Chile is one of the most economically stable and financially mature countries in Latin America, and it plays a significant role in the current crypto market. Although its overall transaction volume doesn't quite match that of regions like Brazil and Argentina, the market activity is still remarkable. According to the latest industry reports, Chile's annual cryptocurrency transaction volume for 2024 is approximately $2.38 billion, placing it at the forefront in Latin America. In terms of user adoption, Chile's performance is equally outstanding, with a cryptocurrency ownership rate of about 13.4%, ranking highly on a global scale.

It is worth noting that as the Chilean crypto market becomes increasingly active, Chile's financial regulatory authorities are also following the trend, viewing crypto assets as a vital component for driving financial innovation. On January 4, 2023, Chile's FinTech Law (Law No. 21,521) was officially published in the Official Gazette, regarded as one of the most important reforms in Chile's capital market in the last decade. The law aims to promote competition and inclusion in the financial system through technological innovation, establishing clear regulatory boundaries for previously unregulated fintech services, including crowdfunding platforms, alternative transaction systems, credit, investment advice, and custody of financial instruments. Subsequently, on January 12, 2024, General Rule No. 502 (NCG 502) further clarified the registration, authorization, corporate governance, risk management, capital, and collateral requirements for financial service projects (including platforms that actually handle crypto assets). Regarding crypto assets, although Chilean authorities currently maintain a prudent regulatory attitude—believing that virtual currencies possess neither legal tender status nor foreign currency status—because they recognize crypto assets as "intangible assets," the Financial Market Commission (Comisión para el Mercado Financiero, CMF) has included them in service categories such as "custody of financial instruments" within the FinTech Law (Law No. 21,521, 2023), thereby providing stable and predictable behavioral guidelines for market participants.

Clearly, with the continuous expansion of the Chilean crypto market and constant regulatory updates, it is necessary to systematically understand the latest systems for Chilean crypto assets, and to get to know the tax compliance framework of the Internal Revenue Service (Servicio de Impuestos Internos, SII), as well as the latest regulatory system implemented by the CMF based on the FinTech Law.

1 The Basics of Chile's Tax System

The SII implements tax supervision on income from crypto asset transactions based on current regulations such as the Income Tax Law (Ley sobre Impuesto a la Renta) and the Sales and Services Tax Law (Ley sobre Impuesto a las Ventas y Servicios). Chile's tax system is dominated by three core tax categories: First Category Tax (Impuesto de Primera Categoría, Corporate Income Tax), Global Complementary Tax / Additional Tax (Impuesto Global Complementario / Impuesto Adicional, Resident/Non-Resident Personal Income Tax), and Value Added Tax (Impuesto al Valor Agregado, IVA).

1.1 First Category Tax (Corporate Income Tax)

The First Category Tax is the core component of Chile's corporate income tax system, mainly applicable to corporate entities engaged in industrial, commercial, mining, agricultural, financial, and other economic activities in Chile. This tax was originally established by the Income Tax Law (Ley sobre Impuesto a la Renta, Decree Law No. 824) and uses an Accrual Basis for taxation, meaning taxable income is recognized in the accounting period when revenue is realized or expenses occur. It is important to note that Chilean companies defined in this law principally include both local companies and foreign companies with permanent establishments in Chile, both of which must pay corporate income tax.

The standard corporate income tax rate is 27%. This rate applies to most general businesses, especially large or multinational corporations. However, to support economic recovery and the sustainable development of small and medium-sized enterprises (SMEs), the Ministry of Finance (Ministerio de Hacienda, MH) has introduced temporary tax incentive measures starting from the 2025 fiscal year. According to the Law on Simplifying Regulations and Promoting Economic Activity (Law No. 21,755), legal entities that meet the criteria for Chilean SMEs will have their income tax rate temporarily reduced to 12.5% for the 2025, 2026, and 2027 fiscal years; it will only return to 15% in the 2028 fiscal year.

1.2 Global Complementary Tax / Additional Tax (Resident / Non-Resident Personal Income Tax)

Chile's personal income tax system consists of two complementary taxes: the Global Complementary Tax and the Additional Tax. The former applies to tax residents (natural persons residing in Chile for more than 183 days or having their center of vital interests there), taxing their global income; the latter applies to non-resident individuals, taxing only their income derived from within Chile.

