1. The Profit Margin Crisis in the Crypto Mining Industry

In November 2025, Marathon Digital Holdings (MARA) revealed a strategic shift in its third-quarter earnings report, announcing that the company "will sell a portion of newly mined Bitcoin henceforth to support operating capital needs". This move highlights the current reality of constantly shrinking profit margins faced by the crypto mining industry.

It's no isolated incident. Riot Platforms (RIOT), another mining giant, released its October 2025 production and operations update, showing that it mined 437 Bitcoin in that month, a 2% month-over-month decrease and a 14% year-over-year decrease. At the same time, it sold 400 Bitcoin. In April 2025, RIOT also sold 475 Bitcoin—the first time RIOT had sold self-mined Bitcoin since January 2024.

RIOT had long adhered to a "HODL" strategy, preferring to hold the majority of its Bitcoin in hopes of gaining from rising currency prices. However, in the new cycle following the block reward halving, RIOT has also begun adopting a more flexible capital strategy. The company’s CEO explained that these sales can reduce the need for equity financing, thereby limiting dilution for existing shareholders. This shows that even top mining companies that stick to a holding strategy must, when necessary, sell off a portion of their Bitcoin output to maintain healthy finances based on market and operational needs.

Based on coin price and hashrate data, mining profits are continuously being squeezed. By the end of 2025, the network hashrate climbed to a record high of 1.1 ZH/s. Simultaneously, the Bitcoin price dropped to around $81,000, and the hashprice fell below $35/PH/s. Meanwhile, the median hashcost (cost per hashrate) soared to $44.8/PH/s—this signifies intensified market competition and compressed profit margins, with even the most efficient mining companies barely reaching the break-even point.

As the marginal revenue from mining decreases, fixed electricity and financing costs remain stubbornly high. Against this backdrop, although some mining companies have rapidly pivoted to AI and High-Performance Computing (HPC), they still face varying degrees of capital strain and survival pressure. At this point, efficient tax planning is a crucial strategy for easing capital pressure and supporting long-term operations. Next, we will use the United States as an example to discuss whether tax planning can effectively lower the overall operating pressure on mining companies.

2. The Tax Burden on Crypto Mining Companies: Taking the US as an Example

2.1 Corporate Tax Framework

In the United States, companies can be structured as either Pass-through Entities or C Corporations. Under US tax law, Pass-through Entities distribute profits directly to the owners, who pay tax at their personal income tax rate at the individual level, achieving single-layer taxation. Conversely, C Corporations first pay tax at the company level at a flat 21% rate, and then shareholders pay tax on dividends at the individual level, resulting in double taxation.

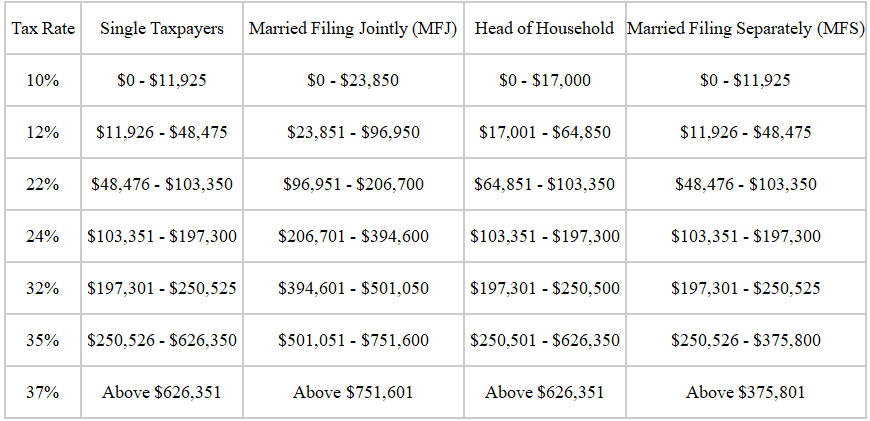

To elaborate, Sole Proprietorships, Partnerships, S Corporations and the majority of Limited Liability Companies (LLC) all belong to the category of Pass-through Entities. Their annual profits flow directly to the individual for tax settlement and are not subject to Federal corporate income tax. Income from Pass-through Entities is treated as individual ordinary income and declared at the ordinary income tax rate, which can be as high as 37% (see the figure).

Table 1: 2025 US Federal Ordinary Income Tax Rates and Brackets

As property, the taxable nature of crypto mining income and sale gains remains unchanged, but the actual tax burden may differ depending on the taxpayer entity.

