On February 26, 2026, Consensys-owned crypto wallet MetaMask announced a partnership with Mastercard, one of the world's biggest card networks, to launch the "self-custody" MetaMask Card in the United States. Users can now use this card for everyday shopping at over 150 million Mastercard-supported merchants worldwide. The best part? Users keep full control of their on-chain assets during the payment process—no need to pre-deposit funds into a centralized exchange account. Plus, they can earn cashback rewards in MetaMask's own stablecoin, mUSD.

The launch of the MetaMask Card has caused quite a stir in the crypto payment world. However, "crypto debit cards" aren't exactly a brand-new invention. Major exchanges like Coinbase and Binance have already rolled out cards that work with the Visa network for daily spending. So, what makes the MetaMask Card so innovative, and how will it shake up the market? We'll take a look at its features and compare it to other popular crypto payment methods to see the bigger picture.

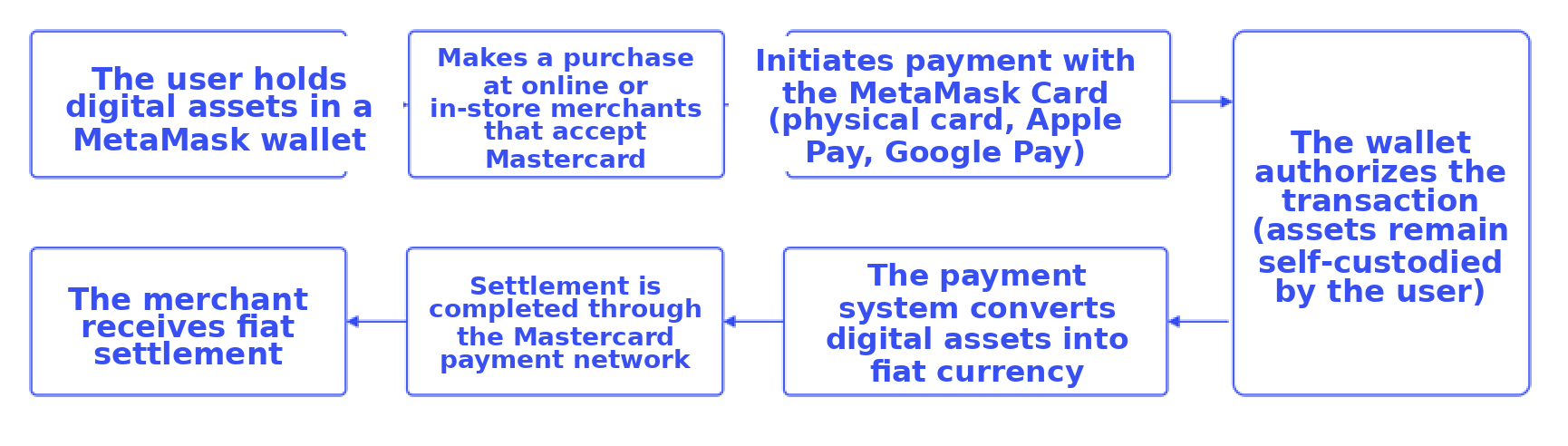

From a design standpoint, the MetaMask Card stands out because it isn't "custodial" like most other crypto cards that force you to move assets to a centralized platform first. Instead, you keep control of your wallet assets right up until the moment you pay. When a purchase happens, the authorization and clearing are handled through regulated infrastructure. The core idea isn't to force merchants to accept crypto on-chain, but to let users spend crypto assets they've authorized for the card's spending feature within the traditional card network. In short: the merchant sees a standard card payment, but the user gets more control than they ever had with traditional crypto debit cards.

According to official materials, this product has four main highlights:

First, Self-Custody: As mentioned, users stay in control of their crypto until they spend it, without needing to pre-load a centralized exchange account.

Second, Cashback Rewards: Every purchase earns on-chain rewards—up to 1% mUSD cashback for standard card spending, while physical cardholders get up to 3% mUSD cashback on their first $10,000 of annual spending.

Third, Global Network: Thanks to the Mastercard network, the card works at over 150 million online and offline merchants—covering everything from groceries and dining to travel and e-commerce. It's also compatible with Apple Pay and Google Pay.

Fourth, Instant Use: Once approved, users can quickly add the card to their mobile wallets and start spending online, in-apps, or in person.

