When it comes to cross-border payments, preserving wealth, and moving capital, the differences between various financial tools and systems become much more obvious during times of high uncertainty. Unlike traditional settlement systems that rely on centralized middlemen, on-chain assets are built for cross-border transfers and self-custody without being tied to a single institution. Because of these technical traits, they are more easily used for moving value, buffering risk, and allocating assets in situations involving sanctions, high inflation, or restricted capital flows.

Take Iran as an example: under extreme external pressure, the market exchange rate of the Iranian Rial against the US Dollar plummeted 30 times. During this intense macro shock, on-chain assets—which can be moved across borders, self-custodied, and are resistant to single-point freezes—were quickly adopted by global traders and locals as a risk buffer and a way to move capital. Research from Chainalysis shows that by 2025, Iran's crypto ecosystem reached about $7.78 billion, with on-chain activity closely following major macro events. However, this borderless flow of assets also brings significant compliance risks. While censorship resistance gives users autonomy, it can also open doors for illegal money flows. Finding the right balance between innovation and regulation is a challenge that policymakers everywhere are now facing.

The short-term "tunnel value" created by macro fluctuations cannot hide the deep value split within the crypto market. The long-term, blind expansion of token supplies stands in stark contrast to the rapid death of countless projects: Data from CoinGecko Research shows that over 13.4 million crypto projects once listed have eventually stopped trading and are considered failures. This massive "death list" is a clear sign that assets driven only by "issuance-fundraising-narrative" without a real foundation cannot sustain consensus. Eventually, market capital and liquidity will inevitably shrink down to a few assets that have sustainable value mechanisms.

Against this backdrop, this paper focuses on "value mechanisms". First, it explores which tokens have the sustainable value to survive market cycles under the test of economic policy uncertainty and global economic activity. Second, it takes a deep dive into why, as global digital finance evolves, regulatory systems must follow a path that starts with cleaning up fundraising chaos, moves to governing market infrastructure, and finally lands on detailed classifications and data-driven reporting.

In its 2025 report, the World Economic Forum (WEF) defined "Tokenization" as the process of using programmable ledgers to represent asset ownership in a transferable digital format. Unlike traditional financial systems that rely on fragmented external messaging (like the SWIFT system), tokenization theoretically creates a Shared System of Record. Combined with smart contracts, this allows for a unified recording system, flexible custody models, and on-chain governance.

The Bank for International Settlements (BIS), in its "Unified Ledger" blueprint, further points out that tokenization merges messaging, reconciliation, and settlement into a single, seamless operation. This leap in underlying architecture significantly cuts down on trust friction and compliance costs in global business. Its theoretical framework is built on three core proofs: First, Proof of Value. This means asset issuance must have a verifiable foundation—either backed by cash flows from the real economy or a broad network consensus. This ensures that on-chain assets aren't just "narrative bubbles" created out of thin air. Second, Proof of Ownership. Property rights must be clear, giving the power to dispose of the asset directly to the legal holder. By using cryptography, distributed ledgers establish exclusive rights and cut the reliance on central intermediaries, technically avoiding the "tail risk" of assets being frozen or misused by a single entity. Third, Proof of Transaction. There must be an unchangeable, verifiable history of trades along with evidence of clearing and settlement. This means every global capital flow is fully traceable, providing the data needed for compliance audits and look-through regulation.

Together, these three proofs form the logical starting point for how tokenization reshapes financial infrastructure: Proof of Value sets the foundation for issuance, Proof of Ownership changes how property rights are exercised, and Proof of Transaction rebuilds the trust mechanism for clearing and settlement.

Current tokenization models can be split into two basic categories based on how they capture value: Native Tokens and Backed Tokens. Their ability to survive macro cycles differs greatly because they are anchored to different things.

Native Tokens are assets issued directly on the blockchain, with their own built-in records for issuance, trading, and ownership. These assets (like the native assets on the Ethereum network) usually aren't pegged to external physical assets. Their main job is to act as a settlement medium within the network and serve as the "security budget" that keeps the decentralized system running. Specifically, native tokens use economic incentives (like Proof of Stake, or PoS) to get nodes to maintain network consensus. They also act as the "network fuel" (Gas Fee) when users run smart contracts or execute complex business logic. The long-term value of a native token is tied deeply to whether that blockchain network can continue to lower costs for real-world economic activities—its value comes from how thriving the ecosystem is and how often it’s actually used. Simply put, the value anchor for native tokens is network utility.

