On 13 February, Esperanza Securities received approval from the Securities and Futures Commission (SFC) of Hong Kong to conduct entertainment-asset tokenisation based on the box-office revenue rights of Christopher Wong’s 40th anniversary concert at the Hong Kong Coliseum. On 24 February, the RWA real-estate project for DL Tower under DL Holdings was approved for issuance. At the start of 2026, high-quality commercial real estate in Hong Kong’s core Central district, together with concert tickets and revenue rights tied to the iconic Hong Kong Coliseum - long seen as a benchmark of Asian pop culture - were brought on-chain in quick succession, becoming among the first RWA projects launched in Hong Kong within their respective sectors. This signals that RWA (real-world assets) is moving beyond the proof-of-concept (PoC) stage and gradually entering a new phase of commercial and scaled deployment.

Hong Kong is becoming a major global hub for RWA assets by leveraging its unique “One Country, Two Systems” advantage, well-established common law system, and forward-looking regulatory framework. Compared with traditional lending and IPOs, issuing RWA products in Hong Kong is not only a strategic way to broaden financing channels and reduce funding costs, but also an important path toward global pricing and liquidity release for underlying assets. Yet financial innovation often comes with complex legal, tax, and compliance risks. RWA is not simply old wine in a new bottle. It requires issuers to build a robust compliance framework across multiple dimensions, including look-through analysis of underlying assets, smart-contract audits, cross-border data compliance, and anti-money laundering (AML). From a professional perspective, this article systematically reviews the evolution and mainstream structures of RWA in Hong Kong, examines the related tax implications and regulatory logic, and looks at the compliance risks behind the financing upside of RWA.

Looking back at the development of RWA in Hong Kong, one can clearly see an evolutionary path extending from standardised financial products to a broader range of real-world assets. This reflects not only the deepening integration of blockchain technology and financial engineering, but also the prudent and progressive regulatory approach adopted by Hong Kong regulators.

RWA in Hong Kong did not begin as a grassroots market initiative. It was driven from the top down by the government. In February 2023, the HKSAR Government successfully issued HK$800 million of tokenised green bonds under Project Evergreen, among the first tokenised green bonds issued by a government anywhere in the world (HKMA, 2023). This stage was characterised by highly standardised underlying assets (bonds), strong credit quality (sovereign credit), and a restricted investor base (institutional investors only). Its core objective was to test whether distributed ledger technology (DLT) could improve efficiency and reduce costs in traditional financial market infrastructure, such as clearing and settlement.

Following the initial validation of infrastructure, the SFC issued multiple circulars, including the Circular on intermediaries engaging in tokenised securities-related activities and the Circular on tokenisation of SFC-authorised investment products (SFC, 2023a; SFC, 2023b). The market then began shifting its focus toward yield-bearing assets such as private credit and money market funds, including tokenised U.S. Treasuries. At this stage, RWA acted as a bridge between Web3 capital and traditional yield-bearing U.S. dollar assets, opening up an on-chain route for capturing the risk-free rate.

At the beginning of 2026, Hong Kong’s first real-estate and entertainment RWA projects were cleared by the SFC, further expanding the range of RWA use cases in the city. Commercial real estate typically involves high capital thresholds and low liquidity. After fractionalisation through RWA structures, professional investors can participate in the investment and income distribution of such assets at a relatively lower entry threshold. At the same time, entertainment assets such as concerts and film copyrights often generate cash flows that are cyclical and uncertain. Putting box-office revenue rights on-chain effectively combines consumption with investment. Fans become not only consumers but also ecosystem investors. This dual “finance + consumption” attribute significantly broadens pre-funding channels for the entertainment industry.

Overall, the core commercial value of RWA has already moved beyond improving payment and settlement efficiency and is increasingly centred on unlocking liquidity premiums. Assets that are relatively illiquid and difficult to split within traditional finance often have more visible upside under an RWA framework.

