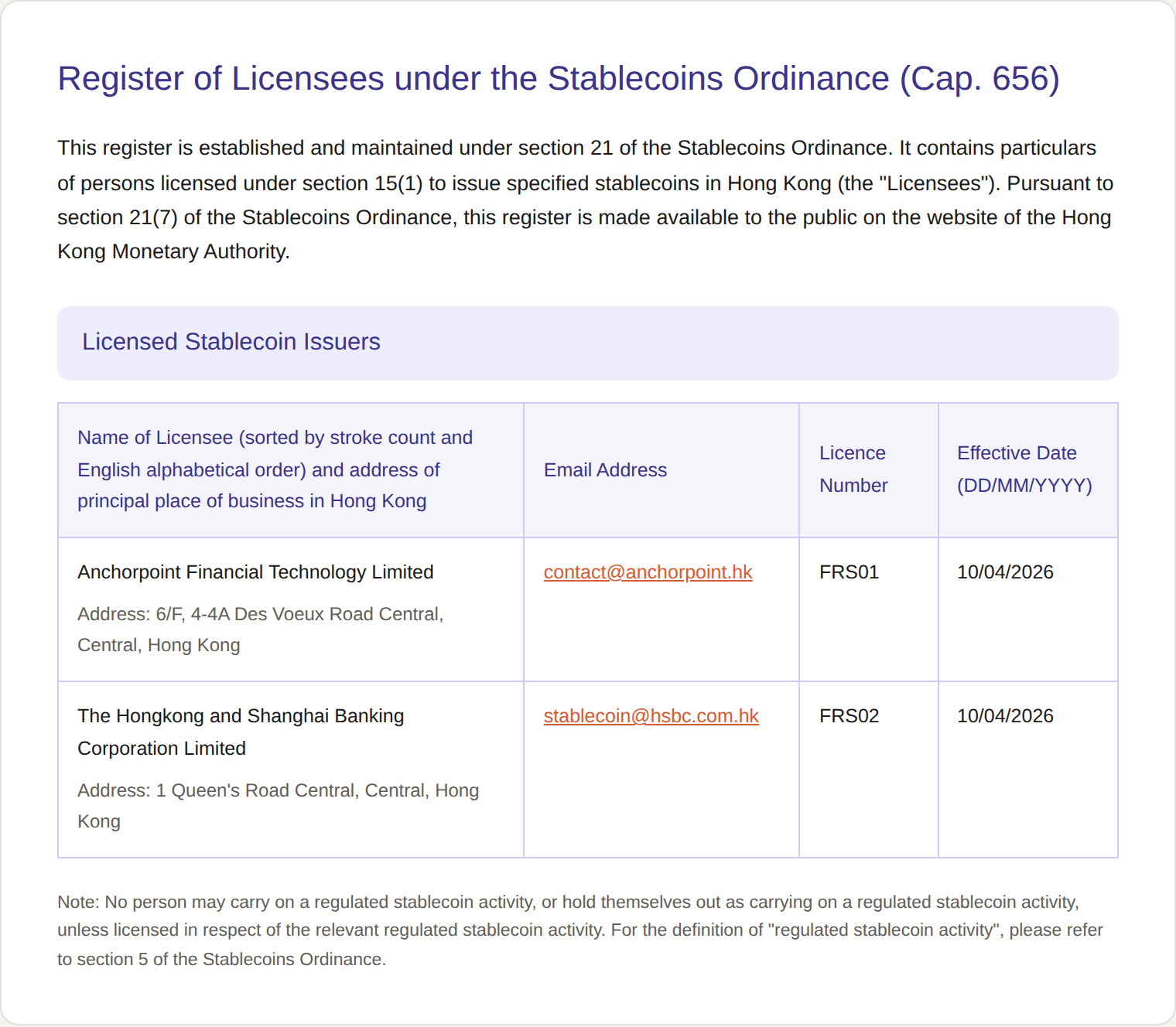

On April 10, 2026, the Hong Kong Monetary Authority (hereinafter referred to as the "HKMA") issued the first batch of stablecoin issuer licenses in accordance with the Stablecoin Ordinance. The licensed institutions are The Hongkong and Shanghai Banking Corporation Limited (hereinafter referred to as "HSBC") and Anchorpoint Financial Limited (hereinafter referred to as "Anchorpoint"), with the licenses taking effect immediately. As of the deadline for the first phase of applications, the HKMA had received a total of 36 license applications from various institutions and approved 2, resulting in an approval rate of approximately 5.6%. The two licensees are expected to successively launch stablecoins pegged to the Hong Kong dollar (HKD) starting in the second half of 2026.

