In October 2023, the Council of the European Union adopted Council Directive (EU) 2023/2226 (DAC8), marking the seventh amendment to Directive 2011/16/EU on administrative cooperation in the field of direct taxation, commonly referred to as the Directive on Administrative Cooperation in Direct Taxation (DAC). DAC8 formally incorporates the OECD Crypto-Asset Reporting Framework (CARF) into the EU framework for tax cooperation. In 2025, EU Member States will progressively complete the transposition of DAC8 into domestic law. As of 1 January 2026, DAC8 will take effect, initiating the first reporting year for crypto-asset tax information and moving the European crypto-asset market toward full operational implementation.

DAC8 aims to strengthen the overall legal framework for automatic exchange of information (AEOI) by bringing crypto-asset information within the scope of tax information exchange, thereby combating tax fraud, tax evasion, and tax avoidance.

CARF is an international standard for the automatic exchange of tax information developed under the OECD to govern cross-border tax reporting and disclosure relating to crypto-assets. Building on CARF, DAC8 sets out the rules and procedures for the exchange of information on crypto-asset users. Through due diligence procedures and reporting rules, it regulates service providers active in crypto-asset transactions and their users.

DAC8 establishes due diligence and reporting obligations for crypto-asset service providers. It requires EU Member States to obtain information from Reporting Crypto-Asset Service Providers (RCASPs) and to exchange such information annually with the EU Member State in which the taxpayer is resident. RCASPs must collect transaction information relating to their non-resident investors for each reporting period and submit such information, in the calendar year following the reporting period, to the tax authority of the Member State in which the RCASP is located. That tax authority must then exchange the information with the tax authorities of the EU Member State(s) where the non-resident investor is resident within nine months after the end of the reporting period. Accordingly, the exchange of information relating to the first reporting period, 2026, is to be completed by 30 September 2027.

With respect to the scope of information exchange under DAC8, the directive is based on the definition of crypto-assets under the EU Markets in Crypto-Assets Regulation (MiCA). It covers a broad range of crypto-assets and also includes e-money tokens and certain non-fungible tokens.

CARF does not have direct legal effect and must be implemented through regional or domestic legislation. The EU institutionalizes CARF through DAC8 by integrating it into the EU legal framework.

DAC8 adopts CARF’s definitions of crypto-assets, RCASPs, and reportable users, and aligns with CARF in its requirements relating to transaction categories, due diligence rules, and reportable data fields. DAC8 transforms CARF into a mandatory and enforceable EU framework for cross-border tax transparency and integrates it with MiCA and the existing DAC toolkit. It not only harmonizes tax information exchange across the EU, but also effectively brings crypto-asset reporting within the EU’s fiscal supervisory framework.

In addition, DAC8 introduces certain extensions to CARF to reflect EU-specific features. It effectively makes extraterritorial compliance a condition for access to the EU market by imposing mandatory reporting obligations on non-EU crypto-asset service providers when they provide services to EU users.