In February 2026, DL Holdings (1709.HK) disclosed its plan to tokenise interests in a limited partnership fund holding a commercial property in Central, Hong Kong. The plan received a “no further comment” regulatory acknowledgement from the SFC and may be distributed by licensed intermediaries to qualified professional investors (PIs). As a model of integration between traditional commercial real estate and digital finance, projects of this kind generally follow the steps below:

1. Asset carve-out and SPV setup: The issuer first establishes a special purpose vehicle (SPV) in Hong Kong or offshore and lawfully transfers the title to, or income rights over, the commercial property into the SPV. The core purpose of this step is to isolate the asset from the credit risk of the developer’s parent company.

2. Third-party due diligence and valuation: Professional firms are engaged to conduct financial and legal due diligence on the SPV and its underlying property, while an independent valuer issues a valuation report so that the token pricing has a fair basis.

3. Oracle design: The value of commercial property and rental income arise off-chain. The project therefore needs a reliable oracle mechanism to synchronise real-world rental cash flows, updated valuations, and other data onto the blockchain on a periodic basis, so that token holders can access accurate information.

4. Smart-contract development and audit: The income distribution logic of the asset (for example, quarterly rental distributions) and transfer restrictions (for example, trading limited to Hong Kong-compliant PIs) are coded into the smart contract. Before deployment, the contract must undergo a security audit in accordance with applicable requirements.

5. Token minting and issuance: Security tokens representing equity or debt interests in the SPV are minted on Ethereum or another public or consortium chain. Each token represents a specific proportional share of the fund’s economic rights and voting rights.

6. Distribution by licensed intermediaries and secondary trading: The tokens are underwritten and distributed through financial institutions in Hong Kong that hold Type 1 (dealing in securities) and Type 4 (advising on securities) licences and have been approved by the SFC to conduct virtual asset-related business. In the future, they may circulate on compliant virtual asset trading platforms (VATPs) in the secondary market.

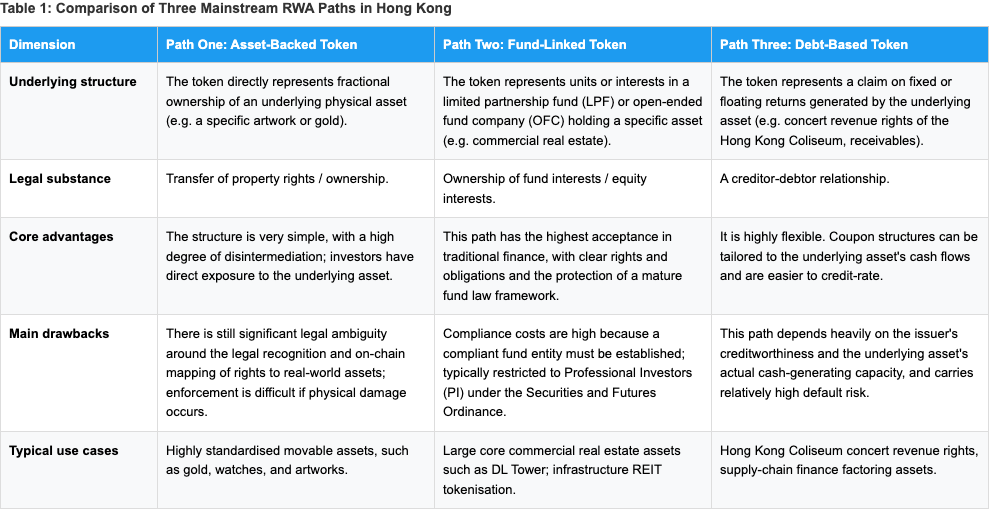

Based on the nature of the underlying asset and the legal structure used, RWA projects in Hong Kong currently fall into three main paths. Each path has different compliance and tax implications.

