Introduction

On May 29, 2025, the U.S. Securities and Exchange Commission (SEC) applied its regulatory framework from Proof of Work (PoW) to release the Statement on Certain Protocol Staking Activities, which systematically addresses the regulatory classification of protocol staking activities under Proof of Stake (PoS) mechanisms.

The statement highlights that in permissionless public blockchains (i.e., decentralized networks where anyone can participate without prior approval), when users stake assets through a protocol mechanism to participate in network consensus and receive rewards as per the rules, such "Protocol Staking Activities" do not involve the issuance or sale of securities as defined under Section 2(a)(1) of the Securities Act of 1933 or Section 3(a)(10) of the Securities Exchange Act of 1934. Participants in these staking activities are not required to register their activities with the SEC, nor are they subject to the registration exemptions under the Securities Act.

Only two months after clarifying that certain PoW mining activities do not constitute securities issuance, the SEC issued this statement, continuing its trend of exempting protocol-driven activities.This reflects the U.S. regulatory framework for crypto assets shifting from unclear enforcement to a more consistent and transparent approach. Since 2025, regulatory authorities have gradually established a distinction between "on-chain native participation behaviors" and "centralized fundraising activities," with the policy focus shifting from "broad coverage regulation" to "behavior-oriented categorized governance."

PoS, as one of the foundational consensus mechanisms, has long faced regulatory uncertainty. This SEC statement provides critical compliance guidelines for staking participants, node operators, and platform service providers, marking a clearer regulatory boundary for on-chain staking mechanisms. This article will further explore the SEC's regulatory attitude toward PoS protocol staking and discuss the extended implications of this statement in terms of securities classification and tax handling.

To better understand the SEC's regulatory rationale on PoS protocol staking, we will briefly compare the fundamental differences between PoS and PoW consensus mechanisms before beginning the analysis.

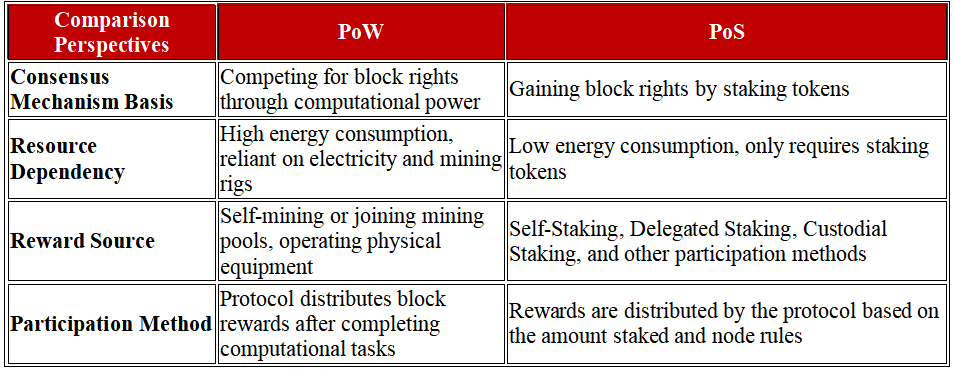

In our previous analysis report, we systematically introduced the operational logic of the Proof of Work(PoW) mechanism. PoW competes for block rights through computing power, requiring participants to invest substantial energy and hardware resources to calculate hash to complete transaction verification and obtain protocol rewards. The characteristic of PoW lies in its high energy consumption and high entry barriers, but it also provides strong resistance to censorship and network security.

In contrast, the Proof of Stake (PoS) mechanism replaces computing power input with asset staking, giving token holders the right to participate in consensus and maintain network security. Participants stake tokens in the on-chain protocol in exchange for block rights and reward distribution. In most PoS protocols, the probability of node selection is generally proportional to the amount of tokens staked, though other factors like validator performance may also apply, with the network's operation more reliant on "economic incentives" rather than "physical computation."

While Ethereum's transition to PoS during the 2022 “Merge” marked a pivotal moment in the mainstream validation of staking mechanisms, it is The Open Network (TON) that has brought PoS adoption to the next level. Unlike Ethereum's retrofit approach, TON was built from the ground up with a PoS architecture, enabling faster finality, lower fees, and native scalability. Its seamless integration with Telegram unlocks access to hundreds of millions of users, positioning TON as a powerful driver of mainstream participation in protocol staking. As the TON ecosystem rapidly expands, PoS-based consensus is becoming not only technically superior, but also more accessible and user-friendly than ever before.

