Recently, the Inland Revenue Department (IRD) of the Hong Kong Special Administrative Region (Hong Kong / HK) updated its Frequently Asked Questions (FAQs). These updates focus on individuals who might be considered residents of both the Mainland and Hong Kong at the same time. The IRD explains how to use the "Tie-breaker Rule" under the the Arrangement between the Mainland of China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income(Comprehensive Arrangement) to determine which side a person belongs to for tax purposes.

As economic ties between the two places grow closer, working across the border and living in both cities has become a way of life. Many people now follow a "work in Hong Kong, live in the Mainland" routine. When someone meets the residency criteria for both places simultaneously, the Tie-breaker Rule plays a vital role in deciding which tax system applies.

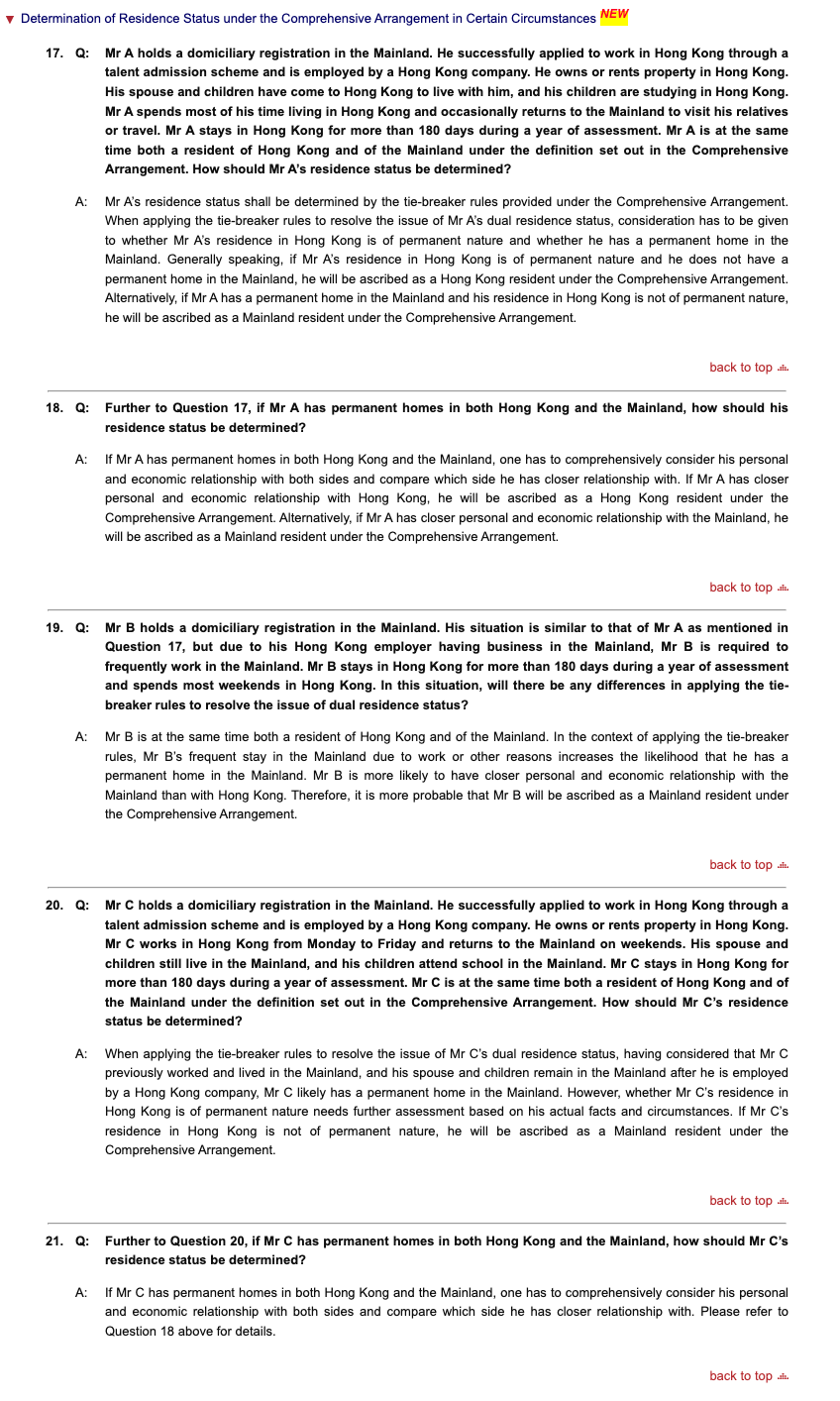

Original link: https://www.ird.gov.hk/eng/faq/dta_2006.htm

On the Mainland side:

A Mainland tax resident is an individual who has a residence in China, or an individual who does not have a residence but has stayed in China for a cumulative total of 183 days within a tax year. Here, "residence" is defined as a place where one habitually resides due to household registration (hukou), family, or economic interests. In practice, the Mainland uses "habitual residence" as the core standard. Keeping a domiciliary registration often leads to a presumption of habitual residence, resulting in being identified as a Mainland tax resident.

On the Hong Kong side:

A Hong Kong tax resident is an individual who ordinarily resides in Hong Kong, or stays in Hong Kong for more than 180 days during a relevant year of assessment, or for more than 300 days in two consecutive years of assessment. Compared to the Mainland, Hong Kong's identification of tax residents focuses more on the actual state of residence and the closeness of economic ties, rather than legal permanent residency status or household registration.

Because of these objective differences in residency rules and tax year calculations, cross-border workers might meet the standards for both places at once, facing tax conflicts due to dual residency. On August 21, 2006, the Mainland and Hong Kong officially signed the "Comprehensive Arrangement" to avoid double taxation and prevent tax evasion. Since then, several protocols have been signed to update the content, keeping up with international tax rules and promoting economic and investment exchange between the two regions.

