In recent years, the UAE has rapidly emerged as a global center for crypto assets. Within the UAE, giants of the crypto industry are making significant moves into the local market: Binance has secured full regulatory authorization, Circle has been approved as a money service provider, and Ripple has obtained a blockchain payment license in Dubai. While pushing the growth of the crypto industry, the UAE is also actively building a supporting system for crypto regulation and taxation. On October 29, 2025, the UAE issued Federal Cabinet Decision No. 134 of 2025, which explicitly brings Virtual Asset Service Providers (VASPs) into the anti-money laundering framework and sets out the "Travel Rule" for virtual assets. On February 24, 2026, Dubai's Virtual Assets Regulatory Authority (VARA) released implementation requirements for said "Travel Rule," making it mandatory to collect, verify, securely transmit, monitor, and preserve information on the originators and beneficiaries of virtual asset transfers. The UAE's crypto regulatory and tax systems are becoming increasingly mature, showing a "Federal-Emirate" dual-governance model from top-level design to practical implementation. This article intends to study the crypto regulatory system and tax overview of the UAE, analyze crypto regulatory trends, and provide compliance references for crypto market participants.

The United Arab Emirates (UAE) is a federal monarchy made up of seven emirates: Abu Dhabi, Dubai, Sharjah, Ajman, Umm Al Quwain, Ras Al Khaimah, and Fujairah. In the crypto asset field, the UAE has gradually formed a "Federal-Emirate" dual-governance model with distinct local characteristics. The Federation is mainly responsible for establishing the basic legal framework for crypto asset regulation and taxation, while each emirate builds more specific and professional regulatory details through local legislation and financial free zone regulators. This model reflects the basic logic of power distribution between the center and localities under the UAE's federal structure, providing an agile governance space for the development of the local crypto industry. To break it down:

Regarding the regulatory system, the UAE government has integrated crypto asset activities into the national financial regulatory system. The Central Bank and the anti-money laundering framework require banks and financial institutions to identify and avoid transactions with unlicensed virtual asset providers. Emirates like Abu Dhabi and Dubai have set up local regulators responsible for issuing licenses to exchanges, custodians, and brokers in designated areas. Dual regulation allows different emirates to explore more innovative regulatory models based on their own economic development strategies and financial market positioning, all within a unified federal legal framework.

Regarding the tax system, the UAE implements a unified basic tax regime. Each emirate provides relatively favorable tax treatment for eligible companies through local tax policies, thereby creating a competitive advantage in attracting crypto enterprises and capital inflows. While maintaining the overall unity of the tax system, the UAE also provides policy space for local economic development and industrial clustering.

