I. Introduction

Not long ago, with the opening of WebX 2025 in Tokyo, Japan once again drew global attention to the crypto market. In fact, as blockchain technology and crypto assets rapidly develop, Japan has become a key player in the global crypto asset market. It not only has many tech developers and individual investors but also attracts numerous Web3 institutions to jointly explore the future of Japan's digital finance. Driven by both tech innovation and risk control, Japan's crypto asset ecosystem is gradually maturing.

According to the 2024 annual report from the Japan Virtual and Crypto Asset Exchange Association (JVCEA), the number of crypto asset accounts in Japan has exceeded 12 million, with user deposit balances over 5 trillion yen. Among them, the holding rates for mainstream crypto assets like Bitcoin and Ethereum have risen significantly. Institutional investors are showing growing interest in crypto asset investments, with 57% of respondents believing that crypto assets will go mainstream in the future. Additionally, there's a stronger public call for regulatory transparency. These data together paint a picture of a market with broad awareness, diverse applications, and clear expectations for regulation.

In this context, understanding Japan's crypto asset tax system and regulatory framework is essential for crypto businesses to comply and develop, as well as for investors to spot market risks. This study will focus on two main lines: the basic tax system and the regulatory framework, to show the interaction between institutions and the market in Japan's crypto asset ecosystem, aiming to give readers a clear overview of Japan's crypto asset system.

II. Japan's Basic Tax System and Crypto Asset Tax Treatment

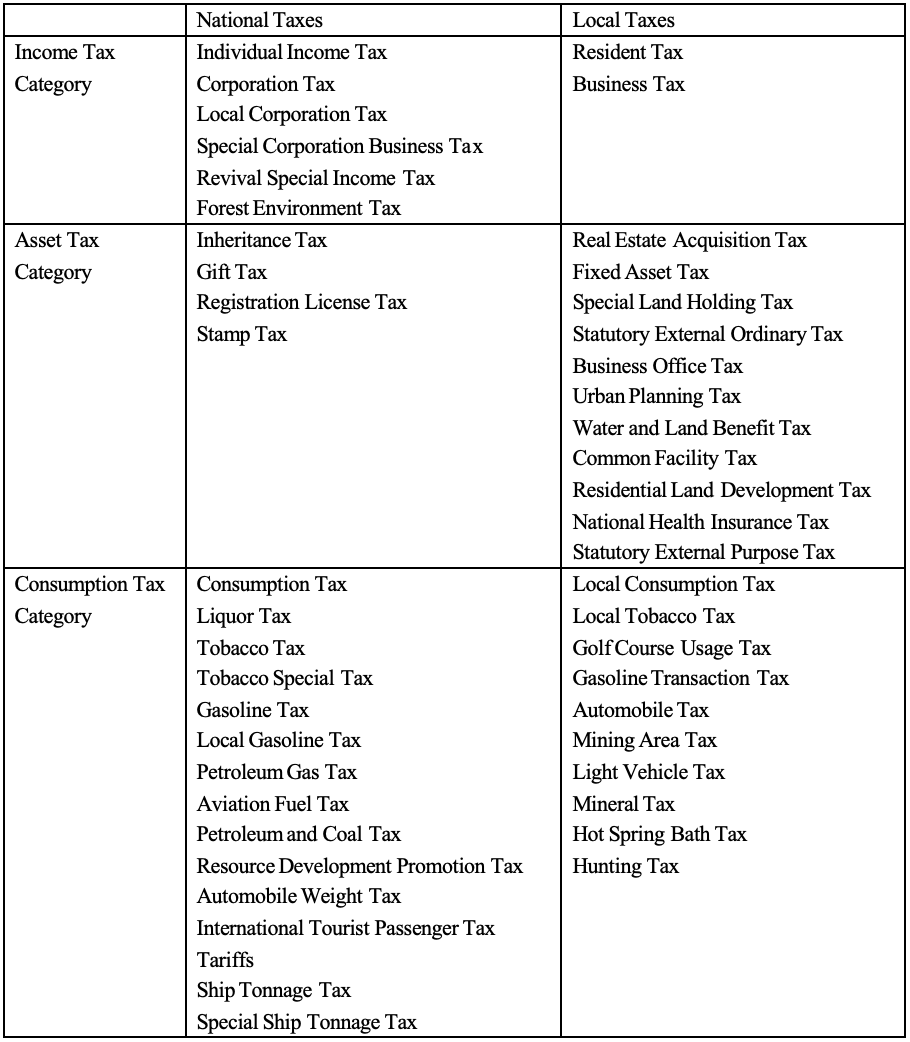

Japan is a country mainly based on direct taxes, with current major tax types including: corporation tax, individual income tax, consumption tax, liquor tax, tariffs, inheritance and gift tax, fixed asset tax, stamp tax, etc. This article will focus on introducing the basic tax systems of tax types strongly related to crypto assets and the related crypto asset tax treatment methods. Japan's current tax types are mainly shown in the table below:

1. Corporation Tax

Japan's corporation tax is a tax levied on the income generated from a corporation's business activities, which is a type of income tax in a broad sense (Japan's income tax refers to individual income tax, detailed below). Corporations with headquarters or main offices in Japan are resident enterprises, while others are non-resident enterprises. For resident enterprises, all income, whether from domestic or foreign sources, is subject to taxation, while non-resident enterprises are only obligated to pay tax on their income sourced in Japan. In calculating taxable income, a company's revenue is the sum from all sources, with no specific requirements to distinguish types of income. The standard corporation tax rate is 23.2%, and for corporations with registered capital of 100 million yen or less, the portion of income up to 8 million yen applies a 15% rate (however, if the company's taxable income exceeds 1 billion yen, this preferential rate increases to 17%).