Backed Tokens are also issued and moved on-chain, but their value is strictly pegged to off-chain assets. Their main mission is to bring real yields from traditional financial markets onto the blockchain. In today's world of growing economic uncertainty, backed tokens are proving to be extremely useful. For example, tokenizing high-quality liquid assets like US Treasuries doesn't just give traditional assets 24/7, divisible global liquidity; it also gives on-chain capital a "risk-free" yield benchmark that stays away from the high volatility of the crypto market. For companies working internationally, these are great tools for managing liquidity, hedging against local currency devaluation, and lowering the costs of global business in a messy macro environment. The value anchor for backed tokens is the value of the off-chain assets.

The fundamental difference is this: Native tokens get their value from within the network, and their survival depends on whether the ecosystem keeps creating value. Backed tokens get their value from an off-chain map, and their survival depends on the credit quality and payout ability of the underlying assets.

After several "bull and bear" cycles, the crypto market is seeing a serious return to reality. Data from CoinGecko Research shows that over 13.4 million crypto projects driven only by "issuance-fundraising-narrative" eventually stopped trading and were kicked out of the market. This huge "death list" reveals a basic rule: speculative goods without underlying assets or real use cases are destined to lose market consensus when macro liquidity dries up.

From an institutional economics perspective, for a token to have sustainable value and survive macro shocks, it must substantially lower the "friction costs" of the real economy and build a solid rights structure. We can look at this sustainable value through three lenses.

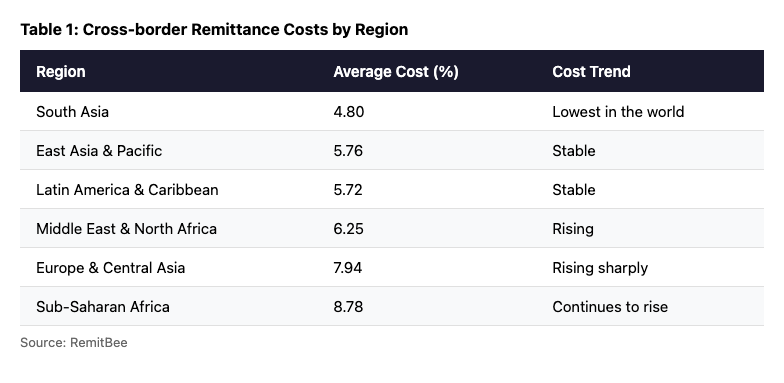

Companies going global or doing cross-border trade rely heavily on stable, low-friction payment networks. However, the traditional Correspondent Banking model creates a lot of "system friction" because the clearing chains are long and the compliance steps are complicated. As of the first quarter of 2025, World Bank data shows that the average cost of global cross-border remittances is still as high as 6.49%, with costs through traditional banks reaching 12% to 13%. You can see the costs for different regions in Table 1. Plus, due to economic instability, these costs are actually going up in some places. The BIS, in its "Project Agorá" study, also noted that the current cross-border payment system is full of challenges, whereas tokenization can merge messaging, reconciliation, and settlement into one seamless move.

Source: RemitBee

When economic policy uncertainty spikes—like during extreme capital controls or sanctions caused by geopolitical games, or when the SWIFT network is cut off during a macro crisis—traditional global capital flows don't just face high hidden and obvious costs; they face a "usability crisis" where funds could be frozen at any time. In these moments, a token's value is first seen in its "macro hedging" ability as an independent, censorship-resistant channel.

Chainalysis's global data proves this logic: in areas under extreme pressure from runaway inflation or conflict, both individuals and businesses tend to move large amounts of money into backed stablecoins like USDT or USDC to keep global supply chains running and hedge against their local currency losing value. These on-chain assets, issued on programmable ledgers, use self-custody to give control back to the user and cut the ties to any single financial middleman. For global economic players, this chain-based value network has become a capital buffer against macro policy risks.

