On Eastern Time August 7th, US President Trump signed an executive order at the White House called Democratizing Access to Alternative Assets for 401(k) Investors. It requires the Treasury Department, Labor Department, and Securities and Exchange Commission (SEC) to kick off rule changes, bringing crypto, real estate, private equity, and other “Alternative Assets” into the mix for 401(k) pension investments. This news struck global financial markets like a seismic shock—it could unlock a whopping $8.7 trillion retirement capital pool and is seen as a key move for crypto assets shifting from fringe experiments to mainstream finance.

While the White House claims this is all about “giving retail investors better access to diverse assets,” a core question pops up: Is this opening a fresh chapter for wealth growth in Americans’ retirement futures, or just a reckless nationwide bet?

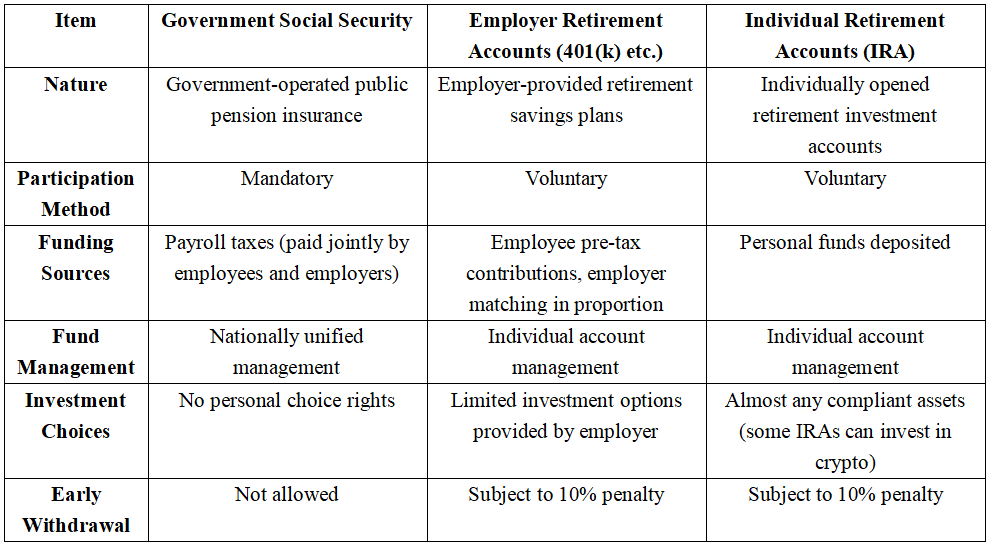

1. 401(k) Plans: The Foundation of America’s Retirement System

To grasp why this matters so much, you've got to understand the role of 401(k) in the US retirement safety net. America's pension system has three main pillars: The first is the government-run mandatory Social Security, which pays out basic pensions monthly to retirees; the second is employer-provided retirement savings plans, with 401(k) being the most common—employees contribute pre-tax, employers match, and funds build up together with limited investment choices from the employer; the third is Individual Retirement Accounts (IRA), set up voluntarily by individuals, with a broader investment scope, and some types of IRAs already allow crypto investments.

In the second pillar, 401(k) is the most iconic employer retirement scheme—most employers support employee participation, building funds through payroll deductions and matching contributions for compound growth. Besides 401(k), there’s also the 403(b) plan for public education institutions and some nonprofit employees. As of the first quarter of 2025, the US 401(k) market size has topped $8.7 trillion, serving as the core safeguard for tens of millions of American families' retirement lives.

Compared to mandatory government Social Security, the big difference with voluntary savings like IRAs and 401(k)s is investment autonomy: Both types of accounts enjoy deferred or tax-exempt treatment on investment gains, but IRAs have a wider investment range and can directly hold various assets (including crypto in some types); 401(k) investments have long been restricted, with most funds going into low-risk products packaged by asset managers chosen by employers (like mutual funds, bonds), not direct spot assets. Trump’s reform this time is exactly about lifting those limits on 401(k), creating the conditions for high-volatility assets like crypto to enter mainstream retirement portfolios.