To resolve conflicts in tax jurisdiction, the "Comprehensive Arrangement" introduced the Tie-breaker Rule. This rule is widely used in international tax circles to solve dual residency conflicts caused by legal differences between tax jurisdictions.

According to the Tie-breaker Rule under the "Comprehensive Arrangement," the tax status of an individual who meets the residency criteria for both the Mainland and Hong Kong is determined in the following order:

1. which side he has a permanent home;

2. which side he has a closer personal and economic relationship;

3. which side he has a habitual abode;

4. If all else fails, the competent authorities of both sides will resolve the matter through mutual agreement to decide which side the person belongs to.

It is important to note that these standards are ranked by priority. The next standard is only used if the previous one cannot solve the issue.

The real value of this FAQ update lies in its use of realistic cases (Q17-Q21). It shows how to determine tax residency under common scenarios like "talent schemes" and "dual-city lifestyle" based on the Tie-breaker Rule.

For various scenarios, the Hong Kong IRD does not provide an absolute "yes or no" answer for tax residency. Instead, it lists factors to consider when making a judgment, including: the individual's domiciliary registration; where core family members like spouses and children live, work, and study; business shares held; and where salary is paid and social security is contributed. These factors are strong evidence of a "center of vital interests."

Therefore, single elements like having a domiciliary registration or staying in Hong Kong for more than 180 days in a tax year are not the only deciding factors under the Tie-breaker Rule. Under the "Comprehensive Arrangement," a person may still be seen as a Hong Kong resident. This doesn't mean core standards like "days of stay" aren't important; rather, the Tie-breaker Rule allows for a combined judgment based on many factors.

Overall, this FAQ update from the Hong Kong IRD isn't a major change to the system. Instead, it serves as a practical guide—further clarifying the rules for determining tax residency for high-frequency cross-border groups. As tax oversight improves and information becomes more transparent, tax authorities in both places will be more accurate in judging the center of an individual's economic interests. Cross-border tax management is moving toward a more refined and precise era.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.