The death of countless "shitcoins" proves that tokenomics relying purely on community hype and Ponzi-like liquidity can't last. The World Economic Forum points out that tokens with sustainable staying power must have clear "Embedded Rights"—meaning the code itself gives holders unchangeable legal economic and governance rights.

Market capital is making a major move: it’s rushing toward assets with "real yields". A WEF report shows that the total transfer volume of backed tokens like stablecoins reached $27.6 trillion in 2024, more than Visa and Mastercard combined. Stablecoin market cap has generally been on the rise since 2020 (see Figure 1). Looking at it from a macro capital efficiency view, there's a potential collateral pool of about $230 trillion worldwide, but because traditional systems are slow and physical movement is inefficient, only about $25 trillion in securities is actually used as collateral.

Tokenizing high-quality liquid assets (HQLA, like US Treasuries) doesn't just give traditional assets 24/7, infinitely divisible global movement; it brings real-economy, risk-free yields directly on-chain. This builds a valuation anchor that moves away from pure crypto speculation and connects backed tokens to classic modern finance valuation models, providing a new liquidity tool for corporate treasury management. Market performance confirms this: during times of high macro volatility, the circulation and trading of compliant stablecoins both go up significantly, showing a real demand for "verifiable value anchors". IMF research (2025) suggests that tokenizing central bank reserves is key to keeping central bank money as the core settlement tool in the digital asset world. Essentially, it’s a tech upgrade for the existing reserve system, not creating new central bank debt.

In the day-to-day life of a business and financial clearing/settlement, a sustainable token’s core value comes from how it reshapes the efficiency of contracts. In traditional capital markets, things like paying dividends, stock splits, and voting are slow and painful. Because the data isn't structured well, it’s easy to have information gaps and mistakes in reconciliation.

The "programmability" of smart contracts offers a new way out: unchangeable code prevents one side from changing the rules and rebuilds business trust through standardized operations. Business contracts like global compliance checks (KYC/AML), moving complex assets, and automating profit sharing can all be turned into self-executing code. Even better, smart contracts enable "Atomic Settlement" (Delivery versus Payment, or DvP), which basically wipes out reconciliation friction and counterparty risk in global collaboration.

This is how the sustainable value of native tokens is established: they act as the "system security budget" and "network fuel" (Gas Fee) that keeps the decentralized ledger running efficiently and safely. This logic has been proven by the market—on chains like Ethereum, network activity and native token consumption are highly correlated. As long as the underlying chain keeps lowering costs for real-world global payments, supply chain finance, and clearing/settlement, the value loop for the native token creates a self-sustaining flywheel effect.

If a token's internal value is decided by its code, then the ever-changing regulatory framework decides its boundaries and compliance costs in the modern economy. A PwC report notes that regulation is no longer a shackle; it’s actively reshaping the market so digital assets can scale responsibly. Globally, crypto regulation has followed a clear path: starting with "cleaning up fundraising chaos," moving to "market infrastructure governance," and finally reaching "detailed classification and data reporting". The main driver here is that as the crypto market grows and assets get more complex, financial risks are no longer stuck inside a little crypto bubble—they are moving into traditional global capital flows and macro financial stability.

From the view of global capital movement, the evolution of regulation is a mix of reacting to big risks and proactively stopping them. It can be split into three stages:

In the early days, the market was full of projects driven only by narratives. Since assets weren't well-defined and had no real cash flows, risks were mostly about regulatory arbitrage, illegal fundraising, and investors getting hurt. Many projects failed shortly after they started trading. Back then, regulation was all about "containment"—cutting off the path between traditional cash and these groundless tokens to stop illegal capital flight and protect the macro financial order.

As the ecosystem grew, centralized exchanges (CEXs) and custodians got huge, creating massive "concentration risk". Without regulation, these places often mixed funds and lacked internal controls. When liquidity got tight or policies became uncertain, these centralized spots were prone to "bank runs," causing a strong pro-cyclical effect. So, regulators shifted focus to building "resilient infrastructure". They started requiring "Asset Isolation" (Bankruptcy Remoteness) and independent third-party custody to make sure customer assets stayed safe if a firm went bust, cutting off the risk of a single point of failure crashing the whole system. This was the era of "institutional regulation"—bringing traditional financial safety standards into the crypto world.

