Driven by the demographic dividend of a young population, a massive demand for overseas labor remittances, and the early popularity of P2E games, the Philippines ranks among the top in global cryptocurrency adoption rates. Corresponding to market development, cryptocurrency regulation in the Philippines has gradually tightened and become clearer in recent years. The country uses licensing management as its basic approach, forming a dual-track regulatory structure under the Bangko Sentral ng Pilipinas (BSP) and the Securities and Exchange Commission (SEC). On the taxation front, the Philippines has not yet enacted independent tax legislation specifically for cryptocurrency. The tax treatment of income related to crypto activities relies on the existing tax system centered around the National Internal Revenue Code (1997). Based on the current legal system and policy dynamics in the Philippines, this article outlines the tax logic for cryptocurrencies in the country, introduces the macro-regulatory framework for conducting crypto-related activities in the Philippines, and tracks the policy trends of core regulatory bodies to provide compliance references for the industry.

The Philippines uses the currently effective National Internal Revenue Code (NIRC) as its basic tax law. Its tax system presents a dual structure of National Taxes and Local Taxes. Among them, national taxes are implemented and collected by the Bureau of Internal Revenue (BIR), mainly including Income Tax, Value Added Tax, Excise Tax, Percentage Tax, and Documentary Stamp Tax. Local taxes are levied by local tax authorities based on authorizing provisions, mainly including Real Property Tax and Business Tax. The tax rates are set by local councils within statutory limits through local tax ordinances. Furthermore, local tax authorities have no right to levy certain specific taxes, such as income tax (except those levied on banks and other financial institutions), documentary stamp tax, or percentage tax or value-added tax generated from sales, barters, exchanges of goods, or services, or other similar transactions.

The major taxes in the Philippines include income tax, value-added tax, excise tax, documentary stamp tax, customs duties, and percentage tax, with indirect taxes accounting for a large proportion of the tax system.

(1) Personal Income Tax

Under the NIRC and the Tax Reform for Acceleration and Inclusion (TRAIN Law), resident taxpayers in the Philippines are required to pay personal income tax on their global income, while non-resident taxpayers are only taxed on their income sourced within the Philippines. The standard for distinguishing between residents and non-residents is nationality, and all Philippine citizens are considered residents.

The classification of tax status for natural persons and the corresponding tax treatments are as follows:

Resident Citizen: Philippine citizens residing within the Philippines. According to Section 23(A) of the NIRC, resident citizens are taxed on their income derived from sources within and outside the Philippines.

Non-resident Citizen: Refers to Philippine citizens who meet the provisions of Section 22(E) of the NIRC, including Philippine citizens who can prove to the Commissioner of Internal Revenue their physical presence abroad with a clear intention to reside therein; Philippine citizens who leave the Philippines during the taxable year to reside abroad, either as an immigrant or for employment on a permanent basis; and Philippine citizens who work and derive income from abroad and whose employment thereat requires them to be physically present abroad most of the time during the taxable year. According to Sections 23(B) and 23(C) of the NIRC, non-resident citizens and overseas contract workers are generally taxable only on income derived from sources within the Philippines.

Resident Alien: Refers to individuals whose residence is within the Philippines but who do not have Philippine citizenship. According to Sections 22(F) and 23(D) of the NIRC, resident aliens are taxable only on income derived from sources within the Philippines.

Non-resident Alien: Refers to individuals whose residence is not within the Philippines and who do not have Philippine citizenship. According to Sections 22(G) and 23(D) of the NIRC, non-resident aliens, regardless of whether they are Philippine tax residents or not, are taxable only on income derived from sources within the Philippines; if a non-resident alien stays in the Philippines for an aggregate period of more than 180 days during any calendar year, they shall be deemed a non-resident alien doing business in the Philippines and taxed according to the corresponding rules.

