News Overview

On January 15, 2026, multiple media outlets reported that the look-back period for back taxes on overseas income for mainland Chinese tax residents has been extended, reaching as far back as 2020 or even 2017. Since 2025, many tax residents have received prompts and notices from tax authorities, requiring them to self-examine their domestic and global income and file tax returns in a timely manner. The scope of these back-tax requests mainly focuses on the last 3 years, specifically 2022 and 2023.

On January 16, relevant departments of the State Taxation Administration (STA) stated that tax authorities will continue to strengthen publicity and guidance regarding personal income tax on overseas income. Since last year, they have been reminding taxpayers to conduct self-inspections on income obtained from overseas between 2022 and 2024.

FinTax Commentary

1. Interpreting the Event: Overseas Income Back Taxes Backdated to 2017

1.1 Event Details and Background

Recently, a report from a well-known media outlet regarding "backdating tax on overseas income" has gone viral across various financial platforms, sparking heated discussions. The report points out that the look-back period for back taxes on overseas income for mainland Chinese tax residents has been extended compared to before, reaching back to 2020 or even 2017. The day after this report was published, relevant departments of the State Taxation Administration revealed that since last year, they have been reminding taxpayers to self-examine income obtained from overseas between 2022 and 2024. This means that a large number of Chinese tax residents holding overseas income accounts—such as those trading US stocks, investing in offshore funds, or setting up offshore trusts—will likely face "retroactive" tax audits for under-reported overseas income from previous years and be required to pay back taxes and late payment surcharges.

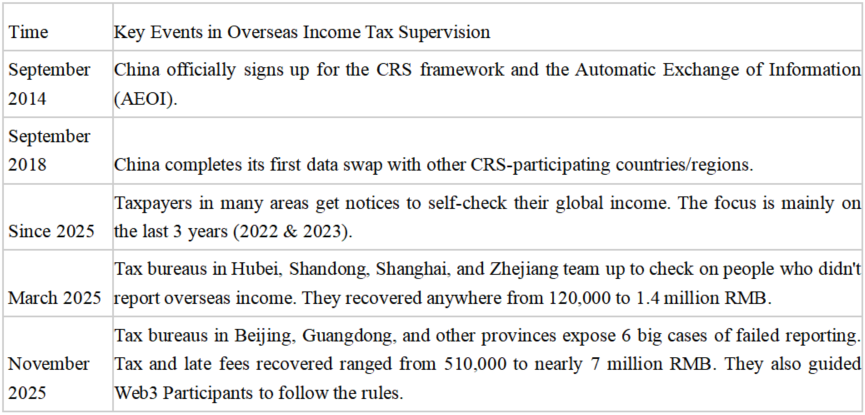

This retroactive tax event is happening against the backdrop of China implementing the CRS system and tax authorities launching a series of tax administration actions for overseas income (as shown in the table below). From the objective logic of tax supervision, the prerequisite for tax authorities to achieve precise audits is mastering tax-related information. China conducted its first CRS information exchange in 2018, which exchanged account information from 2017. Consequently, Chinese tax authorities gained access to account balances, transaction records, and holder details in overseas banks, securities, and trusts under the CRS exchange framework. This makes it possible for tax audits on overseas income to trace back to 2017.

Table 1: Review of Key Events in Overseas Income Tax Supervision

1.2 Observation of Supervision Trends

Reviewing the series of enforcement actions by tax authorities since 2025, it is clear that undeclared overseas income has become a focus of supervision. Analyzing this event and related enforcement actions reveals the following trends:

l Extension of the look-back period: The range for backdating taxes on overseas income has expanded further, covering historical tax data across multiple years, reaching as far back as 2017. Any overseas income that was not fully declared in the past may be included in the scope of inspection.

l Batch identification and upgraded methods: Relying on CRS information exchange and tax big data analysis, tax authorities now have the ability to perform batch identification and precise positioning of overseas income. Combined with the "five-step work method," the supervision model is shifting from "relying on voluntary disclosure" to "substantive inspection and accountability."

l Expanded enforcement scope and increased intensity: Taxpayers in multiple regions have received SMS and phone prompts from tax authorities. The targets of supervision are no longer limited to specific high-risk groups but cover a wide range of people across different income levels and types of overseas earnings.

2. Why is Backdating Taxes Possible? Legal, Information, and Technical Factors

As long as the conditions prescribed by law are met, tax authorities have the right to enforce the law whether tracing back three years, to 2017, or even earlier. A triple-threat of factors—legal, informational, and technical—provides the practical conditions for tax authorities to carry out retroactive tax collection:

First, the legal basis is sufficient and the look-back period is clear. China implements the principle of global taxation for tax residents. Individuals who have a domicile in China or meet the 183-day residency standard are identified as "Chinese tax residents" and must declare and pay personal income tax on their worldwide income. This is based on existing provisions of the Personal Income Tax Law and related regulations, not a new obligation. Taxable overseas income includes global income derived outside China, such as comprehensive income (wages and salaries, remuneration for labor services, author's remuneration, and royalties), business income, and other income (interest, dividends, bonuses, income from transfer of property, income from leasing of property, and incidental income). The classification standards are basically consistent with domestic income.