2. Income Tax

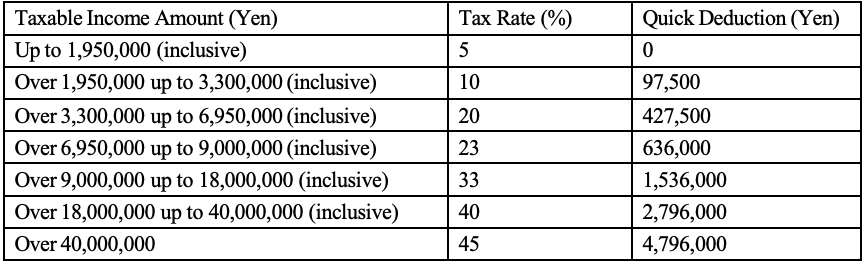

Income tax is levied on an individual's income. In Japan, permanent resident taxpayers must pay tax on their global income. Non-resident taxpayers only pay tax on their Japan-sourced income. Non-permanent resident taxpayers are taxed on their income except for foreign-sourced income not remitted to Japan (especially possibly including certain capital gains), and may be taxed on parts of foreign-sourced income paid or remitted to Japan. Japan divides taxpayers' taxable income into ten categories, calculated separately: salary income, interest income, dividend income, business income, real estate income, retirement income, transfer income, forestry income, one-time income, and miscellaneous income (income not covered by the first nine items; current Japanese tax law classifies personal income from crypto assets as miscellaneous income). When calculating the individual income tax amount, determine and aggregate each person's taxable income, subtract necessary expenses from the income amount, and apply income deductions according to relevant regulations to get the taxable income tax, then calculate the individual's income tax payable for the year based on the applicable tax rate. The current Japanese national individual income tax rate table is as follows:

3. Consumption Tax

Japan's consumption tax is levied when businesses transfer goods, provide services, or import goods into Japan. The general tax rate is 10%, but a lower rate of 8% applies to food and beverages (excluding those consumed in restaurants and alcoholic beverages) as well as subscriptions to newspapers that meet specific conditions. Exports and certain services provided to non-residents apply a zero tax rate. Specific transactions, such as sales or leases of land, sales of securities, and provision of public services, are not within the taxable scope.

4. Inheritance Tax and Gift Tax

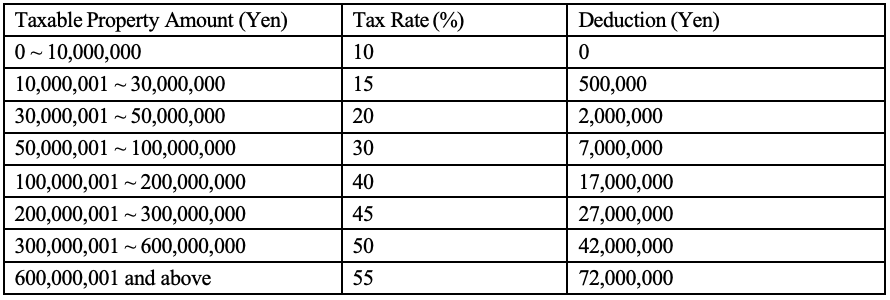

Inheritance tax is a tax levied on property when property transfers occur due to a person's death. The taxable objects of inheritance tax include various forms of assets such as cash, savings and deposits, stocks and other financial assets, as well as movable and immovable property. The taxpayers obligated to pay inheritance tax are individuals who acquire property through inheritance or bequest. The inheritance tax rate is set for each heir's inherited estate exceeding the threshold, applying a progressive tax rate of 10%-55% based on the scale of the taxable estate. The specific tax rates are detailed in the table below:

Gift tax is a tax levied on property when property transfers occur due to gifts. Gift tax is generally a supplementary tax to inheritance tax. Japan's gift tax, for property acquired through gifts within one year, even if from different donors, combines the amounts for taxation. The taxpayers obligated to pay gift tax are individuals who acquire property through gifts. When corporations acquire property through gifts, corporation tax is levied. The taxable objects of gift tax are properties acquired through gifts. Here, property includes all items and rights that can be objects of property rights. There are two methods for taxing gift tax: "calendar year taxation" and "settlement taxation at inheritance" (integrated measures for inheritance tax and gift tax). The calendar year taxation system for gift tax applies a progressive tax rate of 10%-55%.