Under the PoS mechanism, users can choose different ways to participate in staking, including:

l Self-Staking: Validators independently run nodes, participate in consensus, and obtain rewards.

l Delegated Staking: Users delegate staking rights to professional validators while retain asset ownership.

l Custodial Staking: Users transfer tokens to a trading platform or third party, which stakes on their behalf.

These mechanisms significantly reduce the participation threshold for ordinary users while also triggering widespread regulatory discussions about their compliance attributes. In particular, when node operation is handled by platforms and users no longer fully control their reward sources, whether staking remains protocol-driven and whether it constitutes securities issuance becomes the core issue addressed by the SEC in this statement.

1. Statement Interpretation

According to the statement, participants who meet the conditions set by the protocol stake assets to obtain consensus participation qualifications. Their rewards are automatically calculated and distributed by on-chain rules, independent of any specific entity's actions. Therefore, such activities do not meet the core element of the Howey Test, which requires "investment returns dependent on the efforts of others." As a result, these activities do not constitute securities issuance and do not require registration or application of the registration exemptions under the Securities Act.

Specifically, the SEC's perspective involves the following protocol staking activities and transactions:

l Staking crypto assets within a PoS network.

l Activities conducted by third-party participants (collectively referred to as "service providers") during protocol staking, including but not limited to third-party node operators, validators, custodians, delegators, and nominators, as well as their roles and responsibilities in reward acquisition and distribution.

l Provide ancillary services.

The statement applies only to protocol staking activities, including the following types:

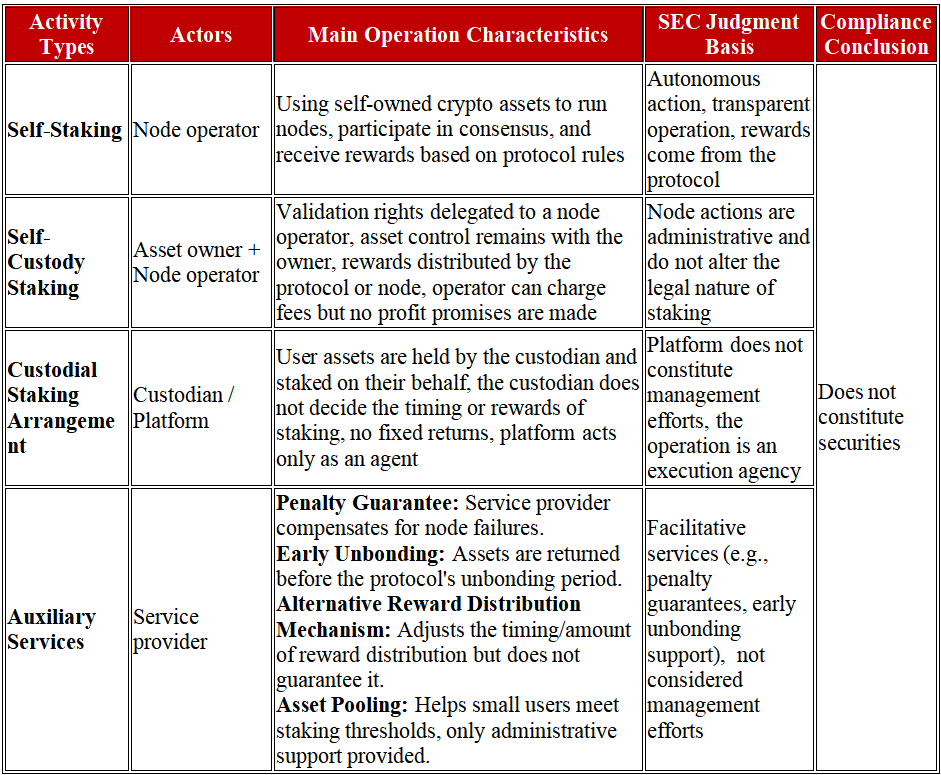

l Self-Staking: Node operators use their own resources to stake crypto assets they own and control. Node operators may be individuals or groups running nodes and staking their crypto assets.

l Direct Self-Custody Staking: Asset owners delegate validation rights to third-party node operators while retaining control of the assets. Rewards are either distributed directly by the protocol or through the node operator.

l Custodial Staking: A custodian stakes assets on behalf of users who have entrusted their assets to the custodian. In this arrangement, the custodian does not decide the timing or rewards of staking, and the platform only acts as an agent to execute staking.