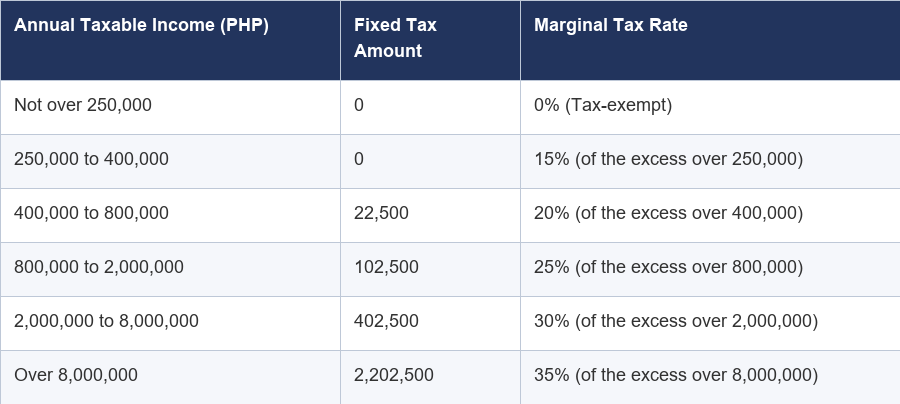

Among them, personal income tax adopts a six-tier progressive tax rate:

Table 1: Tax Rates on Personal Taxable Income (Effective from January 1, 2023)

Additionally, the Philippines implements preferential policies of tax credits, tax deductions, and tax exemptions for individuals meeting specific conditions. Tax credits include foreign tax credits and withholding tax credits. Tax deductions include the deduction of statutory mandatory contributions such as social security, health insurance, housing provident fund (Pag-IBIG), and union dues. For self-employed individuals and professionals, an optional standard deduction of 40% and deductions for necessary expenses related to the business or practice of profession are available. Tax exemptions, such as the 13th-month pay and other productivity incentive benefits received by all Philippine employees, can be excluded from gross income and are not included in taxable income up to a total limit of PHP 90,000.

(2) Corporate Income Tax

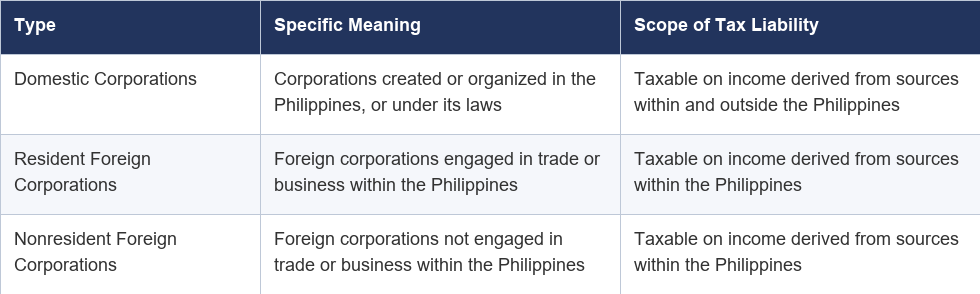

Corporate taxpayers can be classified into three categories: Domestic Corporations, Resident Foreign Corporations, and Nonresident Foreign Corporations.

Table 2: Types of Corporate Taxpayers and Scope of Taxation

The current standard corporate income tax rate is 25%. Domestic corporations meeting specific conditions, namely micro, small, and medium enterprises with an annual taxable income not exceeding PHP 5 million and total assets (excluding specific land) not exceeding PHP 100 million, can enjoy a preferential tax rate of 20%. Nonresident foreign corporations pay corporate income tax on their income derived from sources within the Philippines through a withholding system by the resident payor. Under the final withholding tax system, the amount of income tax withheld by the withholding agent constitutes the full and final amount of the income tax.

(1) Value Added Tax

Value Added Tax is a consumption tax levied on the sale of goods, provision of services (including digital asset services), or importation of goods within the Philippines, with a standard rate of 12%. Export sales and specific export of services are subject to a zero percent rate. Any individual or corporate entity whose gross annual sales exceed PHP 3 million must register as a VAT taxpayer.