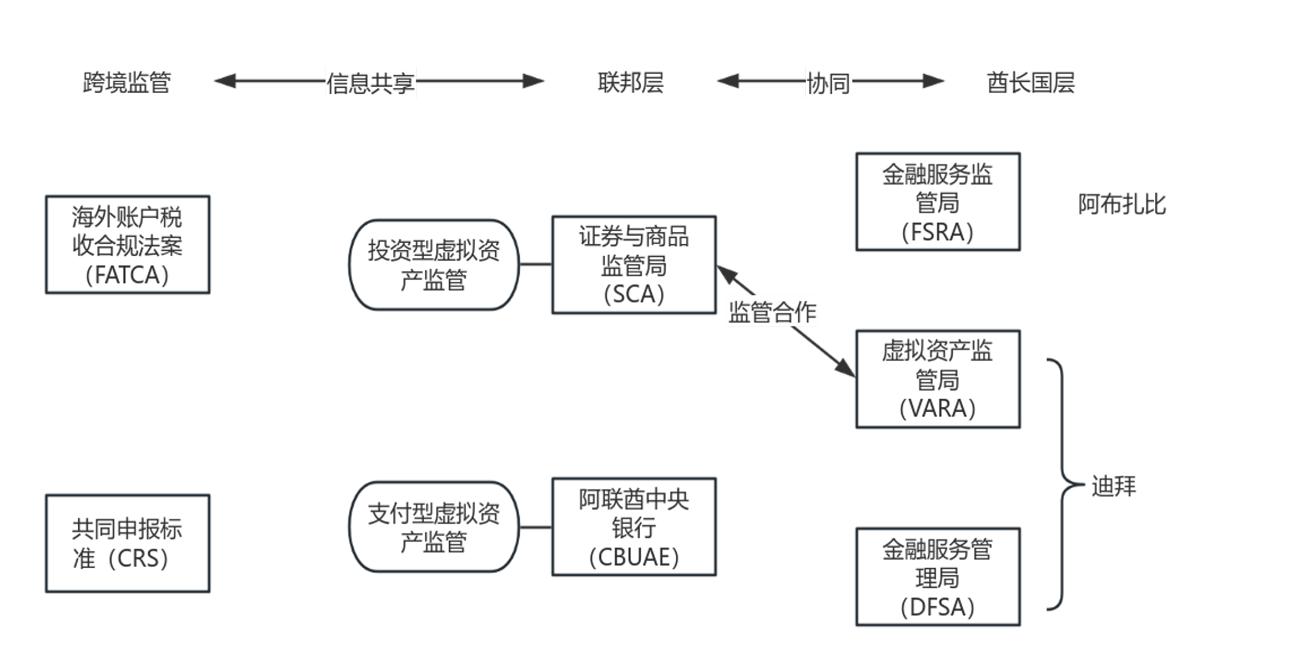

Crypto regulation in the UAE is reflected internally as the collaborative governance of federal and emirate regulatory frameworks, and externally as active participation in globally unified regulatory and information exchange frameworks.

Cabinet Decision No. 111 of 2022 authorizes the Securities and Commodities Authority (SCA) to license and supervise crypto asset activities in the UAE mainland and certain free zones. The local licensing authorities of each emirate are responsible for virtual asset regulation in their own regions. The Central Bank of the United Arab Emirates (CBUAE) is responsible for regulating virtual assets used for payment purposes and approving policies that might affect the stability of the financial and monetary system.

According to the "Regulatory Guidelines for Virtual Assets and Virtual Asset Service Providers" issued by the SCA, virtual assets are divided into two categories: Investment Virtual Assets (used for investment purposes) and Payment Virtual Assets (used for payment purposes). In terms of regulatory division of labor, Investment Virtual Assets are regulated by the SCA, while Payment Virtual Assets fall under the jurisdiction of the Central Bank. Regarding regulatory requirements, it is stipulated that virtual asset service providers must obtain a license if they operate trading platforms or provide virtual asset-related financial services such as trade matching, brokerage, custody, and investment consultancy. They must meet technical governance requirements, including establishing security control and protection mechanisms for wallets and private keys, as well as IT system testing, system change management, cybersecurity measures, and disaster recovery mechanisms for system operation management. When a blockchain undergoes a soft fork or hard fork, they must assess the impact in advance, notify customers, and ensure the consistency of customer assets. They must also fulfill anti-money laundering (AML) compliance obligations, such as conducting customer due diligence (CDD), reporting suspicious transactions, establishing risk assessment mechanisms, and screening sanctions lists. Additionally, the guidelines initially laid out the "Travel Rule."

According to the "Payment Token Services Regulation" issued by the CBUAE on June 7, 2024, engaging in the issuance, custody, transfer, and payment service business of payment tokens requires a license from the CBUAE. The regulation sets strict requirements for stablecoin issuance, including issuer reserve asset requirements, asset segregation, information disclosure, and redemption mechanisms. All payment token service providers must fulfill AML obligations such as customer due diligence, reporting suspicious transactions, and maintaining transaction records. If a payment token service provider violates the rules, it could trigger legal consequences such as fines, business restrictions, or even the revocation of licenses. In this regard, the CBUAE has the power of supervisory inspection, information requests, administrative penalties, and the suspension or revocation of licenses.

Against the backdrop of the aforementioned regulatory systems, the UAE government further issued Federal Cabinet Decision No. 134 of 2025 on October 29, 2025. This explicitly includes virtual asset service providers in the AML framework, requiring them to perform customer due diligence and transaction monitoring, and mandating the enforcement of the Financial Action Task Force (FATF) Travel Rule for crypto asset transfers. The federal crypto regulatory framework is becoming increasingly complete.

