Over the past year, crypto spot ETFs have launched in several markets, making the link between crypto assets and the traditional financial system much more direct. According to Japanese media reports, the Financial Services Agency (FSA) plans to revise the Cabinet Order (Enforcement Order) underenforcement orders of the Act on Investment Trusts and Investment Corporations (Investment Trust Act) to include crypto assets in the category of "specific assets" that investment trusts are allowed to invest in. The FSA expects to submit this bill to the Diet as early as 2026. If it passes, crypto spot ETF products could start trading in Japan by 2028. The market size is expected to reach trillions of yen, which would push brokerages and exchanges to roll out supporting services. However, back in April last year, in an FSA discussion paper titled "Examination of the Regulatory Systems Related to Cryptoassets" (hereinafter referred to as the "Discussion Paper"), the agency clearly stated that ETFs primarily investing in crypto assets could not be established under the current legal framework. Now, as regulatory talks progress, the FSA's policy direction is showing new signals of change.

What do these changes tell us about Japan’s current regulatory direction? What hurdles does Japan still need to clear before launching crypto spot ETF trading, and how will market opportunities and compliance requirements evolve together? This article uses Japan’s push for crypto spot ETFs as a starting point to explain how these products work and how they differ from futures-based products. We will also track the regulatory shifts seen in the Discussion Paper and recent moves, and analyze how this policy evolution will affect Japan’s crypto ecosystem, the business plans of financial institutions, and investor protection.

ETP (Exchange Traded Product) is a broad term for products traded on an exchange, and ETF (Exchange Traded Funds) is the most popular type that works like a fund. In different regions, the legal name for crypto spot products might not always be "ETF," but because the trading experience and investor perception are so similar, the market generally calls them "crypto spot ETFs." Put simply, a crypto spot ETF is a product backed by actual crypto assets, giving investors exposure through the "spot" (real) assets. These products make trading and holding crypto much more convenient, but they don't get rid of risks like price swings, fraud, or market manipulation. When investors move from managing their own digital wallets to using exchange-traded products, the type of risk they face changes, but the biggest factor remains the price volatility itself.

To understand a crypto spot ETF, you have to look at it as a complete chain. First is Underlying Assets and Valuation: products usually calculate their net asset value (NAV) based on spot market prices or specific indices. How often the NAV is calculated, where the price data comes from, and how things are handled during extreme market moves all affect how well the fund tracks the price and the overall investor experience. Second is Custody: the actual assets behind a crypto spot ETF must be kept in a compliant storage system. Keeping private keys safe, using cold storage, managing access, and having regular audits are the core of risk control, usually handled by regulated custodians. Third is the Creation/Redemption and Authorized Participant (AP) Mechanism: Authorized Participants trade between the primary market (where shares are created/redeemed) and the secondary market (the exchange) to profit from price differences. This helps keep the ETF price close to its actual value and affects liquidity. When market swings get wild, these price gaps and trading frictions can get bigger. Fourth is Trading Costs: trading these ETFs involves looking at the "spread" (the gap between buy and sell prices), the impact your trade has on the price, and how taxes are handled in different markets.

In the investment world, crypto products on exchanges are usually grouped by what they actually hold. The most common are Spot ETFs and Futures ETFs. Spot Bitcoin or Ethereum ETFs usually hold the actual crypto assets to track their price, while Futures ETFs hold futures contracts based on those assets.

A Spot ETF is an open-ended fund or similar product listed on an exchange. It creates and redeems shares through "authorized participants." To track a specific price, it builds a portfolio by directly holding and storing the actual spot assets and calculates the fund's value based on the fair market price of those assets. A Spot ETF can hold just one asset (like BTC or ETH) or a "basket" of multiple assets to spread out the risk. Spot ETFs are great for investors who want to track crypto prices within a regular brokerage account without having to deal with digital wallets or private keys, though the price swings of the assets will still directly impact the fund's value.

A Futures ETF uses crypto futures contracts as its main investment tool. These ETFs issue shares that investors can buy and sell to gain exposure to the price changes of, for example, Bitcoin futures. Because these contracts expire and have to be "rolled over" to the next month, investors need to watch out for the risk of the fund's value drifting away from the actual crypto price due to these rollover costs. Before spot products were approved in the U.S., the ProShares Bitcoin Strategy ETF was already available.