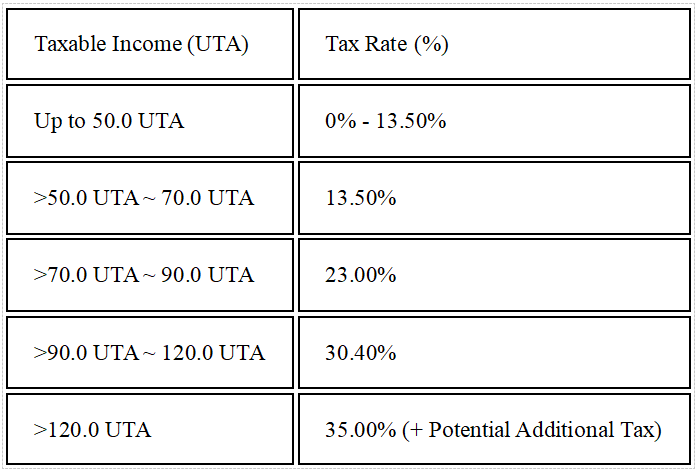

The Global Complementary Tax implements a progressive tax rate system, with rates ranging between 0% and 40%. The specific tax brackets are determined based on the Annual Tax Unit (Unidad Tributaria Anual, UTA). The SII adjusts the UTA value annually based on inflation and exchange rate factors. The personal income tax brackets for the 2025 year are as follows:

1.3 Value Added Tax (VAT)

Chile's Value Added Tax (IVA) was established by the Sales and Services Tax Law (Decree Law No. 825, 1974) and is managed and collected by the tax bureau, with a standard rate of 19%. IVA applies to domestic sales of goods, provision of services, and import activities. Taxpayers must register before providing taxable transactions, and there is no minimum turnover threshold. The system uses a deduction mechanism of output tax minus input tax to avoid double taxation, and filing and payment are usually done on a monthly basis.

According to Chile's Sales and Services Tax Law, the scope of VAT includes: first, sales activities transferring movable property or part of immovable property for consideration; second, various services provided for remuneration; and third, goods imported into Chile. This means that whether it is a domestic transaction or cross-border import, as long as it meets the above conditions, VAT must be paid. Exported goods and specific services (education, medical, financial) enjoy a zero tax rate or exemption, while low-value imports, used car sales, and international transport are subject to simplified collection systems.

It is worth noting that since 2020, non-resident digital service providers offering online services to Chilean consumers are also required to register and pay IVA. Whether this also applies to IVA in this context will be discussed in the next section.

2 How Crypto Assets are Taxed

Through multiple administrative rulings and FAQs, the SII has positioned crypto assets as intangible/digital assets, explicitly stating that they are neither legal tender nor foreign currency. At the same time, it includes the gains generated from them within the scope of general income taxation under the Income Tax Law (i.e., listed as "other general income" shown in Art. 20 N°5). This determination dictates the application of the three types of taxes, including First Category Tax (Corporate Income Tax), Global Complementary Tax or Additional Tax, and VAT, all of which should be based on this intangible asset positioning.

2.1 First Category Tax

The SII has clarified that the "increased value/capital gain" (mayor valor) generated from buying and selling crypto assets should be classified as general income under Article 20, Section 5 of the Income Tax Law, thereby affecting the calculation of First Category Tax (for corporations) and final personal taxes (IGC/IA). Corporations include operating gains confirmed by accounting or tax systems into their taxable profits; individuals apply the corresponding final tax burden based on their tax resident/non-resident status.

2.1.1 Selling / Transferring (Including "Crypto-to-Crypto", Buying Goods / Services with Crypto)

Selling (i.e., exchanging for fiat currency): The sale consideration is confirmed at the time of sale (calculated at the fair value in Chilean Pesos on the day of sale), and taxable income = sale consideration - purchase cost. In this regard, the SII requires transfer vouchers or invoices and other documents to prove the existence of costs and transaction records.