At the emirate level, the UAE has established two financial free zones: the Dubai International Financial Centre (DIFC) and the Abu Dhabi Global Market (ADGM). The regulatory bodies of these financial free zones regulate virtual assets within their respective jurisdictions. The UAE has initially established a federal-emirate cross-agency synergy mechanism based on regulatory cooperation agreements, thereby reducing regulatory conflicts between the UAE federation and local jurisdictions and promoting the unification of regulatory standards across the country.

Abu Dhabi: Abu Dhabi established the Abu Dhabi Global Market (ADGM). Its Financial Services Regulatory Authority (FSRA) is independent of the federal level and is responsible for regulating financial activities such as crypto assets within the region. On June 25, 2018, the FSRA launched a crypto asset regulatory framework aimed at addressing various risks associated with crypto asset activities, including risks in AML and financial crime, consumer protection, technical governance, custody, and exchange operations. On February 24, 2020, the FSRA updated its virtual asset regulatory framework, changing the term "Crypto Asset" to "Virtual Asset" to align with the terminology used by the FATF. It also moved applicable regulations and rules from the specific category of "Operating a Crypto Asset Business" to the corresponding underlying regulated activities, such as providing custody services, operating a multilateral trading facility, and conducting investment transactions, to better reflect the nature of the underlying activities related to virtual assets.

Dubai: Dubai has two independent crypto regulatory jurisdictions, including the Dubai International Financial Centre (DIFC) and other areas like the Dubai mainland.

The Virtual Assets Regulatory Authority (VARA) is responsible for regulating the offering, use, and exchange of virtual assets throughout Dubai outside of the DIFC:

In 2023, VARA released the Virtual Assets and Related Activities Regulations, creating a comprehensive virtual asset regulatory framework based on principles of economic sustainability and cross-border financial security. New companies applying for a VARA license go through two stages: applying for company registration approval and applying for a Virtual Asset Service Provider (VASP) license. All companies applying for a VARA license must comply with VARA's four mandatory regulations regarding company rules, compliance and risk management, technology and information, and market conduct. They must also follow the rulebooks for the virtual asset activities they are authorized to carry out, such as advisory services, broker-dealer services, custody services, and exchange services. On May 19, 2025, VARA released Rulebook 2.0, completing the first round of upgrades to the regulatory framework. This strengthened control over margin trading and token distribution services, unified compliance requirements for all licensed activities, and provided a clearer definition for escrow wallet arrangements.

On November 24, 2025, VARA aligned with federal legislative requirements and issued a circular regarding the effective date of UAE Federal Decree-Law No. 10 of 2025 on AML/CFT/CPF and mandatory compliance requirements for VASPs. It explicitly brought VASPs under the supervision of regulators for AML, Counter-Terrorism Financing (CFT), and Counter-Proliferation Financing (CPF), and introduced updated preventive measures, transparency, beneficial ownership, penalties, and related provisions. It required VASPs to complete a full compliance process from gap assessment to full remediation within approximately 4 months.

On February 24, 2026, VARA issued implementation requirements for the UAE Virtual Asset Travel Rule based on UAE Cabinet Decision No. 134 of 2025, completing the detailed rollout of the regulatory framework in the transaction and circulation link. This requirement mandates that all virtual service providers forcibly share information about both parties in a virtual asset transfer, prohibits transactions with unregulated counterparts and privacy token transactions, and implements stricter controls on unhosted wallets. This further prevents money laundering and cross-border financial risks from the transaction chain level, perfecting the full-chain regulatory system. VARA's regulation is evolving from framework-based norms to refined governance, constantly solidifying the foundation of industry regulation and guiding the industry toward healthy development under the premise of compliance.

The Dubai Financial Services Authority (DFSA) is responsible for regulating virtual asset activities in the Dubai International Financial Centre (DIFC), operating independently from the Dubai mainland and most free zones:

On November 1, 2022, the "Crypto Token Regime" issued by the DFSA came into effect, stipulating its power to set rules to regulate the recognition, issuance, and activities of crypto tokens. On December 15, 2025, the DFSA issued regulatory guidelines on the suitability assessment for applying crypto tokens in the DIFC. It required that the relative importance of various indicators should be considered during the assessment of crypto tokens, taking into account all relevant factors, including the proposed activities, customer base, and the nature, scale, and complexity of the business in the DIFC. On January 12, 2026, the DFSA began implementing the latest crypto token regulatory framework, shifting from a DFSA-led suitability assessment to a company-led assessment. This strengthened investor protection, improved behavioral and operational requirements, covered corresponding reporting obligations more in line with the current global crypto asset market conditions, and reinforced the regulatory system centered on the DFSA.