Besides being split into spot and futures types, these products can also be categorized by what they track (a single asset vs. an index/basket) or by the type of underlying asset (pure crypto vs. stocks related to the industry, like mining companies). There are also Leveraged, Inverse, and Strategy-based products. These have more complex goals and rebalancing rules (often resetting daily), which means they are more sensitive to the path the price takes and are usually meant for a smaller group of experienced investors.

The positive signals the FSA is currently sending regarding crypto spot ETFs are a sharp contrast to its previous cautious and conservative approach. This nearly 180-degree turn is driven both by changes in the local market and pressure from international competition.

Looking at Japan's domestic market, previous regulations focused more on the "payment" side of crypto—things like exchange compliance, managing customer assets, and monitoring price swings. Since 2025, Japan has launched a series of policy updates to move crypto from the fringes of "payment methods" into the financial mainstream. In terms of legal status, on December 10, 2025, the FSA proposed last December to move crypto regulation from the Payment Services Act (PSA) to the Financial Instruments and Exchange Act (FIEA). This treats crypto as a financial product and gives it a legal status closer to traditional securities. On the tax side, Japan released a 2026 tax reform plan late last year, aiming to change the tax on crypto gains from a high 55% "miscellaneous income" tax to a flat 20% "separate tax." These current and potential policy changes create the foundation for treating crypto as a financial commodity, paving the way for spot ETFs.

Secondly, international competition and the need to match global standards are big drivers. Once spot Bitcoin products hit the mainstream in the U.S., institutional interest and compliance services grew fast. For Japan, this isn't just about giving investors more options; it’s about the competitiveness of its financial center. If Japan stays away from regulated products for too long, high-quality capital and services will move elsewhere, and domestic banks and firms will miss the chance to gain experience in a safe, regulated environment.

Finally, the FSA’s previous "no" in the Discussion Paper didn't mean they were against the idea forever; it just meant it wasn't doable under the rules at that time. As the market and regulatory landscape change, there is plenty of room to adjust. The Discussion Paper acknowledged that crypto has shown strong "investment" qualities in the real world and that it is necessary to build the right regulatory tools for it. Based on this, the paper suggested two ways to regulate assets: First, "Financing-type crypto assets," which are tokens used for fundraising or have a specific utility. Here, regulation focuses on making sure the issuer discloses how the money is used and how the project is going. Second, "Non-financing-type crypto assets," like BTC and ETH. Since there is no single company "issuing" them, the focus shifts to making sure the actual trading is fair.