Figure 1: Register of Stablecoin Licensees on the HKMA Official Website

From the enactment of the Stablecoin Ordinance on August 1, 2025, to the HKMA's commencement of license application processing on September 30, 2025, the expiration of the transitional period on January 31, 2026, and culminating in this first batch of license issuances, the legislative and enforcement loops of Hong Kong's stablecoin regulatory framework have now been fully closed. The content established by the Ordinance, including the definition of fiat-referenced stablecoins, the scope of cross-border regulation, reserve assets, redemption mechanisms, risk management, and licensing thresholds, has been specifically analyzed in previous FinTax articles and will not be repeated here. Instead, based on the results of this initial licensing, this article will analyze the actual approval requirements imposed by the HKMA beyond the statutory thresholds, as well as the regulatory trajectory for the next phase following the implementation of the licensing regime.

The initial phase approval rate of approximately 5.6% intrinsically demonstrates a significant disparity between the minimum statutory thresholds stipulated in the Stablecoin Ordinance and the actual thresholds applied by the HKMA during the approval process. The two licensees—one local note-issuing bank and one joint-venture technology company led by a licensed bank—possess the following characteristics:

HSBC is one of the three note-issuing banks in Hong Kong, ranking first in the market in terms of local retail deposits. Its stablecoin business leverages HSBC's proprietary digital channels, namely the retail e-wallet PayMe, which boasts a user base of over 3 million in Hong Kong, and the HSBC HK App. The disclosed initial application scenarios encompass three categories: peer-to-peer (P2P) instant transfers based on PayMe and the HSBC HK App; person-to-merchant (P2M) payments based on PayMe; and the subscription of tokenized investment products using stablecoins via the HSBC HK App.

Since 2022, HSBC has consistently participated in digital asset pilot projects led by the HKMA, including e-HKD+ and the Ensemble tokenization settlement platform. This participation experience ensures that its accumulated practical capabilities in specific operations, such as system integration, Know Your Customer (KYC) procedures, and reserve asset custody, demonstrate a proven alignment with the HKMA's regulatory expectations.

Anchorpoint is a Hong Kong financial technology joint venture newly established in 2026. Its shareholders comprise Standard Chartered Bank (Hong Kong), HKT, and Animoca Brands. The three parties assume differentiated functions within the joint venture structure: Standard Chartered provides a bank-grade compliance framework, a risk management system, and a global clearing network; HKT provides local payment and telecommunications infrastructure, along with retail touchpoints; and Animoca Brands provides blockchain technological capabilities and digital asset ecosystem resources. Anchorpoint plans to issue the HKD stablecoin HKDAP in phases starting from the second quarter of 2026, adopting a Business-to-Business-to-Consumer (B2B2C) business model to reach end-users through authorized distributors. Its initial application scenarios focus on the on-chain settlement of Real World Assets (RWA) as well as cross-border capital and payment flows.

Anchorpoint itself is an entity newly established specifically to apply for the stablecoin license, possessing no existing business to extend from. Its approval signifies that the HKMA recognizes a composite structure—where a licensed bank acts as the controlling shareholder and technology and scenario providers act as joint venture partners—as a valid organizational form for license applications.

The two licensees exhibit complementary characteristics in their business positioning. HSBC focuses on local retail payments and the subscription of tokenized assets, serving as a digital migration of its existing customer base and product lines. Conversely, Anchorpoint focuses on cross-border capital flows and the on-chain settlement of RWAs, constructing incremental scenarios for new financial infrastructure. These two pathways do not overlap in terms of customer structure, application scenarios, or capital flows, thereby forming a relatively comprehensive application coverage. This arrangement allows the HKMA to simultaneously observe the actual conditions of two distinctly different business models—regarding ongoing regulatory costs, compliance execution difficulties, and systemic risk characteristics—within the same regulatory cycle.