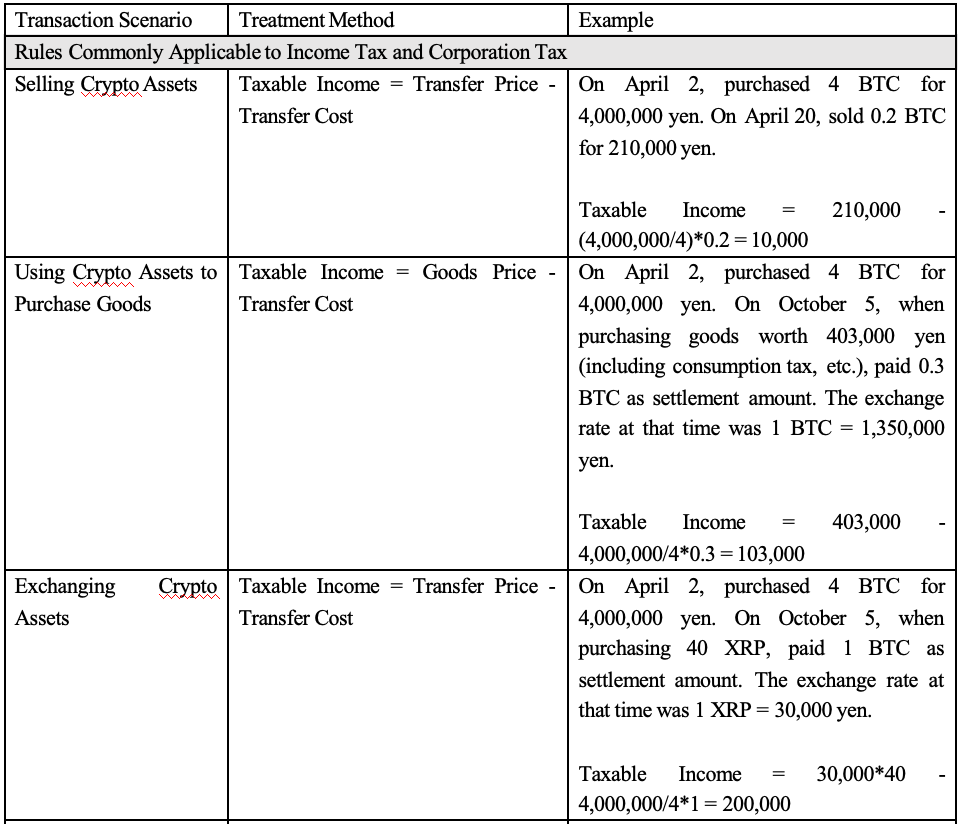

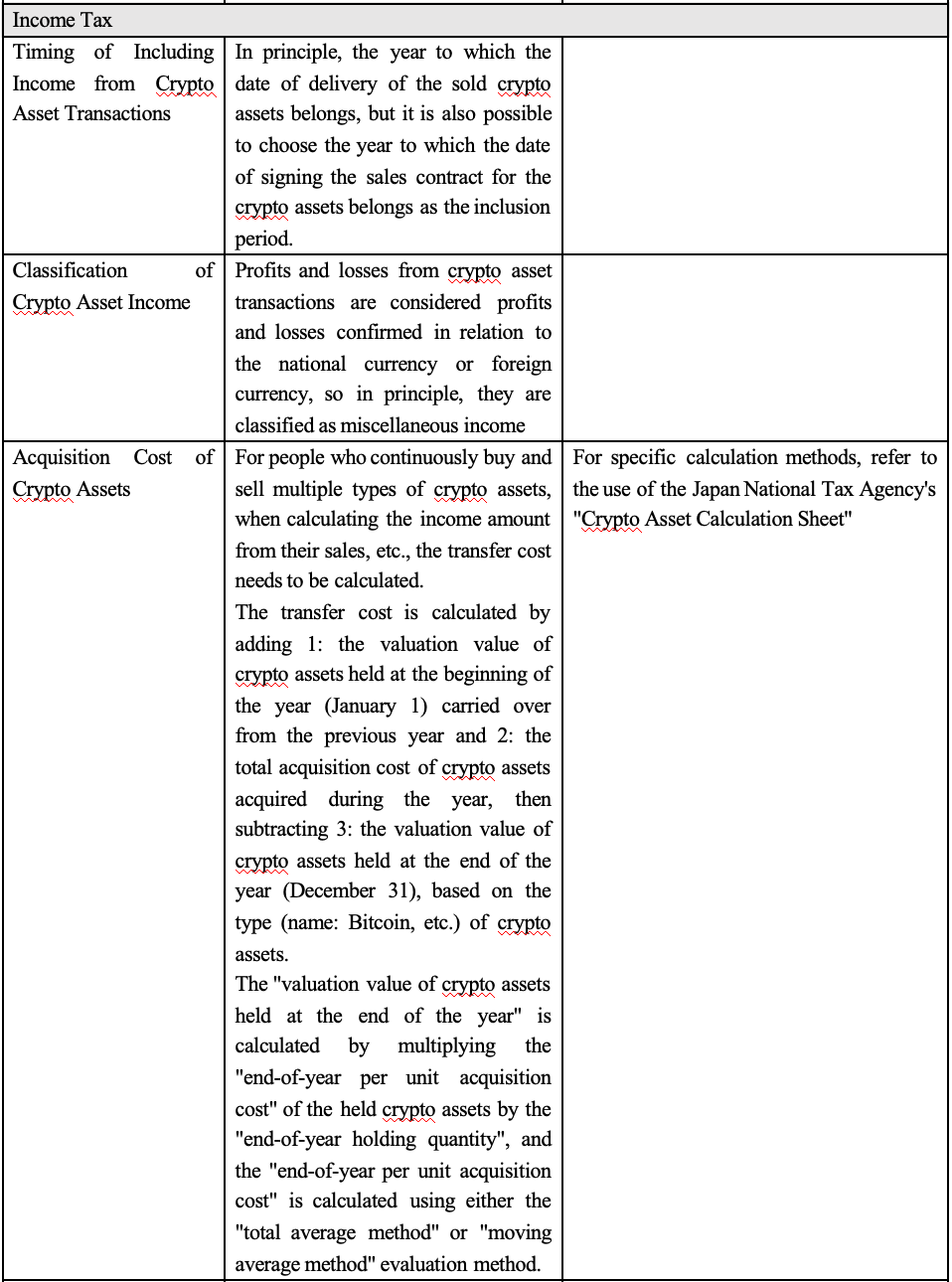

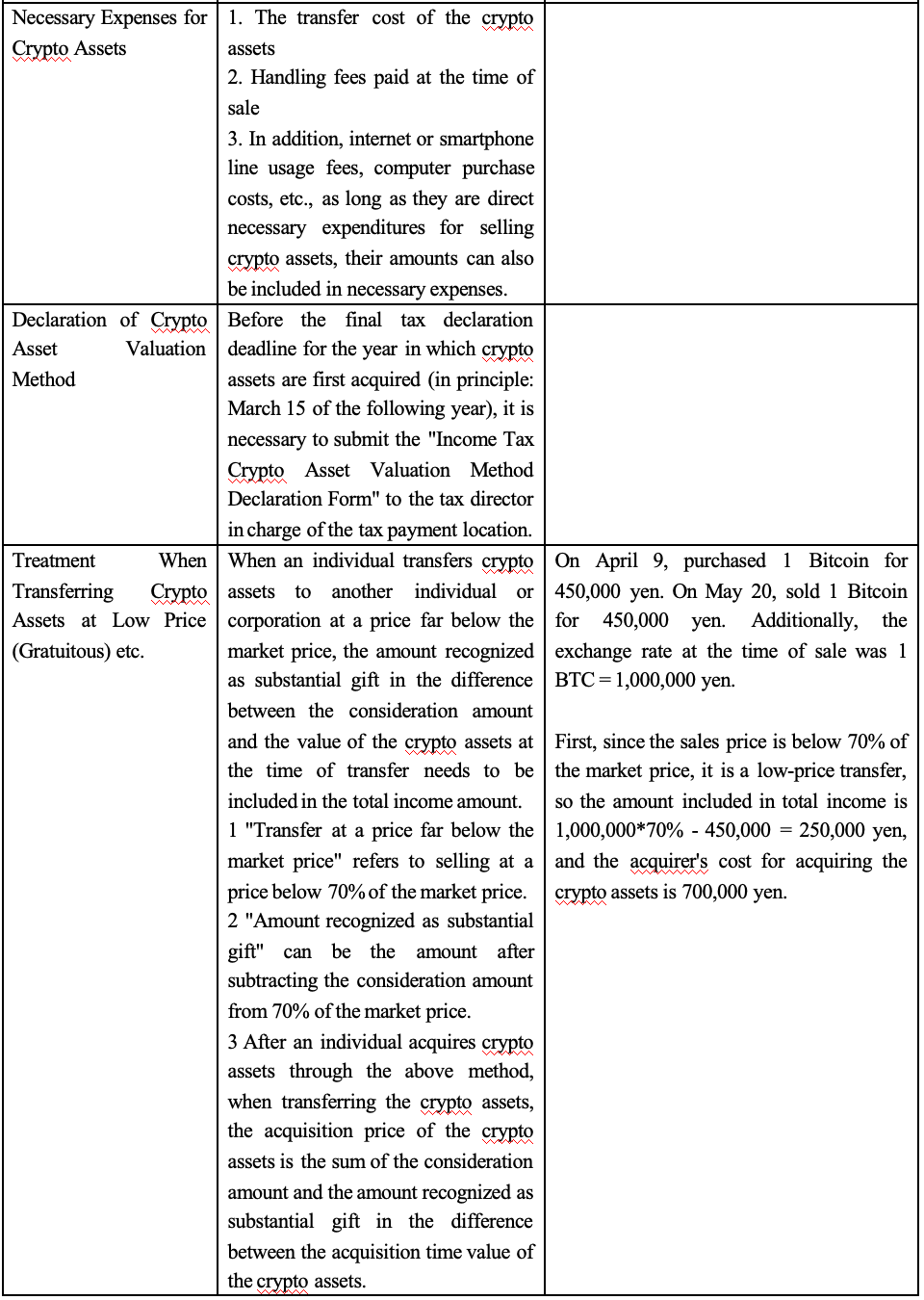

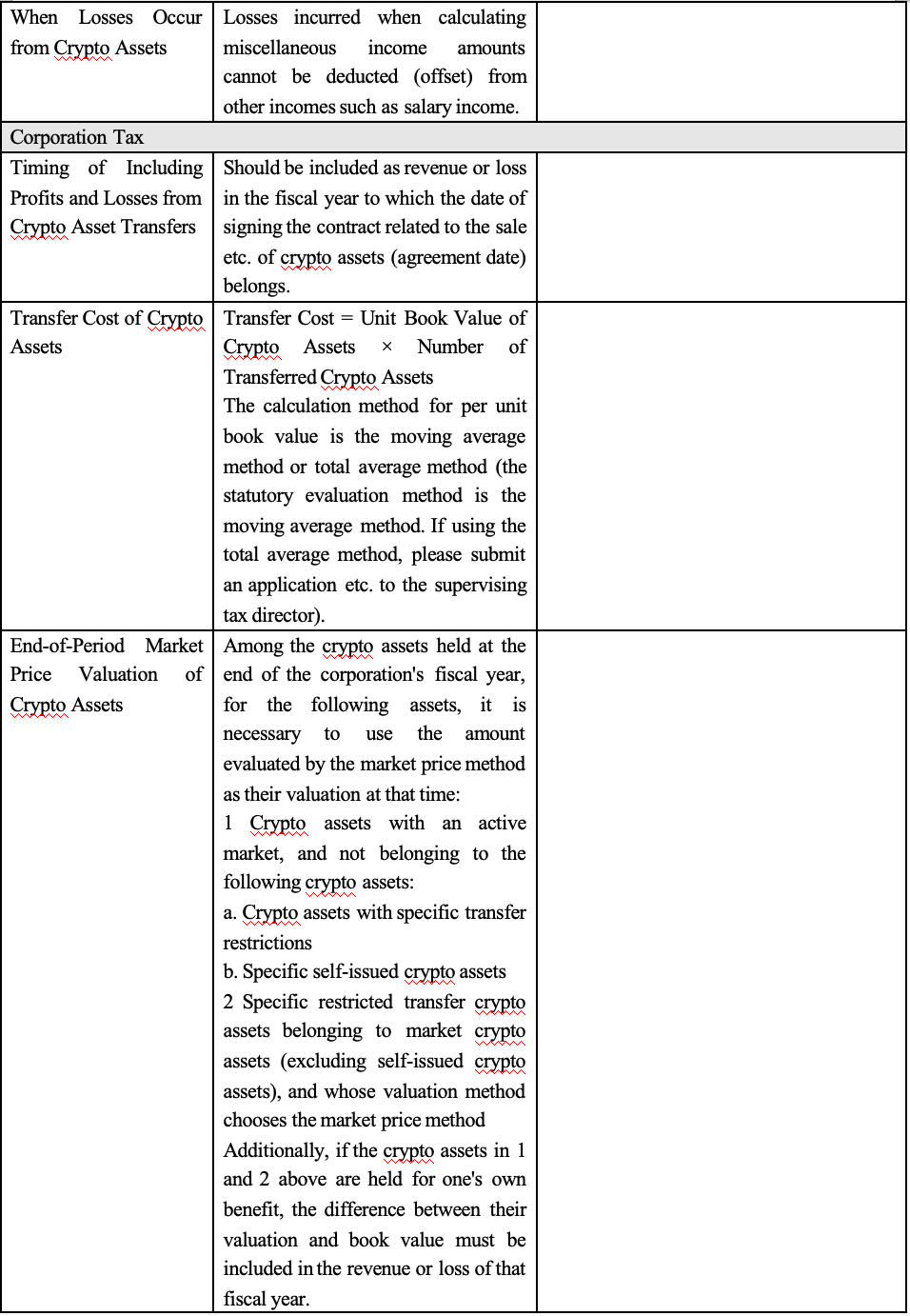

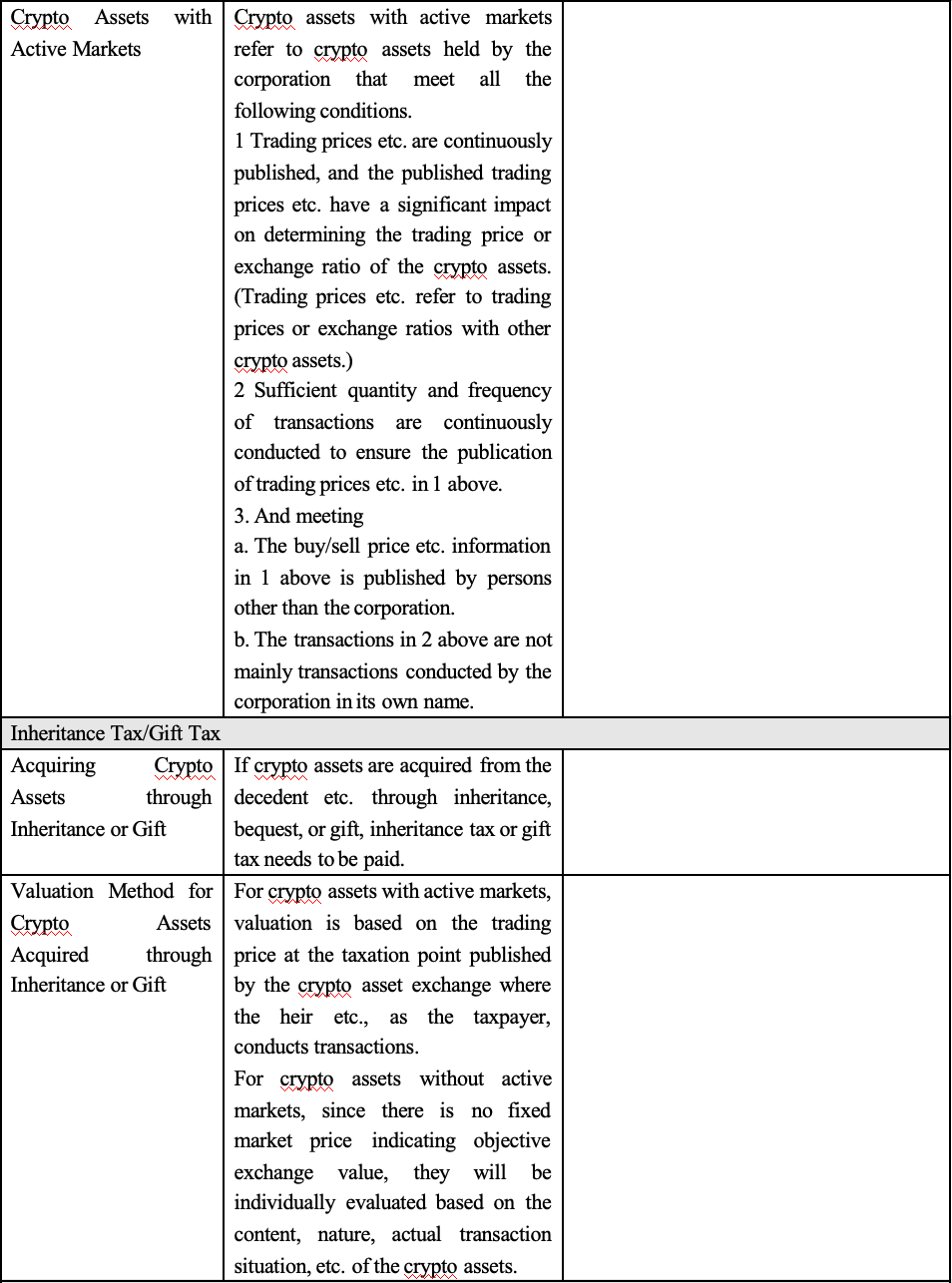

5. Tax Treatment of Crypto Assets

6. Reform Trends

In December 2024, the Japanese government released the "FAQ on Tax Treatment of Crypto Assets etc.", compiling common questions on tax treatment of crypto assets and electronic payment means, including income tax, corporation tax, consumption tax, gift tax, inheritance tax, etc. For specific treatment methods, please refer to the relevant documents. Recently, JCBA and JVCEA collaborated to compile a request on tax reforms related to crypto assets for the 2026 fiscal year, which was submitted to the government for review on July 30. Therefore, this section will focus on analyzing and comparing Japan's crypto asset tax reform proposals with the current system, as shown in the table below:

