and Services Tax

New Zealand's turnover tax is the Goods and Services Tax (GST), a value-added tax (VAT) that applies to the vast majority of transactions involving the sale of goods and the provision of services. There is a threshold for GST to start, which is determined by determining whether a business's monthly revenue exceeds NZ$5,000, and if it does, the business should register as a GST taxpayer. GST rates currently range from 0% to 15%.

2.2.4 Fringe Benefits Tax

The Inland Revenue Department levies Fringe Benefits Tax (FBT) on employers' expenditure on benefits other than wages, and the taxpayer's FBT expenditure can be deducted before tax. There are four different options when calculating the fringe benefit tax rate:Single rate (63.93%), Simplified Alternative Rate (63.93%, 49.25%), Full Alternative Rate (11.73%-63.93%), and Combined Alternative Rate (63.93%, 49.25%).

2.2.5 Employer social security surtax

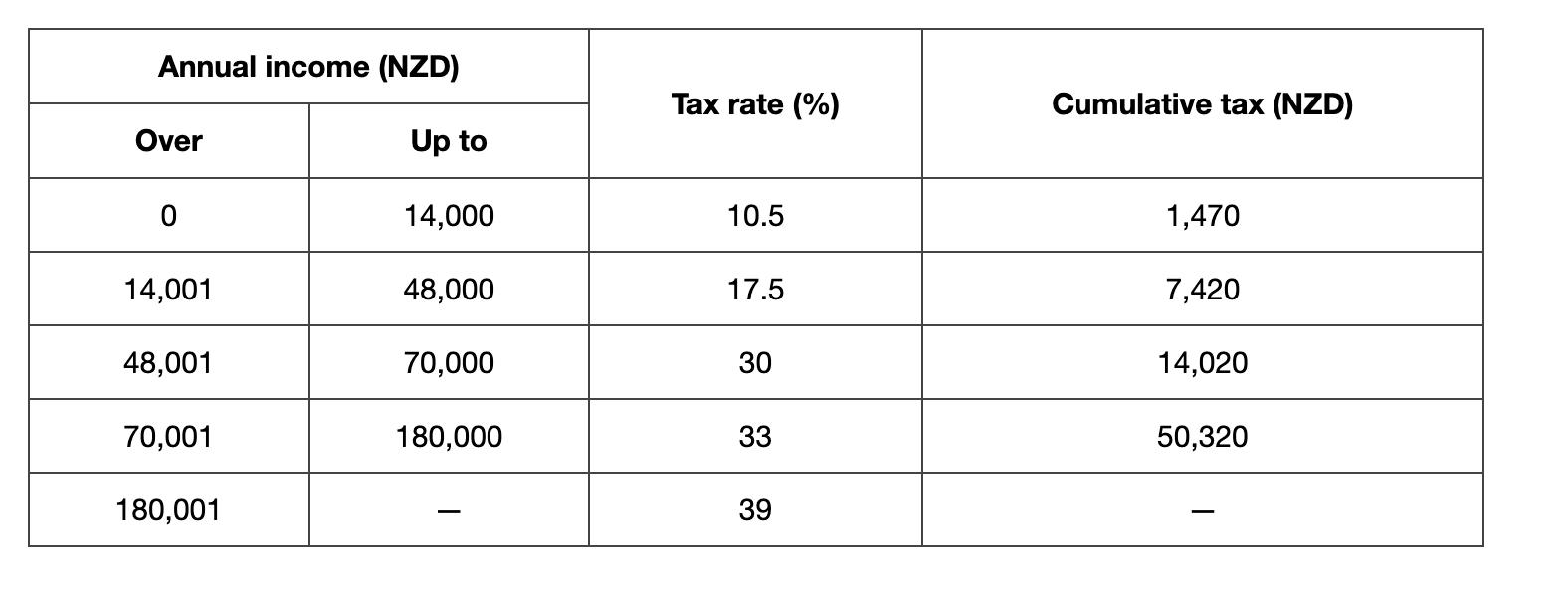

The New Zealand Inland Revenue imposes the Employer's Social Security Surcharge Tax on employers' contributions to approved social security funds (excluding foreign social security) on behalf of their employees. The tax rate is a progressive tax rate based on the employee's annual salary for the previous year plus the total amount of employer's social security fund payments on behalf of the employee. The tax rates range from 10.5% to 39%.

2.2.6 GST

In addition to GST, New Zealand levies excise taxes on alcoholic beverages (e.g. wine, beer and spirits), tobacco and certain fuels (e.g. compressed natural gas, gasoline).