(2) Percentage Tax

Percentage tax is mainly targeted at individuals or entities whose sale or lease of goods, properties, or provision of services in the course of trade or business are exempt from VAT, and who are not VAT-registered. Its tax rate is fixed at 3% of gross sales or gross receipts. This tax aims to simplify the tax burden for small-scale operators. It is generally filed and paid on a quarterly basis and is one of the most basic business turnover taxes in the Philippines.

(3) Excise Tax

It is mainly targeted at specific goods manufactured or produced in the Philippines for domestic sale or consumption, as well as imported goods. It is divided into specific tax based on weight or volume, and ad valorem tax based on selling price. It aims to achieve the dual purposes of increasing fiscal revenue and discouraging the consumption of specific goods.

(4) Documentary Stamp Tax

Documentary Stamp Tax is levied upon specific legal documents. The scope of taxation includes documents, instruments, loan agreements, and papers evidencing the acceptance, assignment, sale, or transfer of an obligation, right, or property. The taxpayers are the makers, signers, acceptors, or transferors of such documents.

Currently, the Philippines has not yet introduced specific tax laws for cryptocurrencies. Regarding the legal classification of cryptocurrencies, according to the guidelines on virtual asset service providers (Bangko Sentral ng Pilipinas Circular No. 1108, Guidelines for Virtual Asset Service Providers) issued by the Bureau of Internal Revenue (BIR) and the Bangko Sentral ng Pilipinas (BSP), the Philippines treats cryptocurrencies as property rather than currency. Therefore, the gains generated from the sale or exchange of cryptocurrencies can be taxed as ordinary assets or capital assets depending on their treatment. Regarding the valuation of cryptocurrencies, Section 40(A) of the NIRC stipulates that taxpayers use the fair market value as the basis for tax filing, meaning that crypto assets need to be converted into fiat currency at the fair market value on the date of the transaction for reporting purposes.

In tax practice, whether cryptocurrency gains are classified as ordinary assets or capital assets will directly impact the tax amount, making the distinction between the two particularly important. If classified as an ordinary asset, the gains are subject to the progressive personal income tax rates or the corporate income tax rate. When cryptocurrencies are used for investment purposes, such as being held as long-term investments, they are more likely to be classified as capital assets. If classified as capital assets, a capital gains tax rate of 15% applies.

Specifically regarding typical transaction scenarios of cryptocurrencies, under the Philippine tax system, a taxpayer merely holding cryptocurrencies will not incur any tax liability; other activities are taxed according to the following models:

(1) Mining: Cryptocurrencies acquired through mining are considered ordinary assets, and a tax liability arises immediately when the taxpayer acquires the cryptocurrencies. Taxpayers are generally required to recognize them as income at the fair market value on the date of receipt, and can deduct costs directly related to mining, such as electricity costs, hardware depreciation costs, and premises rental fees. Additionally, if it is only sporadic mining and not a commercial operation, rules regarding capital gains apply.

(2) Transfer: Cryptocurrencies transferred between different wallets or accounts under an individual's name do not incur taxes, as no transfer of ownership occurs and no value realization has taken place.

(3) Purchasing Cryptocurrency: Purchasing cryptocurrency using fiat currency purely constitutes an asset acquisition act under the Philippine tax system and does not trigger tax liabilities. However, buyers must retain accurate original records, because the purchase price at that time will constitute the cost basis for future disposal of the asset.

(4) Selling for Fiat Currency: Exchanging cryptocurrency for Philippine pesos or other fiat currencies generally constitutes an act of property disposition. The disposal gain is the portion of the realized amount that exceeds the tax basis, and its appreciated portion may need to be reported as capital gains.

