On March 9, 2026, the UK Treasury released the Individual Savings Account (Amendment) Regulations 2026 (SI 2026/248), which updated the access rules for different types of assets under the ISA framework. This amendment officially clarifies at the legislative level that cryptoasset exchange traded notes (cETNs) can now be considered "qualifying investments" and enjoy tax benefits; at the same time, it limits them to the Innovative Finance ISA (IFISA) category. While this setup technically allows cETNs to enjoy tax breaks within the ISA framework, there might be quite a few hurdles in actually making this happen. For instance, the high compliance bar for Innovative Finance ISAs might make it harder for cETNs to become popular among everyday investors. In this context, it is worth looking closer at whether cETNs have truly gained a foot in the door or if they are effectively being pushed to the sidelines. This article will break down the core details of these new ISA rules, look back at how the regulation of cETNs has evolved, and analyze the real-world impact based on market structure and regulatory logic.

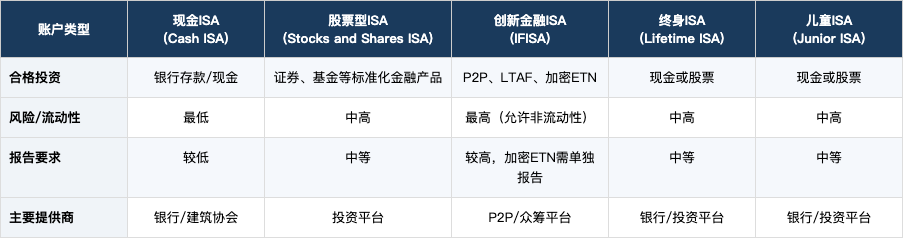

To encourage people to save and invest, the UK government launched a tax-advantaged tool in 1999 called the Individual Savings Account (ISA). Investors can open ISA accounts through investment platforms, brokers, or banks, and hold various financial assets inside. Any investment gains made within the account are tax-free. Based on the risk profile of the products and regulatory requirements, ISA accounts are divided into different types. These accounts differ in terms of the types of eligible products, risk or liquidity, regulatory reporting requirements, and the types of providers allowed to offer them.

Cash ISAs mainly deal with low-risk assets like bank deposits or cash, which are very liquid. Stocks and Shares ISAs cover medium to high-risk standard financial assets, including stocks, funds, and ETFs, where values fluctuate with the market, offering higher potential returns but also the risk of prices dropping. Innovative Finance ISAs carry more complex or higher-risk investment tools, such as P2P loans, Long-Term Asset Funds (LTAFs), and cETNs. These products are often less liquid and might not be protected by the Financial Services Compensation Scheme (FSCS), making them the highest risk overall.

All ISA types require the financial institutions providing them to submit annual reports to HM Revenue and Customs (HMRC). These reports include details like subscription amounts, transfers in and out, and holding summaries to ensure tax benefits are applied correctly. This reporting duty is mostly the same across all ISAs. According to the 2026 amendment, cETNs must be reported as a separate category. Additionally, these financial institutions have a duty to report information to the Financial Conduct Authority (FCA). Cash ISAs usually only involve deposit assets and do not typically require complex suitability assessments or detailed disclosures, so their reporting needs are relatively low. For Stocks and Shares ISAs, platforms must follow general FCA rules regarding investment suitability and disclosure because they involve securities. Lifetime ISAs have to handle extra records for government bonus payments, and Junior ISAs require careful management of guardian information. Because IFISA products are riskier, platforms often have to deal with stricter ongoing monitoring, suitability assessments, capital requirements, and specific disclosure duties. Generally, the reporting gets more complicated as the product risk goes up.

Originally, cETNs were not specifically defined in the Individual Savings Account Regulations 1998, and there were no specific restrictions on them. As debt securities issued by companies and traded on a UK Recognised Investment Exchange (RIE), cETNs met the requirements of "qualifying securities" under Section 7(2)(b) of those regulations. They were usually lumped into the broad category of securities for Stocks and Shares ISAs, enjoying the same tax perks as traditional securities. However, in reality, retail clients could not actually invest in cETNs within an ISA because of the FCA retail ban. Starting January 6, 2021, the FCA banned UK-regulated firms from selling, marketing, or distributing any derivatives or exchange traded notes linked to "unregulated transferable cryptoassets" to retail investors, which included cETNs. This meant that retail investors could not actually buy cETNs on ISA platforms or put them into a Stocks and Shares ISA.

The restrictions on Crypto ETN investments hit a turning point on October 8, 2025. On that day, the FCA officially lifted the sales ban, allowing retail investors to trade Crypto ETN products through an RIE. However, it classified them as Restricted Mass Market Investments (RMMI), meaning they must follow consumer protection rules like risk warnings and suitability assessments. On the same day, HMRC released the "Tax treatment of cryptoasset Exchange Traded Notes policy," making it clear that eligible cETNs could be included in registered pension accounts and held tax-free starting immediately, and would be categorized under the Innovative Finance ISA (IFISA) for tax benefits starting April 6, 2026. These policy arrangements were eventually turned into formal, legally binding rules through the SI 2026/248 regulation, putting HMRC core plan for Crypto ETN account classification into action and setting clear transition arrangements for cETNs held in the past.