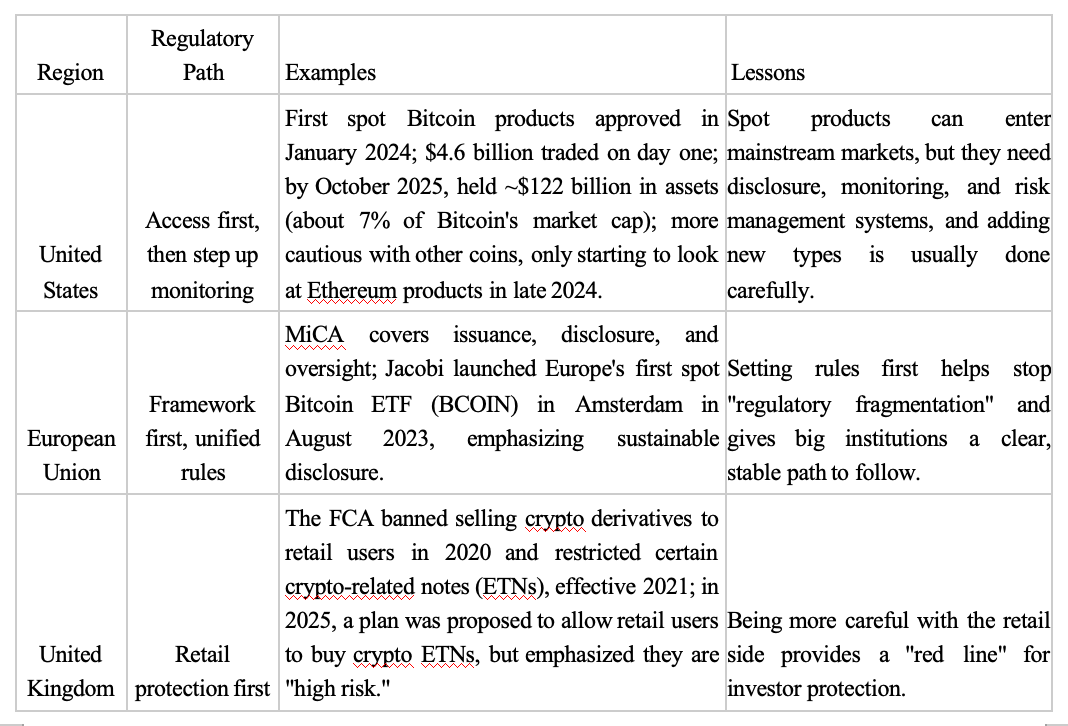

Looking at global experience, the U.S., EU, and UK represent three different paths. The U.S. allowed spot products into the mainstream while stepping up rules on disclosure and market monitoring. The EU focused on building a framework first (MiCA) to reduce "regulatory shopping" (where firms pick the easiest rules). The UK has long focused on protecting regular (retail) investors by first limiting access to high-risk products and then discussing where to draw the line under stricter rules. By weighing these three paths, Japan might take a middle ground: introducing regulated products while stepping up requirements for disclosure, suitability (making sure the product fits the client), and anti-fraud measures to keep investors safe.

Japan’s crypto market has grown significantly lately. As of July 2025, there are about 13.2 million crypto trading accounts. While that’s fewer than regular stock accounts, there is still room to grow. The value of crypto assets held by investors hit about 5 trillion yen in July 2025, and though it dipped to 4.9 trillion in September due to price swings, the trend is generally upward. This shows may reflect that with inflation rising faster than incomes, people are getting more interested in "risk assets." At the same time, questions and complaints are up. FSA data shows 1,304 crypto-related inquiries/complaints in the last quarter of 2024, higher than previous levels. Regulators are under pressure to provide safe ways to participate while keeping an eye on investor protection and financial safety.

If crypto spot ETFs are approved in Japan, the most immediate effect will be a shift in where the money comes from. In this scenario, some money that used to go directly to crypto exchanges might move into products within the regular brokerage system. Local crypto exchanges might feel the pressure as retail trading and existing assets get diverted.

For traditional financial institutions, the launch of crypto spot ETFs is both a chance to innovate and a "stress test" for their reputation and compliance. Given how much crypto prices swing, if a product launches and then crashes quickly, everyone will look closely at whether the risks were explained well, if the sales process was legal, and if the product actually fit the customer’s risk level. Since regulators are very focused on stopping "fraudulent solicitation" and ensuring safe operations, an institution's ability to control internal risks will be the main hurdle for getting involved.

As for investors, global wealth managers, family offices, and hedge funds looking for opportunities in Asia will be watching Japan's progress closely. If Japan allows these ETFs, it creates a new, regulated "entry point" in a mature capital market. This makes it much easier for them to add crypto to their portfolios: the products can be bought and sold via brokerage accounts, reports and disclosures are standardized, storage is handled by regulated firms, and getting internal legal approval becomes much simpler.

Japan’s push for crypto spot ETFs signals a clear intent to bring crypto assets further into the regulated financial mainstream, suggesting that Japan’s crypto market is entering a new phase where institutionalization and standardization deepen, and where competition over existing market share coexists with the introduction of new inflows. However, moving from a policy blueprint to actual market launch still requires Japan to clear several hurdles. And in today’s highly interconnected capital markets, shifts in external regulatory environments will remain an important variable.

Over the long run, crypto spot ETFs are not only a conduit connecting fiat capital and crypto assets, but also a stress test of Japanese financial institutions’ compliance capabilities and risk-control systems. Only if rulemaking stays ahead of risk build-up can Japan establish a crypto trading hub that is both safe and competitive.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.