(5) Crypto-to-Crypto Exchange: The exchange between cryptocurrencies is generally treated as a special barter transaction under Philippine tax law, meaning the disposal of the old coin and the purchase of the new coin occur simultaneously. According to Section 40(A) of the NIRC, the consideration received from the disposal of property includes not only cash but also the fair market value of the property received. Therefore, taxpayers must refer to the fair market value of the incoming currency on the day of exchange to determine the disposal value of the outgoing currency. For example, if Coin A, purchased for PHP 1,000, is exchanged for Coin B, which is worth PHP 2,000 at the time, a capital gain of PHP 1,000 must be reported.

(6) Purchasing Goods or Services: Using cryptocurrency to purchase goods or services is generally considered a barter act completed through the disposal of cryptocurrency. Taxpayers need to determine the fair market value of the goods or services received and treat it as the amount for which the cryptocurrency was sold, thereby calculating the disposal gain.

(7) Earning Cryptocurrency Compensation: Taxpayers acquiring cryptocurrency by providing services constitutes taxable income for this portion of the asset, which is generally reported for tax purposes as salary or service income based on the fair market value on the date the currency is received. For the payer, if it is a business expense, corresponding withholding tax obligations must also be fulfilled.

With the effective implementation of the Value-Added Tax on Digital Services Law (RA 12023), the Philippines has strengthened its supervision of offshore digital service providers (DSPs), emphasizing that Non-Philippine resident DSPs (NDSPs), like resident digital service providers, are required to pay a 12% digital services value-added tax and fulfill VAT registration and withholding obligations. Furthermore, the BIR requires all taxpayers involved in digital assets to maintain detailed transaction records for tax audit purposes, including proof of ownership, transaction dates, fair value records, and cost accounting vouchers. Crypto platforms providing goods or services online can be classified under the aforementioned regulatory scope and therefore must comply with the provisions regarding the retention of transaction records.

In addition to the Bureau of Internal Revenue regulating cryptocurrency activities from a tax administration perspective, the Bangko Sentral ng Pilipinas (BSP) and the Securities and Exchange Commission (SEC) also bear key responsibilities for cryptocurrency regulation. Furthermore, the Philippine government conducts Anti-Money Laundering (AML) and Combating the Financing of Terrorism (CFT) monitoring of cryptocurrency transactions through the Anti-Money Laundering Council (AMLC).

(1) Scope of Regulation: The jurisdiction focuses on payment and remittance services of cryptocurrencies. According to BSP Circular No. 1108, all institutions involved in fiat-to-crypto and crypto-to-fiat transactions, crypto asset exchange, transfer, custody, wallets, and related businesses are defined as Virtual Asset Service Providers (VASP). They are required to conduct activities within the VASP licensing framework and are included within the BSP's jurisdiction.

(2) Core Regulatory Requirements:

Must be registered as a domestic company in the Philippines and obtain a VASP license. Currently, the BSP is still in a Moratorium policy period, suspending the issuance of new VASP licenses. Although the regular application channel is closed, the BSP still allows licensed banks and financial institutions that meet compliance standards under the supervisory rating framework and are rated as stable to apply for a VASP license.

Minimum Capital Requirement: BSP Circular No. 1108 stipulates that the minimum capital for a VASP providing custody services is PHP 50 million; the minimum capital for a VASP not providing custody services is PHP 10 million.

Reporting and Due Diligence Obligations: Regularly submit transaction volume reports and audited financial statements, and execute customer due diligence for transactions exceeding PHP 5,000.

(1) Scope of Regulation: Primarily regulates cryptocurrencies with securities attributes. According to SEC Memorandum Circular No. 2025-05 (the SEC Guidelines on the Operations of Crypto-asset Service Providers, or CASP Regulatory Guidelines), institutions engaged in token issuance businesses with securities characteristics (such as investment contracts, tokenized securities), secondary market trading platform businesses, broker/dealer businesses, and custody of securitized tokens are defined as Crypto-Asset Service Providers (CASP), subject to the CASP institutional framework and regulated by the SEC.