From the table above, it can be seen that the current system's progressive tax rates are very unfriendly to high-frequency traders and high-net-worth investors, while the proposals will significantly reduce the tax rate to 20% and allow loss carryforward, which is beneficial for attracting capital back to the Japanese market. At the same time, deferred taxation on coin-to-coin transactions will greatly simplify declaration and record-keeping obligations, reducing the pressure of tracking a large number of transaction details. Additionally, lowering tax barriers for donations and inheritances may promote the application of crypto assets in social donations and wealth inheritance fields. These proposals from Japan are clearly leaning towards attracting the crypto industry and funds.

III. Basic Research on Japan's Crypto Regulation

1. Basic Framework

Japan is one of the earliest jurisdictions globally to incorporate crypto asset trading into the statutory financial regulatory system, building a relatively complete dual-track regulatory framework through the Payment Services Act (PSA) and the Financial Instruments and Exchange Act (FIEA). The former focuses on the registration of crypto asset exchange operators, asset custody, anti-money laundering and counter-terrorist financing (AML/CFT), and user protection; the latter targets security tokens (STO), investment-type token ICOs, derivatives, etc., establishing strict information disclosure, market manipulation prohibition, and investor protection systems. The two laws have divisions of labor but connect through specific clauses, making crypto assets have clear compliance boundaries from payments to investments, from spot to derivatives. Since 2018, Japan has implemented a mandatory registration system for crypto asset trading platforms, and through multiple amendments in 2019 and 2022, it has raised requirements for cold wallet custody ratios, advertising standards, cross-border transfer information disclosure, etc. The FSA maintains a high-pressure stance on unregistered operations and closely monitors emerging forms like DEX, stablecoins, and Staking, indicating a continuing expansion of regulatory scope.

Under this framework, the Financial Services Agency (FSA) is the national-level supervisory authority. Additionally, the Japan Virtual Currency Exchange Association (JVCEA) and the Japan Cryptoasset Business Association (JCBA) also play important roles in Japan's crypto asset industry. JVCEA is an industry self-regulatory organization voluntarily established by major virtual currency exchanges. With the development of Japan's crypto market and the emergence of related risk events, the Japan Financial Services Agency (JFSA) officially authorized JVCEA in 2018 as an official industry organization with self-regulatory duties. This means JVCEA not only formulates standards for member exchanges on operations, risk control, anti-money laundering, etc., but also assists the government in implementing regulation, responding timely to industry changes and risks. JVCEA not only improves industry transparency and compliance levels but also becomes a key driving force for exchanges to obtain legal operating qualifications, protecting investor interests and rebuilding market confidence.