Now that blockchain is being used by mainstream finance to lower trade friction, regulation is getting serious. Regulators realized a "one-size-fits-all" approach won't work for complex assets. Leading laws like the EU's MiCA and Liechtenstein's TVTG define tokens as "Containers of Rights" and regulate them strictly based on their economic traits. Meanwhile, regulatory tools are going digital and using APIs, requiring real-time, look-through monitoring of on-chain liquidity and global capital moves through unified data reporting. This is "embedded regulation"—baking compliance right into the tech.

Regulators use different rules and tools depending on what a token is anchored to.

For Native Tokens, the goal is to strengthen network resilience and stop money laundering. Non-anonymous crypto assets have a significantly higher average market cap because they are easier to regulate (Cremers et. al, 2025). Native tokens are decentralized and behave like "bearer assets," with everything happening on-chain. In a messy macro world, this anonymity gives users freedom, but it can also be used to dodge rules. Global anti-money laundering groups like the FATF now prioritize monitoring Virtual Asset Service Providers (VASPs). For native tokens, regulators rely heavily on "on-chain analytics" and the FATF "Travel Rule," which requires recording the real identities of both sides of a trade. Basically, they achieve compliance through the service providers without breaking the decentralized network.

For Backed Tokens, the goal is auditing off-chain assets and managing liquidity. The value of a backed token relies on the promise that it can be traded for the real off-chain asset. The weak spot is a potential mismatch between what’s on the chain and what’s actually in the vault. To handle macro shocks, regulators focus on stopping "De-pegging" risks. A February 2026 proposal from the US OCC requires stablecoin issuers to keep 100% high-quality liquid asset reserves, with monthly reports and yearly audits. Modern rules force issuers to use frequent, independent audits and limit risky investments to make sure they have enough liquidity to cover everything. They are using traditional auditing standards to back up on-chain value.

When dealing with fast, complex global trades, the old way of "punishing after the fact" is too slow and expensive. To balance efficiency with safety, many countries are pushing for "Compliance as Code".

By using token standards designed for compliance (like ERC-3643 or the T-REX protocol), identity checks (KYC/AML), travel rule thresholds, and capital limits are hard-coded directly into the smart contracts. This means if a global transfer doesn't meet the rules or hits a sanctions blacklist, the trade is automatically blocked by the blockchain itself. This move from "punishing later" to "embedding before" doesn't just lower costs for global business; it provides a safe infrastructure for legal capital to move even during extreme macro shocks. A DFCRC report estimates that with a clear framework, tokenized markets could create tens of billions in economic gains for Australia, but that potential depends on building this regulatory infrastructure.

Tokenization is rebuilding the foundation of global finance, while geopolitical conflicts and economic uncertainty are acting as the "stress test" for this new way of holding value. In the middle of all this volatility, the "narrative bubbles" and groundless assets are being peeled away, and money is flowing toward tokens with real value.

This research shows that sustainable tokens that can survive market cycles usually have a few things in common: they offer real yield anchors by bringing off-chain credit on-chain; they significantly lower the cost of global contracts through programmability; and they act as a security budget for decentralized networks. These aren't just speculative symbols; they are value carriers tied to real economic activity, with specific functions, yields, or rights.

Right now, global regulation has moved from just trying to block things to actively building rules into the system. Through detailed classification and "compliance as code," regulators are carefully bringing high-quality digital assets into the mainstream financial system.

Given this irreversible trend, here are some suggestions for different players:

For Businesses: Treat on-chain assets as a tool for moving capital more efficiently around the world. For global settlements, prioritize compliant stablecoins to hedge against currency swings and lower system friction. At the same time, make sure to differentiate between volatile native tokens and strictly regulated backed tokens in your cash management strategy.

For Issuers and Financial Institutions: Forget the old "issue a token just to raise money" mindset. The focus should shift entirely to "Embedding Rights"—clearly and unchangeably defining asset traits in the code. Use compliance-friendly standards like ERC-3643 and give the market transparent, real-time proof of value and reserves.

For Policymakers: Stay "tech-neutral" but push for "Compliance as Code". While holding the line against money laundering and systemic risk, guide the construction of unified ledgers based on broad consensus. Merge national credit with programmable tech to build the next generation of financial infrastructure for the digital age.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.