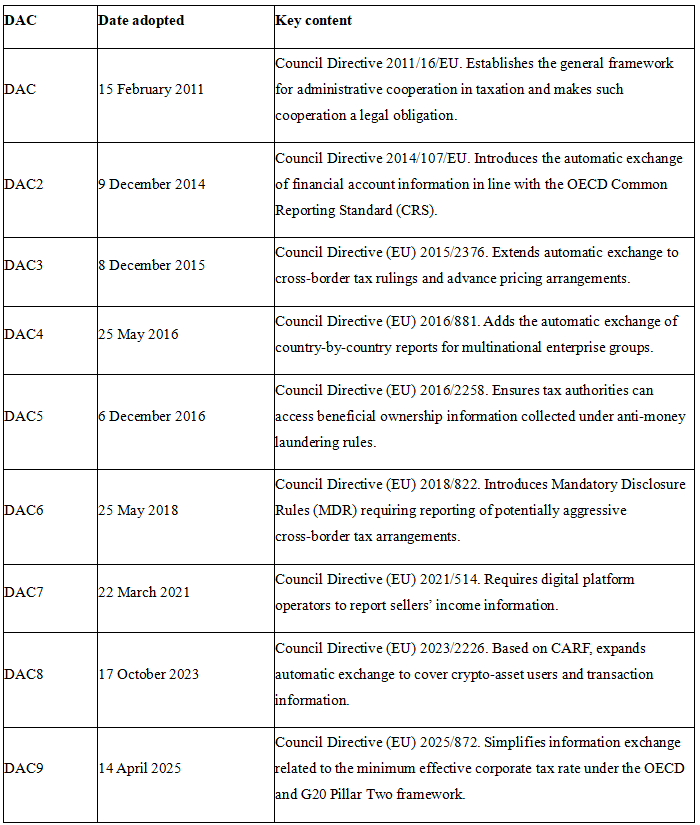

The EU began issuing the DAC series of directives in 2011. DAC does not itself govern the assessment or collection of taxes. Instead, it establishes a coordinated framework that enables EU Member States to collect and exchange tax-related information concerning individuals and legal entities. Its purpose is to support mutual assistance in tax matters and ensure administrative cooperation among national tax authorities across the EU.

To date, DAC has undergone eight subsequent amendments. These revisions have expanded the scope of covered taxpayers and increased the types of data subject to reporting. The evolution of the DAC framework, from DAC through DAC9, is summarized below.

Overall, the DAC framework reflects a shift in the EU from relatively passive information sharing toward a more proactive, systematic, and technology-enabled approach to tax transparency, expanding from traditional income to complex cross-border arrangements and, more recently, to the digital and crypto economy.

DAC8 expands the scope of information subject to automatic exchange under DAC by requiring RCASPs to report reportable transactions and transfer information involving crypto-assets and e-money. It ensures that crypto-assets follow the same information logic applied to traditional financial assets, continuing and strengthening the DAC-based exchange framework. By broadening asset-class coverage, DAC8 marks the full integration of crypto-assets into the EU’s general tax transparency and administrative cooperation regime, rather than treating them as a special or peripheral asset class.

Beyond crypto-assets, DAC8 also refines certain existing provisions of DAC. It improves the reporting and communication rules for taxpayer identification numbers (TINs) to help tax authorities identify relevant taxpayers and assess the associated tax liabilities more effectively. It also grants Member States flexibility in areas such as penalties and compliance to support effective implementation of the DAC framework.

The development and implementation of DAC8 can be viewed at two levels: the EU level and the Member State level.

At the EU level, the origins of DAC8 can be traced back to 2022. Key milestones are set out below.

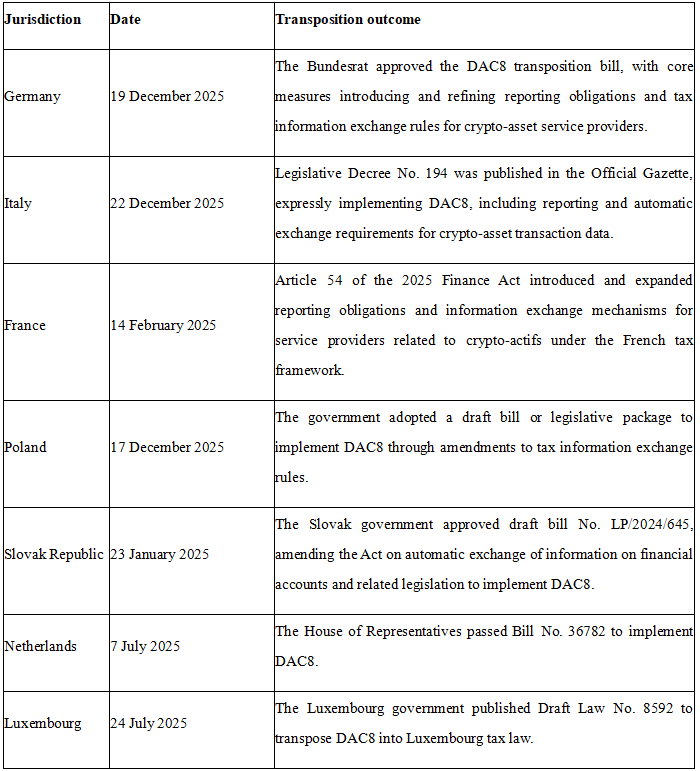

DAC8 provides for a transitional period and requires all Member States to complete transposition by 31 December 2025. Examples of national transposition developments include the following.