According to the press release regarding the license issuance, the HKMA explicitly outlined two approval considerations: First, whether the applicant possesses sufficient risk management capabilities and compliance experience, and adheres to relevant regulations in Hong Kong and other regions; second, whether the applicant can propose specific application scenarios and viable business plans. Based on the approval results of the first batch of licenses, we can provide a deeper interpretation of these two criteria.

Compliance obligations under the Stablecoin Ordinance cover multiple dimensions, including the segregation of reserve assets, redemption guarantees, AML/CFT, suspicious transaction monitoring, customer due diligence, and regular independent audits. The construction of a compliance system for these obligations constitutes a substantial obstacle—in terms of both time and organizational costs—for market entities that are not subject to the prudential regulation of the banking or securities industries.

HSBC itself is a licensed bank operating mature AML/CFT and risk control systems. Although Anchorpoint is a new entity, Standard Chartered Bank (Hong Kong), as the controlling shareholder, provides substantial support for compliance and risk control in accordance with the joint venture agreement. The common structure in both cases is that the issuers' risk management capabilities are rooted in the compliance infrastructure of a licensed bank, rather than being built independently by the issuers themselves. While the text of the Ordinance does not list a banking license as a prerequisite for licensing, the results of the first batch of licenses indicate that the status of a financial institution subject to prudential regulation, such as in the banking or securities sector, has effectively become a de facto threshold in the approval process. This deduction establishes a clear barrier to entry for Web3 startups and pure technology companies not subject to prudential regulation; even if they meet all the explicit requirements of the Ordinance, it will be difficult for them to obtain a license independently under the current approval stance.

The initial application scenarios disclosed by the two licensees are concentrated in four categories: cross-border payments relying on the issuer's existing international network; local payments relying on an existing retail customer base; on-chain settlement of tokenized financial products; and programmable payment and conditional settlement scenarios, such as supply chain financing. Their common structure lies in the fact that each type of scenario corresponds to an existing and identifiable financial or commercial demand. Furthermore, these scenarios can be observed, audited, and evaluated for their compliance execution effectiveness under the current regulatory framework, and they maintain a direct connection with the issuer's own customer base or business network.

This preference stands in stark contrast to application proposals that merely rely on token economic models or market share expectations. The HKMA's emphasis on the practical viability of application scenarios conveys a relatively clear policy positioning: the objective of issuing licenses is not merely to expand the roster of stablecoin issuers, but rather to ensure that compliant stablecoins assume substantial financial functions in specific scenarios such as payments, investments, RWAs, and cross-border circulation. Under this policy positioning, application proposals that fail to present specific, evaluable application scenarios are unlikely to pass the approval process, regardless of their technological or conceptual advancement.

The issuance of the first batch of licenses marks the beginning of the licensing regime rather than the end of the regulatory relationship. Before officially issuing stablecoins, the two licensees must still complete preparatory work, including technical platform and system testing, deployment of reserve and redemption arrangements, implementation of risk management measures, and staffing of key positions. The HKMA has indicated that following official issuance, it will implement ongoing supervision based on the individual business nature and risk characteristics of the licensees. This will be conducted through on-site inspections, off-site reviews, independent assessments, and regular meetings with licensee management, while evaluating implementation effectiveness against the business plans submitted during the application phase.

The actual effectiveness of ongoing supervision in the next phase can be measured by observational indicators across three dimensions. At the reserve asset level, the focus lies on the actual composition of the asset portfolio, custody arrangements, the granularity of monthly disclosures, and the substantive strength of independent audit opinions. At the redemption mechanism level, the focus is on redemption response times, fee structures, and handling arrangements in the event of a sudden bank run scenario. Finally, at the AML/CFT level, the focus centers on the actual penetration depth of customer due diligence within cross-border distribution scenarios, particularly regarding the division of KYC responsibilities between distributors and end-users in Anchorpoint's B2B2C model.

The HKMA has already demonstrated a prudent stance regarding the subsequent issuance of additional licenses, indicating that thresholds will remain at the current level and the overall number of licenses will be kept at a limited scale. The launch pace for subsequent batches is directly correlated with the business implementation effectiveness of the existing licensees. For institutions with the intention to issue but that have not yet been licensed, merely submitting an application does not constitute a valid starting point. A more feasible preparatory pathway involves establishing a risk management system equivalent to that of the initial licensees prior to application, and building a compliance endorsement through partnerships with prudentially regulated institutions.