For a clearer comparison, the table below breaks them down side by side:

The SFC’s regulatory approach to RWA can be summarised in eight Chinese characters: “same business, same risks, same rules.” In other words, regulators will not relax oversight simply because an asset has put on the blockchain’s “new coat.” Instead, they apply a look-through approach aimed directly at the economic substance of the underlying asset.

First, at the asset-classification level, according to the SFC’s Circular on tokenisation of SFC-authorised investment products issued in November 2023, if the underlying asset of an RWA product consists of traditional shares, bonds, or fund interests, the corresponding token will generally be classified as a “tokenised security.” In principle, the issuance of such products remains subject to the issuance, disclosure, and licensing requirements applicable to traditional securities under Hong Kong’s Securities and Futures Ordinance.

Second, for non-standard assets, if the tokenisation structure embeds complex derivative logic or special transfer restrictions, the SFC tends to regard the product as a “complex product.” This means the distributing intermediary, such as a broker or bank, must conduct suitability assessments when recommending the product to clients, and subscription is generally limited to professional investors, including individual professional investors with liquid portfolios of at least HK$8 million.

At the technical and operational compliance level, regulators generally require issuers to subject smart contracts to independent third-party audits in order to mitigate asset risks arising from code vulnerabilities or cyberattacks at the source. At the same time, on the AML side, issuers and virtual asset trading platforms must fully implement KYC procedures and strictly comply with the Travel Rule so that the identities of both the sender and the recipient of every on-chain transaction remain transparent and traceable.

This path mainly involves profits tax. If an issuer directly sells tokens representing local physical assets in Hong Kong, such as machinery or equipment, the transaction may be regarded as a sale arising in Hong Kong. Under the Inland Revenue Ordinance, the resulting profits would generally be subject to profits tax at the standard rate of 15% or 16.5%, depending on the type of entity involved.

At both the fund level and the token level, the tax treatment is more complex. Under the Hong Kong Stamp Duty Ordinance, for transfers of shares in an unlisted SPV (or other Hong Kong securities), ad valorem stamp duty of 0.1% is generally payable by each of the buyer and the seller. When fund interests are circulated in tokenised form, an on-chain transfer of the token may constitute a “transfer of Hong Kong securities” as a matter of law, and may therefore trigger 0.1% stamp duty. In addition, where the relevant fund satisfies the conditions of the Unified Fund Exemption (UFE) regime, profits derived from qualifying transactions may be exempt from profits tax, thereby allowing for tax optimisation.

The tax treatment under this path turns on how investor income is characterised, particularly whether the return is treated as interest income. Using an entertainment-related RWA project as an example, distributions received by investors holding tokens linked to concert revenue rights would, in substance, generally be characterised as interest income for tax purposes. If the investor is a Hong Kong entity, it is necessary to assess whether the interest is sourced from Hong Kong in order to determine whether it falls within the profits tax net. If the investor is an individual, Hong Kong’s current tax system generally does not impose tax on personal interest income.

RWA does not exist in a vacuum. Its growth is closely tied to macro-policy support. To understand the current boom in issuing RWA products through Hong Kong, one must place it in the broader context of regulatory divergence between Mainland China and Hong Kong, as well as the global upgrading of financial market infrastructure.

Mainland China has consistently maintained clear regulatory red lines against the issuance, trading, and financing of virtual currencies. Policy attention remains focused on the use of technology to empower industry and on the promotion of central bank digital currency (CBDC). The Notice on Further Preventing and Handling Risks Related to Virtual Currencies and Similar Matters, issued on 6 February 2026, further clarified the regulatory stance toward RWA: conducting real-world asset tokenisation activities within the territory, as well as providing related intermediary or information technology services, may constitute illegal issuance of tokenised instruments, unauthorised public offering of securities, illegal securities or futures business, illegal fundraising, or other illegal financial activities, and should therefore be prohibited, except where the relevant activities are carried out through specific financial infrastructure with approval in accordance with law and regulation from the competent authorities. Shortly thereafter, the CSRC issued the Regulatory Guidelines on the Overseas Issuance of Asset-Backed Securities Tokens Based on Domestic Assets (CSRC Announcement [2026] No. 1), establishing a dedicated regulatory framework for token issuance overseas where domestic assets are securitised. Taken together, these developments reflect a policy approach of “strict prohibition onshore, strict regulation offshore”: while RWA activities remain prohibited in Mainland China, a limited channel has been left open for the compliant offshore issuance of tokenised products backed by domestic assets.