Overall, at the EU level, DAC8 functions as a system-building instrument that harmonizes and integrates crypto-asset reporting into the EU’s existing tax transparency framework. At the Member State level, it operates as a transposition-driven administrative regime shaped by national enforcement culture, administrative capacity, and policy priorities. The effectiveness of DAC8 will depend not only on a harmonized legal design, but also on each Member State’s ability to translate crypto-asset data into effective enforcement outcomes.

For crypto-asset service providers, RCASPs serve as the primary conduit for information transmission under DAC8. Crypto-asset service providers will, in effect, be transformed into tax-reporting intermediaries. They will be subject to mandatory obligations to determine customers’ tax residency, collect taxpayer identification numbers (TINs), and classify transactions. They must comply with due diligence requirements and submit annual reports to the competent tax authorities. In this sense, RCASPs are brought into the EU tax administration and enforcement framework.

DAC8 also requires crypto-asset service providers to have robust IT systems, legal and tax expertise, and the operational capability to report on an ongoing basis. This entails significant fixed compliance costs, raising the capital threshold for market participation. Smaller providers may face consolidation pressures or exit the market, which may accelerate market concentration and professionalization within the EU crypto-asset sector.

DAC8 applies both to crypto-asset service providers established in the EU and to non-EU providers that offer services to EU users. By linking compliance to market access, it effectively globalizes EU compliance standards for the crypto-asset industry.

The implementation of DAC8 will also have indirect effects on traditional financial institutions such as banks, by imposing higher expectations for risk management. By bringing crypto-assets within the regulated financial system, DAC8 makes crypto-asset exposure a material compliance risk factor for traditional financial institutions. This may require them to reassess crypto-related clients and strengthen due diligence, particularly for high-volume crypto-asset customers.

DAC8 reduces the structural tax opacity historically associated with crypto-assets. Information such as an individual investor’s tax residency, crypto-asset transaction volumes, and cross-border activity will be reported to tax authorities and exchanged automatically among EU Member States. This will increase compliance burdens for individual investors to some extent and may lead to more standardized and compliant trading behavior.

In addition, although DAC8 is not retroactive, the data obtained under DAC8 may trigger audits of prior years. Historical non-compliance in relation to crypto-asset transactions may therefore be reassessed and may result in penalties.

In light of the potential impacts of DAC8, market participants should strengthen compliance awareness, begin consolidating and standardizing data, and seek to convert the compliance burden arising from increased tax transparency into a competitive and governance advantage. In particular:

For crypto-asset service providers, it will be necessary to register in an EU Member State or appoint an EU reporting intermediary in order to centralize DAC8 reporting. Providers may also consider tagging transactions by asset type and transaction characteristics and embedding tax logic into product design to facilitate efficient information collection.

For traditional financial institutions, one approach is to partner with RCASPs that can support DAC8-related reporting and controls, thereby strengthening risk management for crypto-asset exposure. Leveraging the compliance advantages of existing DAC infrastructure, traditional institutions may also develop offerings such as crypto brokerage services and tokenized securities and re-enter the crypto-asset market in a more compliant manner.

For individual investors, it is important to understand DAC8 and recognize the increasing transparency of crypto-asset transactions. The appropriate posture should shift from risk avoidance to proactive compliance planning, including choosing EU-regulated RCASPs as trading platforms. For legacy non-compliance issues, investors should consider voluntary disclosure and corrective filings, and seek professional tax advice where necessary.

The growing importance of the crypto-asset market should not come at the expense of tax transparency. The implementation of CARF through DAC8 marks a milestone in European crypto-asset regulation. By incorporating crypto-asset reporting obligations into the DAC framework, the EU has transformed a non-binding international standard into a legally binding, interoperable, and enforceable transparency mechanism. DAC8 closes what has been, to date, the last major blind spot in the EU’s tax information exchange system, accelerates the normalization of crypto-assets as taxable financial instruments, and positions the EU as a global leader in crypto-asset transparency governance.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.