Unlike JVCEA's focus on exchanges and regulatory self-discipline, JCBA emphasizes promoting the overall development of the crypto asset industry. JCBA's members cover diverse institutions such as wallet service providers, blockchain enterprises, market participants, etc. The association mainly promotes industry innovation and ecosystem improvement through industry exchanges, technical research, policy suggestions, and popular education. JCBA plays a bridging role in communicating with regulatory agencies, negotiating tax policies, formulating standards, and addressing emerging industry issues. The two form a division of labor and complementary relationship, jointly promoting the standardized, healthy, and diversified development of Japan's crypto asset industry.

2. Legal Evolution

Japan is one of the earliest countries to establish a regulatory framework for crypto assets (previously called virtual currencies). As early as 2016, Japan amended the Payment Services Act (hereinafter "PSA") to first respond to international requirements on anti-money laundering (AML) and counter-terrorist financing (CFT), and to make institutional responses to bankruptcy events of domestic operators providing exchange services between crypto assets and fiat currencies. This amendment (implemented in April 2017, hereinafter "2016 Amendment") established a registration system for relevant service providers and introduced a series of measures, including identity verification at account opening, full explanation of transaction terms to users, implementation of separation management of client assets and own assets, etc., thus establishing basic norms in anti-money laundering and consumer protection.

As the crypto asset market developed, some new risks and issues gradually emerged: for example, abuse of high-anonymity crypto assets, insufficient internal management of some crypto asset exchange service providers (hereinafter "exchange service providers"), incidents of leakage or misappropriation of user-entrusted crypto assets and funds, and excessive advertising, etc. In view of these situations, Japan amended the PSA and FIEA again in 2019 (this amendment implemented in May 2020, hereinafter "2019 Amendment"). The main contents of the 2019 Amendment include: requiring exchange service providers to report in advance when changing the crypto assets they handle, rather than afterward; in principle, must use cold wallets to store user crypto assets; establishing regulatory rules for advertising and solicitation. At the same time, to address new transaction behaviors and improper transactions, it clarified that derivative transactions involving crypto assets are included in regulation, and ICO tokens granting profit distribution rights should apply FIEA. It also prohibited unfair trading behaviors such as price manipulation.

On this basis, Japan amended the Act on Prevention of Transfer of Criminal Proceeds in 2022 (implemented in June 2023, hereinafter "2022 Amendment"), introducing the "Travel Rule" in accordance with the recommendations of the Financial Action Task Force (FATF). This rule requires that when exchange service providers transfer crypto assets on behalf of users, they must pass the identity information of the sender and receiver together to the receiver's exchange service provider.

In 2025, the Japanese government has submitted a PSA amendment bill draft to the Diet (unless otherwise specified, the "amendment" in the following text refers to this amendment bill draft). It includes: granting regulatory authorities the power to require exchange operators to keep assets in Japan, to ensure that in extreme cases like bankruptcy, assets can still be returned to domestic users; and adding a new intermediary business category specifically for matching buys/sells or exchanges between crypto assets.

3. Important Rules

1. Market Entry and Registration Management

Registration System

No entity may provide crypto asset exchange services without registration with the Japanese Prime Minister (executed by the Financial Services Agency FSA).

Registration Application

Must submit a written application, including: company name, address, capital, executive names, names of crypto assets to be handled, business content and methods, etc.

Strict Registration Rejection Criteria

The Financial Services Agency must reject registration in the following cases:

• Company form: Non-stock company or foreign company without a business office in Japan.

• Financial foundation: Does not have a sound financial foundation.

• System construction: Has not established necessary systems to ensure normal and stable business operations (such as compliance systems).

• Industry self-regulation: Has not joined a certified industry self-regulatory organization or has not formulated equivalent internal rules.

• Violation records: The company or executives have been penalized for violating relevant laws in the past five years.

• Historical records: The company has had relevant licenses revoked in the past five years.

• Executive qualifications: Executives have unfit circumstances (such as bankruptcy, criminal records, etc.).

Changes and Filings

When changing important matters such as the types of crypto assets handled, business models, etc., must report to the Financial Services Agency in advance.

Prohibition of Lending Licenses

Strictly prohibit lending one's name to others to engage in crypto asset exchange services.

2. Business Operation Norms

Information Security Management

Must take necessary measures to prevent leakage, loss, or damage of business-related information.

Advertising Norms

Advertisements must clearly indicate the service provider's name, registration number, and clearly inform that "crypto assets are not fiat currencies" as well as risks like price fluctuations.

Prohibited Behaviors

Strictly prohibit making false statements, misleading promotions, or speculative promotions for profit purposes.

User Protection and Information Explanation

Before signing a contract, must fully explain to users the characteristics of crypto assets, fees, and contract terms; when providing leveraged trading, must additionally explain risks.

User Asset Segregation Management

• User funds (fiat): Must be separated from the company's own funds and entrusted to a trust company for management.

• User crypto assets: Must be separated from the company's own crypto assets; most assets must be managed using high-security methods (such as cold wallets).

• Performance guarantee system: For user assets in hot wallets, the service provider must hold the same type and quantity of own crypto assets as performance guarantee and manage them separately.

• Regular audits: The segregation management of user assets must undergo regular audits.