International cooperation and domestic regulation regarding crypto activities in the UAE support each other. Currently, the UAE automatically exchanges information with the US Internal Revenue Service (IRS) through the Foreign Account Tax Compliance Act (FATCA) and with authorities in other jurisdictions through the Common Reporting Standard (CRS). Specifically, FATCA and CRS require UAE Reporting Financial Institutions (RFIs) to report information on certain financial accounts maintained by reportable account holders and/or controlling persons to the UAE Ministry of Finance annually. Subsequently, the UAE Ministry of Finance exchanges data with the US IRS and relevant jurisdictions respectively. UAE RFIs must report details of reportable accounts every year before the prescribed deadline (usually June 30).

On November 8, 2025, the UAE Ministry of Finance announced the implementation of the updated CRS 2.0 starting from January 1, 2027, with the first information exchange under the new rules beginning in 2028. CRS 2.0 expands the scope of information exchange, clarifies tax information reporting obligations for various crypto asset-related activities, and puts forward additional audit and reporting requirements. Its implementation helps prevent crypto assets from becoming tools for cross-border tax evasion, solidifies the UAE's compliant image as a global crypto asset hub, and achieves broad coverage of UAE crypto tax regulation.

Furthermore, to extend global tax transparency standards to crypto activities, the OECD developed the Crypto-Asset Reporting Framework (CARF). In November 2024, the UAE committed to implementing CARF, with the first information exchange expected in 2028. As an extension and expansion of domestic regulation, the UAE actively participates in the international cooperation system for crypto regulation and information exchange to solve issues like regulatory gaps and tax evasion caused by the cross-border flow of crypto assets.

Regarding the UAE's crypto tax system, the UAE has not established a tax law specifically for crypto assets. Instead, they are usually treated according to the existing tax system based on the use of the crypto assets. The UAE's tax structure is simple, with no personal income tax and a characteristic of few tax types and low tax rates. It implements a unified federal tax system nationwide, and each emirate does not have an independent tax law system. However, the Federation has set certain tax incentives for financial free zones, and local enterprises can enjoy preferential treatment according to the law. UAE crypto taxation mainly involves two parts: Corporate Tax and Value Added Tax (VAT).

According to Federal Decree-Law No. 47 of 2022, the UAE began levying a 9% corporate tax on June 1, 2023, with the portion of annual taxable income not exceeding AED 375,000 being tax-exempt. If crypto asset transactions constitute a "Business or Business Activity," the gains should be included in the calculation of taxable income. Companies engaged in crypto asset-related activities must comply with the UAE's corporate tax system unless the entity qualifies as a Qualifying Free Zone Person (QFZP).

Qualifying Free Zone Persons can enjoy a 0% tax rate on qualifying income. On May 20, 2024, the UAE Federal Tax Authority (FTA) issued the Corporate Tax Guide for Free Zone Persons (CTGFZP1). It explicitly pointed out that crypto assets must meet the investment purpose holding period test to enjoy the 0% corporate tax rate. This requires holding the crypto assets continuously for at least 12 months. If held for less than 12 months but dividends or other gains have been received, the intent to continue holding until 12 months must be proven. The guidance stipulates that income generated from crypto asset investments, such as dividends or profit distributions held for 12 months, capital gains from sales after holding for 12 months, and bond interest income from holdings of 12 months, can be recognized as qualifying income and apply the 0% rate. In addition, if a free zone enterprise engages in crypto asset investment as a qualifying activity, it must maintain adequate "substantial business activities" within the financial free zone. This includes: core income-generating activities like investment planning must be conducted within the financial free zone; having adequate office facilities and technical systems to support crypto asset investment; being equipped with full-time qualified employees to execute investment decisions and risk management; and generating sufficient operating expenses within the financial free zone.

UAE Cabinet Decision No. 100 of 2024, the "Amendments to the Executive Regulations of the VAT Law," fundamentally changed the VAT treatment of crypto assets, making them closer to financial services like currency exchange. According to the clarification document VATP040 regarding this amendment issued by the UAE FTA, the transfer of ownership of virtual assets is exempt from VAT, and the exemption can be applied retrospectively to January 1, 2018. If virtual asset custody and management services are provided within the UAE and explicit fees, commissions, or similar charges are collected, VAT is required at the standard rate of 5%.