The SEC emphasizes that protocol staking activities are not limited to users locking tokens to participate in consensus, but also include the staking execution and reward distribution duties performed by third-party service providers (such as node operators, validators, custodians, representatives, or nominators) and the auxiliary services provided around staking activities. In other words, whether these activities constitute securities depends not only on the staker but also on the role of each participant in the entire chain and whether their function exceeds the scope of "protocol execution."

Furthermore, the SEC explicitly recognizes three typical methods of participation in protocol staking: (1) Self-Staking: This involves node operators using their own crypto assets to run nodes, participate in consensus, and receive rewards. The activity is independent, and the operator bears the profit and loss;(2) Self-Custody Staking: In this method, asset owners delegate validation rights to third-party node operators but retain control over the assets. Rewards are distributed either by the protocol or through the node operator;(3) Custodial Arrangement: Users entrust their assets to a platform, which then represents the users in staking activities. In this structure, as long as the custodian does not make return promises or interfere with staking reward management, the activity is still considered part of protocol staking.

The SEC continues to adhere to the logic established in its earlier statement on PoW mining activities, which emphasized that "protocol-driven, self-participation, and service-supported" are the conditions under which protocol staking activities are not considered securities issuance. As long as the behavior structure does not deviate from the on-chain protocol rules and the service provider does not bear operational control obligations, securities law applicability can be excluded. This judgment framework also provides a reference boundary for determining compliance in complex scenarios involving staking on trading platforms, delegated node participation, and other similar situations.

Thus, the statement affirms that in permissionless PoS networks, user participation in consensus and reward acquisition through self-staking, self-custody staking, or custodial arrangements are not considered securities issuance and do not require registration or application of exemption procedures under securities law.

Key Points to Understand from the Statement:

l Limited Legal Effect, Clear Regulatory Guidance

This statement, as a guidance document issued by the SEC's Division of Corporation Finance, does not carry the force of law but reflects the regulatory agency's standards and boundaries for enforcement in the protocol staking field. It serves as an important policy reference and market guidance.

l Continued Mechanism Logic, Clear Scope of Application

The statement continues the logic of the previous PoW mining behavior judgment, explicitly excluding "protocol-driven, self-participation, and not relying on the efforts of others" on-chain activities from securities issuance. It includes self-staking, self-custody staking, and compliant custodial arrangements, providing a clear compliance positioning for mainstream PoS staking activities.

l Specific Conditions, Regulatory Boundaries Must Be Defined

The statement only applies to permissionless public chain protocol staking activities governed by protocol rules. If the staking process involves asset fundraising, fixed return commitments, platform operational interventions, or other financialized behaviors, it may exceed the scope of "protocol staking" and will require case-by-case determination to assess if securities issuance applies.

2. Discussion on Specific Activities

In addition to expressing its stance on the overall non-securities nature of protocol staking activities, the SEC also elaborated on several typical participation methods from a legal applicability perspective. As we outlined in our PoS analysis report, the SEC similarly referenced Section 2(a)(1) of the Securities Act and the classic Howey Test as the basis for its judgments, emphasizing the need to evaluate "economic realities" to determine whether the activity constitutes an "investment contract." In this framework, the statement analyzed four types of activities: self-staking, self-custody staking, custodial arrangements, and related auxiliary services, evaluating whether they satisfy the key elements of securities recognition.

In summary, the SEC has provided a detailed analysis of the legal characteristics of various typical protocol staking activities in this statement. Within the existing securities law framework, it has explained, step by step, why these activities do not constitute "investment contracts." This analysis not only continues the regulatory logic of compliance exemptions for on-chain native behaviors but also provides clear judgment criteria for various participation methods in practice.

It is worth noting that the statement begins by stating that its purpose is to "provide greater clarity on the application of federal securities laws to crypto assets." This phrasing reveals a clear shift in regulatory direction—the SEC is gradually moving from "enforcement-driven" to "rule transparency." By making public statements and offering systematic clarifications, the SEC aims to guide market participants in understanding which on-chain activities fall within the scope of securities regulation and which can obtain clear compliance exemptions. This is not only a clarifying statement but also signals the shift toward a more stable and systematic regulatory approach.