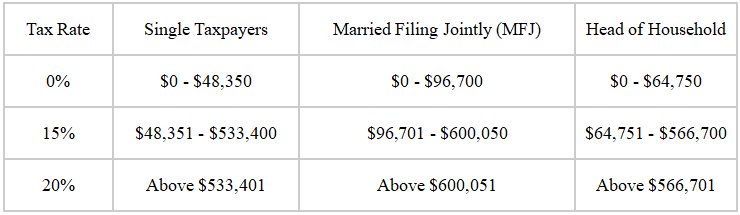

(1) If a crypto mining company is a Pass-through Entity, it is not required to pay Federal income tax. However, the company's shareholders must declare personal income tax on their share of the profits. The types of taxes involved for a Pass-through Entity in the acquisition and trading of cryptocurrency are ordinary income tax and capital gains tax. First, cryptocurrency obtained by the Pass-through Entity through mining, staking, airdrops, or other means require shareholders to declare and pay taxes as ordinary income at the individual level. Second, when the Pass-through Entity sells, exchanges, or spends cryptocurrency, it is subject to capital gains tax. If the holding period is less than or equal to one year, the gain is treated as short-term capital gain and taxed at the ordinary income tax rate, ranging from 10% to 37%. If the holding period is greater than one year, the gain is treated as long-term capital gain and enjoys preferential rates of 0%, 15%, or 20%, depending on the taxable income (see the figure).

Table 2: US Long-Term Capital Gains Tax Rates and Brackets

(2) If a crypto mining company is a C Corporation, it is subject to a flat 21% Federal corporate income tax, along with State taxes. Cryptocurrency obtained by a C Corporation through mining, staking, airdrops, or other means is included in the company's revenue at its fair market value. Capital gains (without distinction between long-term and short-term) from selling, exchanging, or spending cryptocurrency are also included in the company's revenue. The company's profit, calculated after deducting costs and relevant expenses, will be taxed at the 21% Federal corporate income tax rate, and State taxes will be simultaneously paid according to each state's standards. If a C Corporation chooses to pay dividends to shareholders, it triggers a second layer of taxation at the dividend level, resulting in double taxation.

2.2 The Challenge of Multiple Tax Burdens

Within the US jurisdiction, large, publicly funded, or companies preparing for listing, such as MARA, RIOT, and Core Scientific, almost universally operate as C Corporations. Smaller or startup mining companies, however, tend to favor Pass-through Entity structures.

The choice of corporate structure is driven by differences in financing needs, cash retention strategies, and tax considerations. The crypto mining industry is capital-intensive, with a strong demand for retained earnings during expansion periods. The C Corporation structure is conducive to retaining profits, does not immediately pass the tax burden to owners, and reduces the cash outflow pressure caused by owners paying tax on undistributed profits. The LLC structure offers early tax flexibility (it can choose to be taxed as a Partnership or an S Corporation to reduce the tax burden) and can choose to reorganize as a C Corporation after reaching a certain scale. Therefore, many startup mining companies use the LLC structure early on, gradually transitioning to a C Corporation as their scale and financing needs grow.

Even with different company structures, crypto mining companies face multiple tax burdens. For Pass-through Entities, business income "passes through" to the owners, so miners acquiring a token are immediately deemed to have obtained taxable income, and subsequent appreciation from disposing of the token must be declared again. Owners must continuously bear the tax burden at both stages. In contrast, a C Corporation records mining or related business income on its books, and the enterprise calculates profits and pays corporate income tax centrally. If the enterprise distributes profits to shareholders, it triggers tax again at the dividend level. Nevertheless, through appropriate tax planning, mining companies can legally and reasonably reduce their taxes, turning the existing tax burden into a competitive advantage for the enterprise amidst compressed mining profits.

3. Possibilities for Crypto Mining Company Tax Optimization

Using the US as an example again, crypto mining companies can plan various tax optimization paths to achieve tax savings.

3.1 Utilizing Miner Depreciation to Optimize Current Tax Burden

The United States introduced the One Big Beautiful Bill Act this year, which restored the 100% bonus depreciation policy stipulated in Internal Revenue Code (IRC) Section 168(k). The "bonus depreciation" policy provided by IRC §168(k) allows taxpayers to deduct the entire cost of newly purchased fixed assets such as mining machines or servers in the year of purchase, thereby reducing taxable income. This preferential depreciation rate was originally set at 100% between 2018 and 2022, but was planned to be gradually reduced starting in 2023, reaching 0% in 2027. The One Big Beautiful Bill Act aims to restore and extend this benefit, stipulating that eligible property purchased and placed in service after January 19, 2025, and before January 1, 2030, will have the 100% bonus depreciation restored. Simultaneously, the One Big Beautiful Bill Act also increased the depreciation limit for IRC Section 179, raising the cap on equipment expenses that can be fully deducted immediately from $1 million to $2.5 million.

This is extremely significant for mining companies. Fixed assets such as purchased mining machines, power infrastructure, and cooling systems can be expensed in the first year, directly lowering the current year's taxable income and significantly boosting current cash flow. Besides saving on taxes, the "bonus depreciation" method is also beneficial for increasing the present value of funds.