Crypto-to-Crypto Swaps / Exchanging Crypto for Goods or Services (Treated as Barter/Transfer): The official Q&A has not made a specific explanation regarding this. However, the SII treats the disposal of general crypto assets as a transfer (enajenación) event, and the income gain should be calculated based on the transaction consideration of that day, used for declaring and paying income tax. Therefore, some scholars believe that this principle applies not only to selling cryptocurrency for fiat currency but can also be extended to crypto-to-crypto swaps or using cryptocurrency to pay for goods or services—meaning any outflow of crypto assets could trigger capital gains taxation.

2.1.2 Mining / Staking / Airdrops

Mining: Mining income should be confirmed as the asset's book value at the market price on the day of "acquisition." Direct expenses incurred from mining (such as electricity, hardware depreciation, etc.) can be deducted or calculated as costs at the corporate/individual level (depending on whether it is a business activity) according to relevant rules.

Staking / Airdrops: The SII has not been explicit. Some scholars believe that tokens obtained for free through staking or airdrops can have an acquisition cost recorded as zero; subsequently, when sold, the taxable income is calculated as the sale consideration minus this (zero) cost. If obtained as a corporate business activity, it should be handled separately according to accounting and tax rules.

2.1.3 Transaction Fees / Brokerage Commissions

The SII has determined that when determining taxable income, commissions charged by brokers/exchanges can generally be listed as "necessary expenses to generate such income" in the current period (i.e., treated as operating expenses or deductible expenses), but transaction fees cannot be directly capitalized into the asset cost (i.e., fees are not items constituting the "tax cost" of the crypto asset, but are treated as expenses). This specifically depends on the accounting and tax rules applicable to the taxpayer.

2.2 Global Complementary Tax / Additional Tax

For resident individuals, income from crypto asset transactions is usually included in the annual comprehensive income and levied by the Global Complementary Tax at progressive rates. The SII points out that if the crypto asset transaction belongs to a natural person and is obtained non-commercially, the income should be calculated according to general income tax rules, including the difference between the transfer price and the purchase cost.

For non-resident taxpayers, crypto asset transaction income occurring in Chile or derived from Chile applies to the Additional Tax in principle, but no specialized ruling explicitly clarifying the detailed taxation method has been seen in public literature yet. Therefore, in actual operation, relevant income for non-residents should still be presumed to likely be subject to Additional Tax based on the tax law framework.

2.3 Value Added Tax (VAT)

According to SII rulings, due to the lack of physical substance, the buying and selling of crypto assets does not fall within the scope of taxation on the sale of tangible goods under the Sales and Services Tax Law, so it generally does not apply to the 19% IVA.

At the same time, regarding intermediary services or commission charges provided by exchanges or platforms, the SII pointed out in FAQs that these services "may be subject to IVA taxation" and require corresponding invoices or vouchers to be issued.

3 Chile's Crypto Regulatory Structure and Future Trends

To more comprehensively understand the position of tax policy within Chile's crypto asset regulatory system, this section will review the formation and evolution of the regulatory framework from an institutional perspective, focusing on analyzing its basic architecture, main rules, and latest revision dynamics.

3.1 Early Regulatory Setup

The period between 2018 and 2020 was the early stage where Chilean regulatory authorities gradually explored a regulatory framework for crypto assets. The regulatory characteristics of this period were generally quite preliminary, mainly concentrating on the legal characterization of crypto assets and tax treatment guidelines.

In 2018, the SII made its first authoritative response to the tax characterization of crypto assets via Ordinary Letter No. 963 (2018), deeming that gains obtained through buying and selling crypto assets belong to general income listed in the Income Tax Law (Art. 20 Nº5), and based on this, clarified the income tax application framework (distinction between individuals/corporations, etc.). This ruling laid the foundation for subsequent tax practices (such as cost confirmation, treatment of frequent traders).

Subsequently, in 2020, the SII further proposed more detailed administrative guidance on cost calculation methods, fee deductions, and high-frequency trading scenarios through Ordinary Letter No. 1474 (2020), responding to a large number of daily trading and tax filing practice issues in the market (such as accounting confirmation and cost methods).

3.2 Current Regulatory Framework

As mentioned above, Chile's systematic regulation of crypto assets began with the 2023 FinTech Law, so the current regulatory framework of Chilean authorities regarding crypto assets also unfolds based on the provisions of this law.