Before SI 2026/248 came out, as long as an investment tool looked like a "transferable security" in legal terms, it could be included in a Stocks and Shares ISA. Under that setup, cETNs automatically fell into the "qualifying securities" category, making them technically eligible for Stocks and Shares ISAs. This amendment makes a major change to that structure and stops using that broad classification. First, it creates a specific definition for cETNs to separate them from the general "qualifying securities" category. Second, it explicitly states that cETNs are no longer allowed in Stocks and Shares ISAs. Finally, it limits them to being eligible investments only for Innovative Finance ISAs, making the classification crystal clear.

SI 2026/248 highlights the core features of a Crypto ETN: first, it must be a financial instrument traded on a UK RIE, giving it the status of a publicly traded product. Second, it is defined as a debt security without regular interest payments; the returns do not come from a fixed interest rate but depend on the price performance of a specific underlying asset. Third, its return structure is clearly pegged to "unregulated transferable cryptoassets," which sets it apart from exchange traded products backed by traditional financial assets. Fourth, the legal definition does not limit the type of risk exposure, covering various structures like delta-1, inverse, or leveraged setups. By confirming that cETNs are securities while separating them from general securities in the rules, this definition provides the necessary foundation for different access rules within the ISA system.

An ISA manager is a financial institution, like a bank or a brokerage, approved by HMRC to set up, run, and manage ISA accounts. While this amendment did not roll out a bunch of brand-new standalone duties for managers, the changes to Crypto ETN rules indirectly add new compliance burdens, mostly regarding business qualifications and reporting. In terms of qualifications, only managers with the authorization to run Innovative Finance ISAs can offer Crypto ETN products within the ISA framework. This is not a separate financial license, but a specific type of account authorization within the ISA manager approval system. Therefore, this revision essentially places a new requirement on managers: those who only handle Stocks and Shares ISAs cannot continue to offer Crypto ETN products unless they get IFISA authorization. If they want to keep that business going, they need to apply for approval and adjust their business models and account systems. Regarding reporting, the new rules beef up the duties for ISA managers. First, they amend Regulation 31 of the original rules; on top of the annual returns of information, cETNs are now listed as a special investment type that needs to be identified and reported separately. The info to be reported includes the market value and the amount of cash held, so HMRC can track the scale, valuation, and risk exposure of Crypto ETN holdings. Second, systems must be able to recognize cETNs as an asset class, ensure they are correctly placed in IFISA accounts, and report them separately in the format specified by HMRC.

Because the underlying assets of cETNs are so volatile, complex, and lack transparent information, they carry higher risks than traditional stocks, bonds, or funds. By stripping cETNs out of Stocks and Shares ISAs and putting them into IFISA accounts, the new ISA rules keep the door open for investors to get tax breaks while keeping high-risk assets in a specific account designed to handle that risk. This shows that regulators want to manage different assets by matching risk levels with specific account functions. Furthermore, when the FCA lifted the Crypto ETN retail ban in late 2025, the UK Treasury did not shove cETNs into IFISAs immediately. Instead, they provided a transition period, allowing those who already held cETNs in a Stocks and Shares ISA before April 6, 2026, to keep holding them there without moving them to an IFISA. Setting this six-month transition window gave platforms time to get their tech ready and helped investors get used to the new rules.

For ISA managers, the new rules mean they have to get IFISA permissions to do Crypto ETN business. They also need to redesign their account categories and product management workflows and upgrade their systems to support things like separate identification, valuation, and reporting for cETNs. Even though the new rules legally put cETNs into IFISAs with tax benefits and provide a clearer framework, the reality is that there are not many IFISA managers. Combined with a lack of platform experience, high operating costs, and compliance pressure, running an IFISA Crypto ETN business brings both cost concerns and reputation risks.

For cETNs issuers, the most direct hit is a shrinking retail distribution channel. Before, the Stocks and Shares ISA was seen as a major gateway for Crypto ETN growth. Under the new rules, if there are not enough IFISA managers willing to take on the business, the scale of retail distribution for issuers might get squeezed. Next is the shift in liquidity expectations; because retail demand might slow down, secondary market activity could weaken, affecting overall trading volume. Issuers will need to rethink market liquidity and try to stay competitive by optimizing indexes or adjusting fees.

For everyday investors, the new rules limit cETNs to IFISA accounts, which technically boosts protection for those buying high-risk assets, but it might actually make them harder to get. Right now, because there are so few managers who have IFISA status and actually want to offer cETNs, it is harder for regular investors to start holding new cETNs within the ISA system. Also, the current transition plans are a bit vague on what happens next with existing holdings. According to the new rules, cETNs put into a Stocks and Shares ISA before April 6, 2026, can stay there, but there are not detailed rules on how to handle future trades, conversions, or moving accounts. For example, it is unclear if investors can keep buying more in their original accounts or what the specific steps are for moving between different managers.

The rollout of the SI 2026/248 regulation marks the official legalization of the UK strategy to manage Crypto ETN risks differently within the ISA framework. By putting cETNs into the Innovative Finance ISA (IFISA), this revision keeps a tax-free investment path open for retail investors while isolating the systemic risks of cETNs through account classification. It shows the regulators are trying to balance financial innovation with stronger consumer protection. However, as mentioned before, the limited supply of IFISA managers might slow down the spread of cETNs in the ISA system for a while. This just shows that there is still some work to be done to align policy design with market reality.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.