The distinction between issuance and distribution under the Ordinance is also a key focal point worth observing. Issuance requires a license, whereas distribution requires the status of an authorized provider. Entities eligible to act as authorized providers include: (1) licensed issuers; (2) licensed corporations providing virtual asset services (VATPs); (3) entities licensed under Section 8F of the Payment Systems and Stored Value Facilities Ordinance; and corporations holding a license to carry on Type 1 regulated activities under the Securities and Futures Ordinance; and (4) banks. This institutional arrangement opens a relatively broad entry point for regulated financial institutions to participate; most financial institutions that fail to obtain an issuance license can still find room to participate in the distribution phase.

There are two key compliance points for participating in sales or distribution: First, confirming that the entity itself belongs to one of the aforementioned authorized provider categories. Second, completing reciprocal due diligence with the issuer, covering dimensions such as scale, capabilities, professional expertise, track record, reputation, as well as governance, conduct, risk management, and internal controls.

The first batch of licensing raises three taxation and compliance architecture issues that require continuous tracking.

First, the accounting and tax treatment on the issuer's side. The Ordinance prohibits licensed issuers from paying interest on the stablecoins they issue. Consequently, licensed stablecoins are presented on the issuer's liability side as non-interest-bearing redemption obligations measured at face value, which presents a structural difference in accounting and tax treatment compared to traditional interest-bearing deposit liabilities. The attribution arrangements for returns on reserve assets, the consolidated reporting and tax treatment under strict segregation conditions between reserve assets and the issuer's own assets, and the handling of foreign exchange gains and losses under cross-currency reserves (such as the permitted scenario of backing HKD stablecoins with USD assets) all remain to be gradually clarified once the licensees commence formal operations.

Second, the compliance boundaries of the distribution chain. Under the B2B2C model, the division of responsibilities between authorized distributors and issuers—particularly identifying the ultimate bearer of KYC obligations and the attribution of responsibility for suspicious transaction monitoring—directly dictates the design of the compliance architecture. The practical implementation of such multi-tiered compliance obligations in cross-border distribution scenarios will serve as a crucial entry point for observing the maturity of Hong Kong's stablecoin industry ecosystem.

Third, the structural differences compared to USD stablecoins under the U.S. GENIUS Act. The GENIUS Act's restriction on the scope of reserve assets (limited strictly to USD cash and U.S. Treasury bonds) is narrower than that of the Stablecoin Ordinance, and its regulatory hierarchy adopts a dual-tier structure at both the federal and state levels. The compliance alignment, tax characterization, and compliance costs of these two types of compliant stablecoins during cross-border circulation may yield substantial differences. Institutions currently operating or planning to operate in both jurisdictions must proactively assess the differential treatment of these two sets of rules during the architecture structuring phase.

The issuance of Hong Kong's first batch of stablecoin issuer licenses signifies that the digital asset regulatory regime has transitioned from the legislative phase into the enforcement phase. The shared characteristics in the endowments of the two licensees—namely, the status of financial institutions subject to banking prudential regulation, coupled with practical and evaluable application scenarios—form a direct correspondence with the two approval standards disclosed by the HKMA. Under the premise of a limited number of licenses, the regulatory focus has shifted from market entry review to ongoing supervision. The composition of reserve assets, the operation of redemption mechanisms, and the penetration depth of AML/CFT in cross-border scenarios will become core metrics for long-term observation.

For institutions intending to participate in the Hong Kong stablecoin market, the high threshold for issuance licenses implies that the viable entry point for the majority of entities lies in the sales and distribution phases rather than the issuance phase. A two-tier structure—centered around the licensing regime and supplemented by the authorized provider system—will constitute the fundamental institutional paradigm of the Hong Kong stablecoin market in the coming years.

[1] Hong Kong Monetary Authority: Press Release on "Monetary Authority Grants Stablecoin Issuer Licenses under the Stablecoin Ordinance", April 10, 2026.

[2] FinTax: "A Comprehensive Guide to the Commonalities and Characteristics of Stablecoin Bills in Hong Kong and the United States", July 2025.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.