(2) Core Regulatory Requirements:

Standards for Securities Identification: The SEC determines the nature of tokens based on economic substance, with the core standard being the Howey Test. It judges whether a cryptocurrency constitutes an investment contract based on whether there is an investment of money in a common enterprise with a reasonable expectation of profits to be derived from the efforts of others. If it constitutes an investment contract, securities registration is mandatory.

Dual Identity Requirement: Must be a locally registered company, and the primary purpose in the Articles of Incorporation must include CASP-related activities.

Capital Threshold Requirement: The company must have a paid-up capital of at least PHP 100 million. This capital can be held in cash or in kind, but excludes the valuation of crypto assets.

Asset Segregation Requirement: CASPs are strictly required to segregate customer assets from their own corporate funds both legally and physically.

Reporting Obligation Requirement: CASPs shall submit monthly financial statements, wallet address lists, board of directors' records, and compliance assessment reports.

Philippine crypto regulation has gradually moved from early pilot governance to a dual regulatory system functioning in parallel under the BSP and SEC. In February 2017, the BSP issued Circular No. 944, recognizing the legal status of cryptocurrency as a valid payment method and proposing regulatory guidelines for virtual currency exchanges for the first time. During this phase, the Philippines treated cryptocurrencies as payment instruments similar to remittance businesses, focusing on AML and KYC reviews. The resulting drawback was that regulation was mainly concentrated on the fund transfer process and failed to cover the securities attributes of cryptocurrencies and broader market risks.

With the scaling up of the crypto industry, the Philippine government realized that the traditional remittance business model could no longer cope with complex digital financial risks. In early 2021, the BSP issued Circular No. 1108 (Guidelines for Virtual Asset Service Providers), establishing a comprehensive regulatory framework for virtual asset service providers in the country. Concurrently, the circular imposed higher requirements for minimum capital and prudential management. To prevent systemic financial risks brought about by the barbaric growth of the industry, the BSP issued Memorandum No. 2022-035 in September 2022, announcing the suspension of new VASP license applications to integrate existing licensed institutions and weed out non-compliant entities over a three-year Moratorium policy. This policy was extended indefinitely by BSP Memorandum No. 2025-031.

From 2023 to the present, Philippine regulators began to strengthen local licensing supervision of cryptocurrency service providers and intensify crackdowns on illegal operating behaviors. In November 2023, the Philippine SEC called out Binance for operating related activities in the Philippines without local registration and without obtaining a securities sales license in the Philippines. It issued a ban prohibiting Binance from operating locally and required it to exit the Philippine market within three months. Citing Binance's lack of compliant licenses, the Philippine SEC also instructed competent authorities in March 2024 to block access to its website and App nationwide. On May 30, 2025, the Philippine SEC issued Memorandum No. 2025-05, clarifying the regulatory requirements for CASPs in the Philippines. In August 2025, ten exchanges including OKX and Bybit had actions taken against them by the SEC to restrict access because they operated or solicited investments in the Philippines without SEC permission. As the regulatory landscape of the Philippine crypto market continuously becomes clearer, market entry thresholds are further tightened, and a compliance license has become the foundation for crypto service institutions to establish themselves in this market.

Overall, the regulation of crypto assets in the Philippines has expanded to cover a comprehensive regulatory framework including platform access, customer due diligence, VAT on digital services, CASP rules, and international tax transparency. As the Philippine government signs the CARF framework and plans to fully implement it by 2028, the international coordination of the Philippines at the level of crypto asset taxation will be further strengthened. Taxpayers using crypto assets, whether local residents or offshore platforms, will face a more transparent crypto tax environment in the future. For market participants, the Philippines remains an important crypto market in Southeast Asia with an active user base. However, it is foreseeable that a series of regulatory requirements such as license applications, tax filings, and anti-money laundering reviews will ultimately become the key to entering this market in the future.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.