At the regulatory execution level, the CMF takes the lead, responsible for formulating general rules and implementing registration and authorization procedures for the financial service categories listed in the FinTech Law (such as alternative transaction systems, custody of financial instruments, intermediation of financial instruments, etc.). The General Rule No. 502 published by the CMF details the registration, authorization, governance, risk management, and capital requirements for financial service providers (Financial Service Providers / Virtual Asset Service Providers), thereby transforming the abstract requirements of the FinTech Law into enforceable compliance thresholds. Concurrently, the 2024 Tax Compliance Law (Law No. 21,713) strengthened the SII's powers in valuation, data acquisition, and anti-avoidance, emphasizing the ability to review complex transactions and non-market pricing, which consequently indirectly increased the tax compliance risk of crypto asset-related transactions.

The Central Bank of Chile (Banco Central de Chile, BCCh) has exclusive functions in monetary policy, payment systems, and determining legal tender status, and carries out policy coordination and research with the CMF on issues such as "payment-type digital assets" (e.g., stablecoins or retail Central Bank Digital Currencies). The division of labor between the BCCh and CMF is manifested as follows: the CMF focuses on regulatory compliance in capital markets and financial services; the BCCh focuses on publicly circulating means of payment and financial stability risks. Both maintain policy collaboration on overlapping issues.

Taxation and Anti-Money Laundering (AML) / Counter-Terrorism Financing (CTF) and cross-border intelligence tasks are undertaken by the SII and Chile's Financial Analysis Unit (Unidad de Análisis Financiero, UAF). The SII provides guidance on the tax characterization and practical treatment of crypto assets (such as treating crypto assets as intangible assets, income tax treatment of transfer events, and tax treatment of transaction fees) through a series of official documents and Q&As, while the UAF is responsible for suspicious transaction reporting and inter-agency coordination related to AML/CTF and cross-border intelligence.

Overall, under the macro guidance of the FinTech Law, Chile's regulatory framework presents a governance structure of "three powers collaborating, each performing its own functions": (1) CMF is responsible for market entry, governance, and ongoing supervision; (2) BCCh handles currency/payment stability issues; (3) SII and UAF are responsible for tax and anti-money laundering compliance respectively. This multi-agency collaborative governance model aims to strike a balance between encouraging financial innovation and ensuring market integrity.

3.3 Key Current Rules

Chile places the core rules for regulating fintech and crypto-related services under the FinTech Law and the General Rule No. 502 formulated by the CMF thereunder: the former defines the regulated financial service categories and regulatory objectives, while the latter puts registration, authorization, governance, and ongoing compliance requirements into practice. Summarized specifically, the rules can be divided into four categories.

The first and most significant compliance threshold is registration and market entry. Anyone providing financial services designated by the FinTech Law (including alternative transaction systems, custody of financial instruments, and intermediation of financial instruments, etc.) must register with the CMF and obtain authorization; registration applications must submit documents on corporate governance, management team qualifications, business models, capital structure, and risk management. Foreign entities can apply to enter if they meet the conditions. This system aims to bring over-the-counter or unregulated activities into the regulatory scope, increasing market transparency from the source.

The second category of requirements focuses on corporate governance, capital, and operational capabilities. General Rule No. 502 sets clear standards for governance independence, segregation of client assets, business continuity plans, and minimum capital or collateral, and requires the submission of an opinion report on operational capabilities from a third party as review material. Regulation focuses on reducing systemic risks generated by custody and entrustment services through these requirements, while setting a systemic bottom line for investor protection.

The third category of rules is AML/CTF and information disclosure obligations. Chile's UAF has clear requirements for suspicious transaction reporting, customer due diligence, and real-name registration. Virtual Asset Service Providers and other regulated financial service providers must execute transaction monitoring and report suspicious activities according to UAF and CMF standards; meanwhile, the SII's tax guidelines require keeping complete transaction records and valuation vouchers to facilitate tax compliance inspections.

Finally, regulation also emphasizes continuous supervision and enforcement consequences. The CMF maintains the deterrent power of the rules through routine reviews, information requests, and administrative sanctions on non-compliant parties (including fines and revocation of registration); at the same time, the 2024 tax reform enhanced the SII's investigation authority in valuation and anti-avoidance, meaning that in the cross-over areas of tax and regulation (such as large OTC transfers by related parties), there will be stricter compliance and audit risks. In this regard, companies need to treat compliance governance, valuation methods, and tax due diligence as equally important tasks.