It should be noted that when using the bonus depreciation method, one still needs to consider the current year's cost situation to avoid profit loss and subsequent loss carryforwards. For instance, a US mining company earned $400,000 in income and spent $500,000 to purchase mining machines in 2024. If the company immediately deducts the $500,000 cost in that year, due to its low income, it will result in a book loss of $100,000 (Net Operating Loss, NOL) after the deduction. Although the current period’s profit is negative, and no income tax is due, this also means that the enterprise cannot extract or distribute profits even if cash flow still exists on the books. For tax treatment, NOL carried forward to the next year can only offset 80% of the current year's taxable income. Therefore, blindly using bonus depreciation in low-profit years may not be a wise decision.

3.2 Structuring the Cross-Border Architecture and Plan Capital Gains Rationally

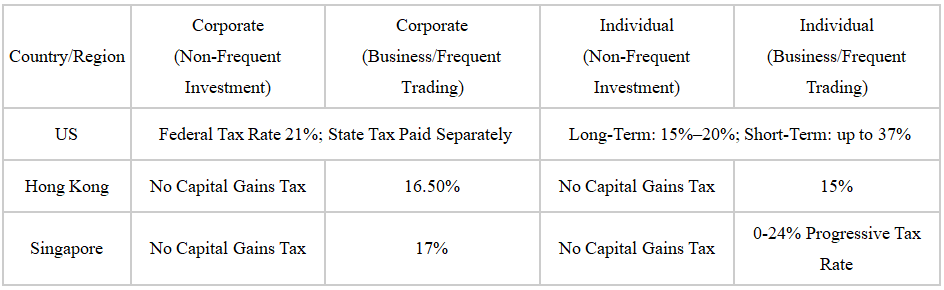

Crypto currency tax policies differ across various jurisdictions. In the United States, as long as a taxable transaction occurs and a profit is made, tax declaration and payment are required, regardless of whether it's an occasional sale for cash, frequent trading, or a business operation. This "tax-on-every-gain" tax system treats all equally and puts significant tax pressure on US-based crypto miners. In contrast, the crypto tax policies in Singapore and Hong Kong are more friendly. Currently, both regions do not tax crypto capital gains obtained by individuals or businesses from non-frequent investments. As long as the related transaction is classified as non-frequent investment income, investors do not have to pay tax on the appreciated portion of the assets, realizing a zero-tax dividend for long-term holding. Naturally, those engaged in frequent trading or business activities still need to pay corporate or personal income tax on their profits. Singapore's corporate income tax is about 17%, and Hong Kong's corporate tax rate is 16.5%. Although frequent traders still need to pay tax, the rates in Hong Kong and Singapore are clearly more competitive compared to the Federal corporate tax of 21% in the US.

Table 3: US, Hong Kong, and Singapore Tax Rate Comparison

Based on the differences in tax systems across jurisdictions, US crypto mining companies can legitimately reduce their crypto tax burden by structuring a cross-border architecture. Take a US Bitcoin mining farm company as an example: it can establish a subsidiary in Singapore, first selling the regularly mined Bitcoin to this affiliated subsidiary at the market fair price. The subsidiary then sells the Bitcoin to the global market. Through this "internal first, external second" transaction arrangement, the US parent company only needs to pay corporate income tax on the initial mining income. The appreciated profit of the Bitcoin held by the Singapore subsidiary may, under certain conditions, be eligible for Singapore's capital gains tax exemption policy, thereby avoiding capital gains tax. The tax-saving effect of this cross-border architecture design is clear, with its core being the legal transfer of the crypto asset appreciation stage from a high-tax zone to a tax-exempt or low-tax zone to achieve the maximization of retained earnings.

3.3 Using a Mining Rig Custody-Leasing Structure to Plan the Economic Substance and Tax Burden

The mining rig custody-leasing structure is widespread in the crypto mining industry. Its business logic is to separate asset ownership from mining operations, enhancing the efficiency of capital and resource allocation. This model naturally leads to a profit distribution, where different entities recognize income based on their role in the transaction. For instance, an overseas entity located in a low-tax jurisdiction handles the purchase, ownership, and external leasing of mining rigs, while the local US entity focuses on mining operations and pays rent or custody fees to the overseas entity. In this scenario, the equipment income generated by the low-tax jurisdiction entity has the opportunity to be subject to a lower tax rate. Although the mining rig custody-leasing structure itself wasn't created for tax purposes, it has a genuine commercial background. This provides a certain scope for implementing cross-border tax planning.

Of course, using this structure within the same entity must also meet certain compliance prerequisites. For example, the overseas leasing entity must have economic substance and genuinely hold the mining rig assets. The rent must be priced according to the arm's length principle, meaning the rent is at a reasonable market level, etc.. Only when these conditions are met can the related transactions be considered genuine business arrangements and not tax avoidance.

4. Summary

Mining profits continue to decline due to multiple factors, and the global crypto mining industry is quietly entering a new industry cycle. At this turning point, tax planning is no longer just an optional financial tool; it has the potential to become the key solution for mining companies to maintain capital health and boost their competitiveness. Mining companies can conduct systematic tax planning by integrating their business characteristics, profit structure, and capital investment, all while ensuring that various arrangements comply with regulatory and tax law requirements. This converts the tax burden into a competitive advantage, laying the foundation for long-term stable development.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.