On April 28, 2025, the UAE FTA issued VATP039, a public clarification document on VAT for crypto asset mining. For crypto asset mining using the "Proof of Work" mechanism, it stipulated two core tax treatment rules: First, mining for one's own account is not considered a taxable supply and falls outside the scope of VAT because there is no clear recipient, the reward is uncertain, and there is a lack of a direct consideration relationship; the mining rewards received are not seen as consideration. Second, mining for others' accounts is considered a taxable service supply because there is an identifiable service recipient, the miner obtains clear mining consideration from the customer, and providing computing power is service-oriented; thus, it is subject to the standard 5% VAT. If the customer is a non-resident service recipient and meets relevant conditions, a zero rate may apply. Accordingly, input tax for mining for one's own account is not deductible, while input tax for mining for others' accounts as a service provider is deductible within the scope used to provide taxable supplies.

In addition, the document also stipulates special rules for cross-border services. UAE enterprises receiving mining services from non-resident service providers are considered to be receiving a taxable supply. If the service recipient is registered for VAT, they should use the reverse charge mechanism to account for the tax themselves. If the service recipient is a UAE resident enterprise but not registered for VAT, the non-resident service provider needs to register for VAT in the UAE and levy the tax.

The UAE has gradually formed a crypto regulatory model that features both "supporting innovation" and "prudent regulation." Looking at the overall institutional evolution, its regulatory trends mainly show the following characteristics:

In terms of regulatory goals, the UAE's crypto regulation is compliance-oriented. In the early days, the UAE used the advantages of financial free zones and a relatively relaxed institutional environment to attract global crypto institutions to settle. As the crypto market grew, the UAE gradually strengthened requirements for AML, transaction transparency, and investor protection, pushing the crypto industry to innovate and develop within a compliance framework.

In terms of regulatory structure, the UAE's crypto regulatory system operates under the "Federal-Emirate" dual structure, and the regulatory coordination between the Federation and the emirates is becoming stronger by the day.

In terms of cross-border regulation, UAE crypto regulation is gradually aligning with international standards. The UAE is strengthening transaction traceability by implementing virtual asset travel rules, promoting the alignment of domestic and global tax transparency mechanisms, and constantly reinforcing coordination with international rules.

Under the aforementioned regulatory trends, different market participants in the crypto industry can adjust their business and compliance strategies accordingly.

For Virtual Asset Service Providers (VASPs), they should further strengthen their compliance governance capabilities. Given that the compliance requirements for VASPs from the federation and emirates are constantly increasing, VASPs should pay attention to policy changes and promptly establish complete mechanisms for customer identification, transaction monitoring, and information reporting. They should also use technical means to collect and store transaction data to meet compliance requirements. Meanwhile, companies should also pay attention to the differences in regulatory rules between different emirates, reasonably choose where to land their business, and establish a unified cross-regional compliance management system to reduce institutional risks brought by regulatory uncertainty.

For Institutional Investors, they should strengthen risk management during the investment and business expansion process. As the UAE gradually strengthens market regulation and tax systems, institutional investors should pay more attention to asset compliance, information disclosure, and tax arrangements when participating in crypto asset investment, custody, or trading platform cooperation to ensure that investment activities meet local regulatory requirements.

For Individual Investors, they should increase their awareness of changes in the crypto asset regulatory environment. Currently, the UAE still maintains a personal investor-friendly institutional environment in terms of taxation. However, with the strengthening of AML regulation and tax transparency mechanisms, individual investors still need to focus on transaction record preservation, the legality of fund sources, and potential cross-border tax information disclosure risks when participating in cross-border transactions and digital asset investment.

The UAE crypto regulatory and tax system is moving towards a more mature and institutionalized direction. While maintaining industrial attractiveness, by strengthening regulatory coordination and docking with international rules, the UAE is expected to further consolidate its position as a global crypto asset center. For market participants, actively adapting to regulatory trends and establishing a robust compliance and risk management system will become key conditions for long-term development in the UAE crypto market.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.