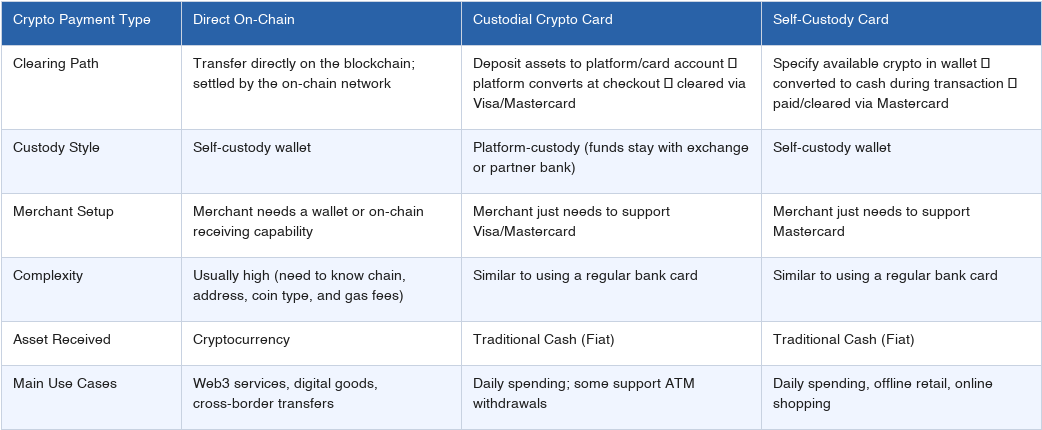

Crypto payment simply means using cryptocurrencies like Bitcoin, Ethereum, or USDT for transactions instead of traditional cash. Current crypto payment methods generally fall into three categories: Direct On-Chain Payments: Users send crypto directly to a merchant's wallet address. Custodial Crypto Cards: Users deposit assets onto a platform, which then handles the conversion to cash via networks like Visa or Mastercard. Self-Custody Wallets Linked to Card Networks: This is what MetaMask Card does. It aims to keep the "self-custody" vibe while giving users an experience that feels almost identical to using a regular bank card. This model shows how crypto tools are blending into real-world spending and highlights how Web3 wallets are becoming the go-to hub for managing digital assets, moving away from the old exchange-centric model.

The rise of PayFi (Payment Finance) has pushed crypto from just being a way to move value on-chain to something you can use for real-world shopping. Stablecoins paired with on-chain payment tools are showing serious speed and cost advantages for things like global remittances and instant settlement. Against this backdrop, there are four big reasons why MetaMask Card is moving from pilot to full rollout:

First, the pilot phase was a success. Following a 2025 pilot at ETHDenver, MetaMask has seen the card used for everything from coffee to big-ticket items across multiple markets. Launching across the entire US shows the product is ready for the big leagues.

Second, the market is ready for this product logic. Unlike traditional cards, the MetaMask Card lets users keep control of their money until they swipe. This design hits the sweet spot for crypto users who want the security of self-custody without sacrificing the convenience of a bank card.

Third, infrastructure and regulation have changed for the better. Over the past year, the US has clarified its rules for stablecoins and banks involved in crypto. The GENIUS Act created a federal framework for payment stablecoins, and the FDIC cleared the way for regulated institutions to engage in low-risk crypto activities. These clear rules actually help the market run more smoothly by defining the "red lines" for everyone.

Finally, it's a win-win for both partners. MetaMask needs to make wallet assets usable in the real world, and Mastercard wants to capture the growing crypto payment market.

If crypto payments remain "high-interest but low-use," they'll never go mainstream. A 2026 survey by GoMining found that while 80% of crypto holders want wider adoption, only 12% actually use crypto for daily shopping. The MetaMask Card pushes a trend: combining on-chain assets with regulated payment networks to make it easier for everyone to use. Mastercard isn't alone here; Visa recently announced plans to expand stablecoin-linked cards to over 100 countries, showing that the giants are all moving in this direction.

Most crypto payments used to rely on centralized custody, which puts a lot of risk on the platform (like fund mismanagement or hacks). By using a self-custody model, the MetaMask Card lets users keep the keys to their assets, cutting those centralized risks out at the root. Also, MetaMask uses different conversion rates for different assets, effectively baking the risk of volatility into the fees. This helps the industry move toward a model where the price of payment matches the actual risk involved.

The MetaMask Card works by embedding traditional compliance—like KYC (Know Your Customer) and AML (Anti-Money Laundering)—directly into the crypto payment process. This sets a standard for other crypto projects to follow. Future competition in crypto payments won't just be about tech or fees; it'll be about who has the best compliance setup. However, with global regulations still being quite fragmented, these projects will need to find a way to balance global compliance with local operations.

The MetaMask Card isn't the first crypto card, but it's a very important new example. When self-custody wallets stop being just for storing coins and start connecting to real-world shops through regulated networks, the conversation shifts from "Can we pay with this?" to "How do we balance control, usability, and compliance?" That is exactly why this card is worth watching.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.