Dispute Resolution Mechanism

Must sign a contract with a designated dispute resolution organization or establish other effective complaint handling and dispute resolution mechanisms.

3. Supervision and Management

Books and Reports

Must prepare and preserve business books as prescribed; each fiscal year must submit audited business reports and financial documents to the Financial Services Agency.

Inspections and Inquiries

The Financial Services Agency has the right to require service providers to submit reports and materials, and may conduct on-site inspections and inquiries at any time.

Business Improvement Orders

When the Financial Services Agency deems it necessary, it can order the service provider to take measures to improve its business operations or financial condition.

License Revocation and Business Suspension

If the service provider has violations, improper acquisition of registration, or meets "rejection of registration" criteria, etc., the Financial Services Agency may revoke its registration or order suspension of business.

4. Exit and Special Provisions

User Asset Priority Repayment Right

The user's claim for return of crypto assets has priority over other creditors of the service provider, which is an extremely important user protection clause.

Business Termination and Liquidation

Termination of business requires advance announcement and notification to the Financial Services Agency. After license revocation or business termination, the primary obligation is to complete all unfinished transactions and return user assets.

Additionally, if crypto assets have securities nature, they apply the higher requirements of the Financial Instruments and Exchange Act (FIEA) for information disclosure and regulation of behaviors like market manipulation and fraud.

4. Amendment Dynamics

4.1. Introduce Domestic Asset Preservation Orders for Crypto Asset Exchanges

Previously, Japanese authorities were concerned that crypto asset exchanges handling spot trading might transfer their assets overseas, thereby harming user interests in cases like bankruptcy. The relevant amendment allows the Japanese government to issue "Asset Retention Orders" to prevent such asset outflows, ensuring user asset safety.

4.2. Implement More Flexible Management Requirements for Reserves of Trust-Based Stablecoins

Previously, stablecoin issuers were required to hold all reserves in the form of demand deposits. This amendment allows issuers to hold up to 50% of their reserves in low-risk assets such as government bonds or redeemable time deposits. It is expected that this change will enhance the international competitiveness of Japan-issued stablecoins.

4.3. Newly Establish Crypto Asset Brokerage Business Category

Previously, institutions only engaging in crypto asset intermediation also needed to register as full exchanges, with high entry barriers. The amendment adds a "brokerage business" category, allowing intermediary institutions to operate under an independent regulatory framework, lowering entry barriers, more fitting industry reality, and helping promote new service providers entering the market. This measure is consistent with regulatory practices in other financial fields.

4.4. Regulation of Cross-Border Collection Services

In the past, cross-border collection services were basically unregulated, not requiring money transfer business licenses, but there were risks of abuse for illegal gambling, investment fraud, etc. The new rules have strengthened regulation on such services. The core of the new rules is to crack down on unregistered illegal money transfers. For high-risk businesses, additional strengthening of consumer protection and anti-money laundering (AML) measures. Services that do not directly facilitate goods or service transactions will be included in money transfer business regulation; while low-risk services like platforms directly participating in transactions or third-party custodians already regulated by other laws may be exempted. Industry groups like the Japan New Economy Association are concerned that excessive regulation may harm the digital payment industry, so they call for the new rules to focus on actual risks, avoiding impact on ecosystems like electronic payments and point settlements. Subsequent detailed regulations need close attention to their impact on the industry and innovation.

4.5. Speed Up User Refunds in Case of Bankruptcy of Money Transfer Institutions

In the past, even if user assets were guaranteed by banks or trusts, the refund process still required government leadership, taking at least 170 days. The new amendment introduces a direct refund path, where banks or trust institutions can directly return funds to users without going through the original procedures. This measure enhances consumer protection, effectively improving the efficiency of financial services, allowing funds to be returned to users faster and safer when institutions have problems.

IV. Conclusion

In summary, Japan has gradually perfected its tax regulation and financial regulation institutional pattern in the crypto asset field: on one hand, the tax system centered on the NTA has made detailed provisions for income tax, corporation tax, inheritance tax, gift tax, etc., on crypto assets, although the current system still imposes certain constraints on investment activity in terms of tax rates, loss carryforward, taxation timing, etc., but the 2026 fiscal year tax reform proposals have clearly evolved towards reducing tax burden, facilitating transactions, and being friendly to public welfare; on the other hand, the financial regulatory framework led by the FSA, through the Payment Services Act, Financial Instruments and Exchange Act, and supporting management by self-regulatory organizations (JVCEA), has made Japan the first globally to establish a full-chain compliance system covering spot, derivatives, stablecoins, etc., and continues to iterate to address new technologies and new business models.

This steady optimization of tax system and regulation not only responds to the domestic market's needs for transparency, efficiency, and international alignment but also reflects Japan's development idea of deeply integrating crypto assets with Web3.0 strategy. In the future, with the implementation of separate taxation, deferred taxation on coin-to-coin transactions, inheritance and donation incentives, etc., as well as the improvement of more flexible market entry and consumer protection mechanisms, Japan is expected to significantly enhance its competitiveness in the global crypto asset and blockchain industry chain while maintaining high-level risk control, attracting more capital, technology, and entrepreneurial projects to land in its market, thereby further consolidating its leading position in the Asia-Pacific and even global digital finance landscape.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.