2.2.7 Gift tax

Gifts made on or after October 1, 2011 are not subject to gift tax. For gifts made before October 1, 2011, a gift statement is required for all gifts with an aggregate value of more than NZ$12,000 in any 12-month period, and gift tax is payable on gifts totaling more than NZ$27,000 in any 12-month period. The tax rate is 0-25%.

3. New Zealand Cryptocurrency Taxation Compendium

3.1 Taxes involved in cryptocurrencies

3.1.1 Personal or corporate income tax

The New Zealand government has recognized the legitimacy of cryptocurrencies and considers them as a form of asset and investment. Therefore, income from cryptocurrencies earned through holding, trading and mining is legal and subject to tax. According to the IRS, gains from the sale and trading of cryptocurrencies should be reported as “taxable income” and taxed according to individual or corporate income tax brackets. The tax rates range from 10.5% to 39%, depending on income. For those holding cryptocurrency as a long-term investment, capital gains are not subject to income tax under current regulations.

Taxpayers can offset cryptocurrency losses from other sources of income. However, this offset only applies if the cryptocurrency is acquired for the purpose of disposal (e.g., sale or trade).

3.1.2 Goods and Services Tax

Transactions and sales of cryptocurrencies are not subject to GST. However, if the cryptocurrency is used to pay for goods and services, it may be subject to GST. The GST rate is 15%.

3.1.3 Gift Tax

Giving cryptocurrency as a gift/receiving cryptocurrency as a gift is subject to a gift tax of 0-25% depending on the value.

3.2 Cryptocurrency Tax Benefits

New Zealand's cryptocurrency tax policy does not currently have specific incentives directly targeting cryptocurrencies, but there are some general tax-related provisions and incentives that may apply in certain circumstances.

Transitional Tax Resident Benefit: For new tax residents, it may be possible to be treated as a transitional tax resident and enjoy a four-year tax exemption on foreign income, which includes cryptocurrency income. However, the sale of cryptocurrency on a New Zealand exchange is not exempt from these taxes.

Small Business Tax Credit: Generally, New Zealand grants certain tax benefits to qualifying small businesses. If cryptocurrency trading activities are considered part of a small business, it may be possible to apply these benefits.

Personal Income Tax Loss Credit: Taxpayers may be able to offset cryptocurrency losses from other sources of income. However, this credit only applies if the primary purpose of acquiring the cryptocurrency is disposal (e.g., sale or trading).

3.3 Cryptocurrency Tax Compliance

Businesses dealing with cryptocurrencies face more complex compliance requirements. These include keeping detailed records, complying with anti-money laundering and combating the financing of terrorism (AML/CFT) regulations and meeting GST obligations. The Inland Revenue Department (IRD) provides guidelines for businesses that emphasize the importance of transparency and compliance with the existing legal framework. This includes guidance on how to handle cryptocurrencies for GST purposes.

4 Conclusion

Overall, the New Zealand cryptocurrency market is vast and the cryptocurrency tax policy is comprehensive, providing clear norms and guidance for cryptocurrency holders, investors, and traders.2024 On April 17th, the New Zealand Federal Reserve announced that it had officially launched a call for opinions on the issuance of a New Zealand digital currency in the hope that this would provide a full understanding of the market's, businesses', and individuals' views and demand, and further promote the development and innovation of financial technology. The New Zealand digital currency here refers to the Central Bank of New Zealand Digital Currency (CBDC) rather than decentralized cryptocurrency, which indicates that while accepting decentralized cryptocurrencies, the New Zealand government also wants to actively explore the field of centralized central bank digital currency. As the New Zealand Federal Reserve has indicated, it seeks to establish a more complete, efficient and secure payment system to meet the development needs of the digital era,while also strengthening supervision and committing itself to creating a safe and sound environment for the development of digital currencies, and striving to safeguard the interests of investors and the integrity of the financial system. In the future, in the context of the coexistence of decentralized cryptocurrencies and central bank digital currencies, how to deal with the relationship between the two, how to give good play to the respective advantages of the two, and how to build a supporting compliance and regulatory system will be issues that the New Zealand government will need to carefully consider.

参考文献

[1].国家税务总局.(2023).中国居民赴新西兰投资税收指南

[2].TaxDAO.(2023).新西兰加密资产税收概览

[3].Cryptopolitan.(2024).New Zealand embraces strategic approach to crypto

[4].StacksOnChain.(2024).Best Crypto Exchanges New Zealand

[5].Cryptopolitan.(2024).Crypto Industry in New Zealand: Legitimized by Small-Scale Investors

Send this FinTax note to your team.