Since the release of the Policy Statement on Development of Virtual Assets in Hong Kong in 2022, Hong Kong has built one of the clearest and most innovation-friendly policy environments for RWA globally. In November 2023, the SFC issued the Circular on intermediaries engaging in tokenised securities-related activities and the Circular on tokenisation of SFC-authorised investment products, laying down the regulatory tone for RWA in Hong Kong. In 2024, the Hong Kong Monetary Authority (HKMA) launched the Project Ensemble Sandbox, focusing on the testing of tokenised money for interbank settlement in institutional RWA settlement scenarios and helping to build financial infrastructure that connects tokenised money with tokenised assets in Hong Kong. In August 2025, the Stablecoins Ordinance came into effect, creating a dedicated licensing regime for issuers of stablecoins pegged to fiat currency. Stablecoins provide a compliant pricing anchor and payment instrument for RWA transactions, and the Ordinance helps further remove practical frictions in the tokenisation of real-world assets.

Faced with the financing opportunities created by RWA, project sponsors cannot stop at the level of narrative excitement when issuing through Hong Kong. A complete compliance framework must be built in parallel.

General compliance: First, the authenticity and independence of the asset structure matter. In designing entertainment revenue-rights or real-estate RWA products, if an issuer promises fixed returns in the name of a token while failing to achieve genuine asset isolation at the underlying level, the structure may easily be characterised under Hong Kong’s regulatory framework as illegal fundraising or an unauthorised collective investment scheme. For this reason, it is advisable to introduce an independent third-party asset custodian to reduce the risks associated with pooled-fund operations and implicit guarantees. Second, AML constraints on-chain are hard requirements. To satisfy AML obligations, project sponsors need an operational framework covering customer due diligence, wallet address screening, transaction monitoring, and suspicious activity detection.

Tax compliance: First, the legal nature of the token affects the tax analysis and calls for careful tax planning. When reviewing token transactions, the Hong Kong Inland Revenue Department may look through the technical shell of the smart contract and focus directly on the economic substance of the arrangement. Whether the token represents a property right, an equity interest, or a right to receive distributions (that is, a debt-type claim) will affect both tax characterisation and the availability of preferential treatment. Second, cross-border tax information exchange may trigger reporting obligations. Under Hong Kong’s CRS framework for the automatic exchange of financial account information and the CARF for crypto-asset reporting, eligible financial institutions and crypto-asset service providers may need to carry out customer due diligence and information reporting under the relevant rules. Third, cross-border withholding tax needs to be addressed proactively. When cash flows generated by Mainland entertainment or real-estate assets are remitted to a Hong Kong SPV, withholding tax can materially affect investor returns. Sponsors should therefore actively assess whether they can rely on the preferential rates available under the Arrangement between the Mainland of China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income - for example, by seeking to reduce dividend withholding tax from 10% to 5%, or royalty withholding tax to 7%. However, applying those treaty benefits requires advance planning. The Hong Kong SPV must obtain a Certificate of Resident Status (CoR) and satisfy the Mainland tax authorities’ strict substantive tests for “beneficial owner” status.

For Mainland enterprises holding high-quality underlying assets, issuing RWA products through Hong Kong opens up a new route to broader financing channels and access to global liquidity. But the real question is not whether a real-world asset can be put on-chain. It is whether a sound implementation framework can be built across law, tax, and commercial structuring. Hong Kong has already put in place the supporting infrastructure and regulatory environment. In this still-emerging RWA wave, the true winners will be those capable of navigating complex compliance challenges.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.