3.4 Latest Revisions and Future Focus Areas

Since 2024, the pace of regulatory revisions has noticeably accelerated. In December 2024, the CMF revised General Rule No. 502, detailing the registration and authorization procedures, as well as the supporting materials required for application, thereby improving the efficiency of the regulatory agency's review at the practical level and reducing room for interpretation (e.g., making the positioning and submission requirements for third-party operational capability opinions clear). At the same time, the Tax Compliance Law passed in 2024 significantly enhanced the SII's powers in valuation, information collection, and anti-avoidance, meaning that for issues such as large OTC transactions, transfers between related parties, and valuation adjustments under extreme price volatility, the intensity and complexity of tax audits will rise.

Regulation of "payment-type" digital assets (especially stablecoins) and Central Bank Digital Currencies (CBDC) has become the core focus of the next stage of regulation. The BCCh has carried out proof-of-concept and pilot work for CBDC and has proposed special research on the regulation of stablecoins as a means of payment; both the practice sector and regulators are preparing to include tokens with "strong payment functions" in the currency/payment regulatory scope, and this type of regulation is likely to be promoted collaboratively by the BCCh and CMF. Therefore, for tokens issued or operated for payment purposes, issuers and Virtual Asset Service Providers providing related services need to assess possible license, capital, and liquidity requirements in advance.

regarding AML/CTF and cross-border intelligence cooperation, the Financial Action Task Force's (FATF) guidance on virtual assets and virtual asset service providers continues to constitute the international compliance benchmark. When designing registration, due diligence, and reporting obligations, Chilean regulatory agencies obviously align with the FATF's risk-based methodology. Therefore, Virtual Asset Service Providers should achieve technical and procedural alignment in customer identification, transaction information transfer, and cross-border cooperation as soon as possible to avoid compliance gaps in cross-border transactions.

In summary, the future focus of Chile's crypto asset regulation can be roughly summarized in three aspects: First, in terms of valuation and tax auditing, the SII is expected to strengthen the review of high-risk transactions and gradually promote the unification of valuation and reporting standards; second, the regulatory positioning of payment-type tokens will be clearer, especially rules related to stablecoins and Central Bank Digital Currencies (CBDC) may become stricter, and there is room for raising the thresholds for issuance and use; finally, international compliance collaboration and technical alignment will become a trend, and Virtual Asset Service Providers (VASPs) need to gradually implement transaction information reporting and "Travel Rule" requirements that comply with the Financial Action Task Force (FATF) and international standards.

For market participants, the implications at the practical level are mainly three points: 1. Establish stricter valuation mechanisms and complete transaction document retention systems; 2. Plan for liquidity and capital in advance when involving payment or exchange scenarios; 3. Optimize technical architecture to support cross-border information exchange and compliant reporting, reducing potential operational and regulatory risks.

4 Conclusion

With the rapid expansion of the Chilean crypto market, the country has established a crypto asset regulatory system that is both complete and transparent through tax rulings, legislation, and supporting regulatory measures. On the tax front, the SII has clearly defined the nature of crypto assets and transaction handling, providing tax guidelines for corporate and individual investors to follow; on the regulatory front, the CMF and the Anti-Money Laundering and Terrorist Financing Unit have formed an interconnected regulatory mechanism, making the compliance framework more systematic and actionable. The establishment of this system allows Chile to demonstrate significant institutional competitiveness within the region. On one hand, clear rules and regulatory paths have improved market predictability and legal security; on the other hand, tiered regulation and progressive implementation mechanisms have provided moderate flexibility for various fintech companies, balancing innovation and risk control.

Looking ahead, with the gradual implementation of international reporting standards, the Chilean market is expected to further align with global regulatory standards, attracting more institutional investors and compliant projects to enter the local market. For investors, Chile has become one of the few crypto asset investment destinations in the Latin American region that can simultaneously provide institutional transparency, clear compliance paths, and policy continuity, and its regulatory evolution will continue to set a benchmark for regional financial innovation.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.