3. Tax Treatment of PoS Rewards

The SEC statement clearly excludes "compliant staking behaviors" from the definition of securities issuance, providing clear boundaries for staking participants and node operators. However, tax compliance issues related to PoS staking behaviors should also be addressed.

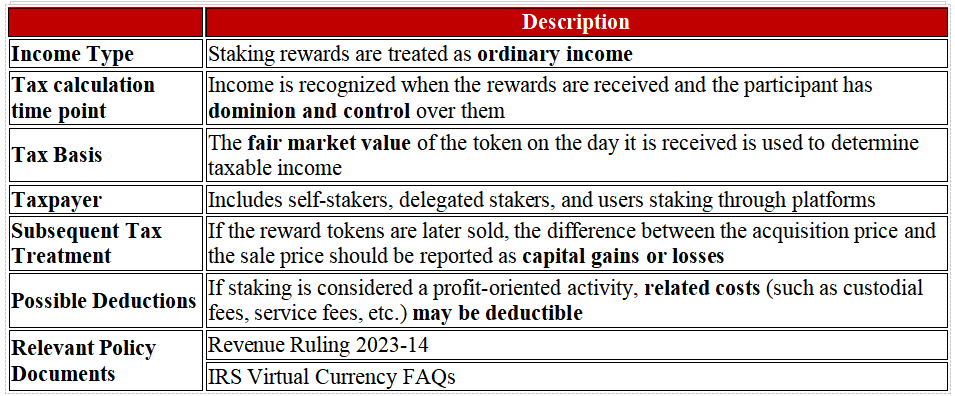

According to the IRS's Revenue Ruling 2023-14, taxpayers who receive rewards through PoS staking should report the fair market value of those rewards as ordinary income when they gain "dominion and control" over the rewards, even if they do not sell them. In other words, once participants can freely dispose of the rewards, a taxable event occurs. Additionally, if the assets are sold later, capital gains or losses should be reported based on the difference between the acquisition price and the sale price.

This policy logic aligns with the IRS's earlier tax treatment of mining income in Notice 2014-21, indicating that U.S. tax authorities apply the "tax upon acquisition" principle to on-chain incentive income. At the same time, if staking activities constitute continuous, profit-driven commercial activities, related expenses (such as transaction fees, node operation costs, etc.) may be deducted as operating costs depending on the circumstances.

It is worth noting that whether PoS staking rewards should be recognized as taxable income "upon receipt" has sparked substantial controversy. A representative case is Jarrett v. United States in 2021. In this case, taxpayers Jarrett and his spouse received token rewards for participating in the Tezos network's protocol staking but refused to report the income unless the tokens were sold, arguing that staking rewards should not be taxed before sale. They filed a lawsuit in the U.S. District Court for the Middle District of Tennessee to recover the taxes paid on staking rewards.

Initially, the IRS agreed to refund the taxes and proposed a settlement, but Jarrett rejected the offer, seeking only to clarify the legal application through case law. However, in 2023, the court dismissed the lawsuit on the grounds of "mootness," meaning there was no longer a substantial issue to resolve, and did not make a substantive ruling on the tax status of staking rewards. Although the case did not alter the existing policy, it sparked widespread attention and led to the IRS issuing Revenue Ruling 2023-14, which clarified for the first time that PoS rewards should be reported as ordinary income upon gaining "dominion and control," reinforcing the "tax upon acquisition" stance.

In 2024, the Jarretts initiated a new lawsuit regarding the 2020 staking rewards, claiming that the rewards should be considered "creative output" and that tax obligations should arise only upon monetization or sale, not upon receipt. They requested the court to confirm that the IRS's rules were incorrectly applied and to refund the taxes paid. The case is still under trial in the Federal District Court for the Middle District of Tennessee, and no judgment has been made. While the outcome is still uncertain, the case is seen as an important challenge to the "tax upon acquisition" principle within the crypto industry. If the Jarretts receive a favorable ruling, it could significantly change the taxation of crypto assets staking rewards, potentially allowing taxpayers to defer taxes on tokens obtained through staking activities.

Therefore, even though the SEC has defined the non-securities boundary for protocol staking under securities law, staking participants must still fulfill full reporting and record-keeping obligations under tax law to ensure consistency between "non-securities compliance" and "tax compliance."

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.