Furthermore, the law clearly stipulates legal responsibilities for tax violations and the look-back period for recovering taxes and late payment surcharges. Legal responsibilities include recovery of taxes, late payment surcharges, administrative penalties, and criminal penalties. The look-back period is defined in Article 52 of the Law on the Administration of Tax Collection: if a taxpayer or withholding agent fails to pay or underpays taxes, the tax authorities have the right to recover the unpaid taxes and surcharges within 3 years; in special circumstances, the period can be extended to 5 years. If tax evasion, tax refusal, or tax fraud is involved, the tax authorities are not subject to the aforementioned time limits when recovering unpaid or underpaid taxes and surcharges.

Second, the implementation of the CRS system has broken down cross-border information barriers. China officially completed the domestic legislative process for CRS in 2017 and conducted its first automatic exchange of financial account information with other CRS participating jurisdictions in September 2018. This covers core data such as account balances and investment returns from major countries like the UK, France, Germany, Switzerland, and Singapore, as well as traditional tax havens like the Cayman Islands, the British Virgin Islands (BVI), and Bermuda. The accumulation and integration of historical exchange data have changed the situation of cross-border tax information asymmetry, providing an information foundation for tax authorities to conduct risk assessments and substantive inspections of overseas income from earlier years.

Finally, the implementation of "Tax Governance through Data" has improved tax administration efficiency. The deep application of "Golden Tax Phase IV" and the comprehensive support of tax big data have achieved the intelligent integration and analysis of cross-departmental and cross-year global capital flow data. By identifying tax risk points through big data models, tax authorities now possess the ability to conduct batch screening and precise positioning of overseas income. Meanwhile, combined with the "five-step work method" (prompting and reminding, urging rectification, warning interviews, case filing for inspection, and public exposure), tax enforcement is gradually turning toward active substantive inspections. The continuous upgrade of enforcement technology provides the technical support for carrying out retroactive audits.

3. Turning a Crisis into an Opportunity: A Compliance Guide for Taxpayers

Taxpayers with overseas income and related tax risks can refer to the following measures to review their tax situation and deal with compliance challenges:

First, carry out self-inspections of income and assets to assess tax impact. Systematically review bank accounts, securities accounts, insurance products, trust interests, and fund shares held overseas since 2017 (especially from 2022 to 2024). Organize various types of income obtained in the corresponding years, such as dividends, labor remuneration, and gains from asset transfers. Compare these with previous Personal Income Tax annual settlement records to confirm if there are any undeclared or under-declared situations. Based on the results, assess the amount of tax, fines, or late payment surcharges (if applicable) and make appropriate responses to the potential personal tax impact.

Second, take proactive remedial actions to lower compliance costs. The actual cost of undeclared overseas income is not just the tax itself, but also the late payment surcharges (calculated daily) and administrative fines. The timing of handling the issue has a material impact on legal consequences. For individuals with historical filing flaws, it is crucial to seize the window for self-inspection and complete the declaration promptly, paying back taxes and surcharges to avoid the continuous accumulation of costs. If you have already received risk prompts via SMS or phone calls from tax authorities, you may be in the "prompting and reminding" stage of the "five-step work method." Actively cooperating with corrective filings may help secure more lenient treatment.

Third, seek support from professional advisors. Tax issues regarding overseas income involve a complex mix of domestic and international regulations, tax treaties, and the determination of the nature of income. Taxpayers can seek help from professional financial advisors in a timely manner to improve their response capabilities and prevent legal risks.

The FinTax team can provide customized tax planning and consulting services at different stages:

l Stage 1: No inspection notice has been received from the competent tax authority. In light of current personal income tax management policies and national risk control requirements for overseas income, we assist clients in sorting out domestic and overseas income and preparing for potential future risk control responses.

l Stage 2: An inspection notice has already been received from the competent tax authority. We assist clients in sorting out overseas income data for the relevant years as required by the tax notice and prepare explanations based on the type of income. We help clients communicate with tax inspectors to ensure compliance throughout the inspection process, complete the personal income tax response for overseas income, and provide optimization suggestions for future overseas tax business and domestic/overseas tax arrangements.

4. Summary

Since China began participating in CRS information exchange, the ability of tax authorities to monitor overseas financial accounts and investment returns has continuously improved, making the tax risks associated with personal overseas income more prominent. In this new era of high tax transparency, it is difficult for taxpayers to rely on "supervision blind spots." Only by establishing a comprehensive sense of compliance and evaluating their overseas income structure and its tax impact in China as early as possible can they effectively deal with the challenges of upgraded supervision and achieve steady and secure asset growth.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.