2. From Strict Bans to Opening Up: A Shift in Regulatory Ideas and Market Realities

For a long time, US 401(k) plans have strictly kept out high-risk assets like crypto, mainly because the goal is to protect the safety and stability of retirement savings. High volatility naturally clashes with the aim of steady pension growth, and regulators worry that retail investors lack the risk tolerance and expertise—a sharp market swing could hit their retirement security hard. Plus, financial institutions face extra costs and risks in custody, valuation, and compliance, which has kept policies tight.

But Trump’s administration signing this executive order to ease restrictions isn’t some whim—it’s the result of multiple factors piling up: On one hand, in a world of low interest rates and high inflation, it's responding to folks’ need for higher-yield options and fulfilling campaign promises of “deregulation”; on the other, this represents a quid pro quo—the crypto industry backed Trump’s camp during the election, and his family holds diversified stakes across crypto ventures; deeper down, crypto isn’t just a niche experiment anymore, with institutional adoption, ETF approvals, and global compliance speeding up, it’s increasingly viewed as mainstream assets.

It’s worth noting this policy isn’t just for crypto but for broader “Alternative Assets,” officially defined to include private equity, real estate, commodities, and digital currencies. So, the policy’s intent is a comprehensive rollback of investment barriers, aimed at broadening individual investors’ portfolio options while accommodating societal appetite for yield-generating assets.

You could say this flip from “strict bans” to “opening up” shows a loosening in US regulatory thinking, while mirroring changes in capital market landscapes and political reshaping.

3. Far-Reaching Impacts: A Gamble That Might Just Kick Off

Bringing crypto and other Alternative Assets into 401(k) options means the US government is launching an unprecedented high-risk experiment in retirement systems. Once pensions flow into crypto markets at scale, it’ll boost liquidity and price stability hugely, and tie government interests tightly to crypto: With millions of Americans’ retirement savings linked to crypto assets, policymakers will have to think about keeping markets stable. This deep tie could speed up crypto’s compliance process, forcing regulators to roll out clearer, better rules, boosting the whole market’s maturity, transparency, and credibility to draw in more mainstream institutions and individuals.

At the same time, a deeper political angle is that these interest ties might give crypto-friendly policies staying power beyond party changes. It elevates protecting crypto from just Trump’s personal or partisan move to a “forced choice” for the government to safeguard citizens’ property—any steps weakening crypto could be seen by voters as “messing with retirement cheese,” sparking political backlash.

When your money’s on the chain, do they still dare say “no”? Image source: Created by the author

However, this gamble is full of worries. Crypto markets are famous for wild price swings, with cyclical bull-bear shifts often bringing big asset shrinks. More crucially, structural issues like fraud, money laundering, and illegal financing still lurk, some assets lack transparency, and trading platform security incidents happen now and then. If pension funds take a heavy hit in this setup, the losses won’t just be on paper—they’ll spark a trust crisis socially, shaking millions of American families’ future security, with political pressure quickly hitting the White House and Congress. Then, the government might have to step in with fiscal bailouts, creating a double bind between policy and markets.

In other words, this could push crypto into an era of institutionalization and full regulation, or backfire on policymakers if risks spiral, turning this “bold try” into a chapter that’s reflected on or even criticized in history.

4. Another Angle: The Fiscal Game Behind Tax Deferrals

For ages, US 401(k) plans have had two tax modes: Traditional takes “pre-tax contributions, taxed as ordinary income on retirement withdrawal,” while Roth is “after-tax contributions, tax-free on qualified withdrawals”—either way, both defer taxes on investment gains, which is their long-term appeal. So, adding crypto assets to 401(k) won’t change these basic tax rules, but it means these high-volatility assets are entering a compliant “shell” of deferred or exempt taxes for the first time, letting investors bet on cryptos long-term growth while enjoying tax perks.

Within this framework, the fiscal impact is more like a tax game across temporal horizons. For “traditional account” choosers, current taxable income drops, short-term government revenue dips, but future withdrawals get lumped into taxable income—it’s a classic “planting seeds for future harvests” strategy, trading today’s concessions for a bigger tax base decades later. If crypto succeeds long-term, retirement cash-outs could far exceed now, bringing the government higher taxes; but if markets slump or policies shift, short-term tax sacrifices might lead to long-term revenue voids. That’s the biggest risk and suspense in this move from a fiscal standpoint.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.